The RRSP vs. TFSA vs. Non-Registered Guide for Canadians Earning $80,000

In my previous articles, The RRSP vs. TFSA Guide for Canadians Earning Under $60,000 and The RRSP Trap: Why Middle-Class Canadians Should Be Careful , I argued that for many, the TFSA is the clear winner. But as your income climbs, the math changes. At $80,000, you are sitting in a higher tax bracket where the RRSP’s immediate tax relief starts to look very tempting. In this guide, I’ll evaluate whether the RRSP finally overtakes the TFSA at this income level, or if a strategic combination of RRSP, TFSA, and non-registered accounts is the secret to maximizing your net worth.

1. Retirement Savings Options for a $80,000 Annual Income

John and Bob are Ontario residents who finished their studies at age 24 and started their careers in entry-level roles. For the next six years, they focused on paying off their student loans, which meant they didn’t contribute to any registered savings plans like an RRSP, TFSA, or FHSA.

By age 30, in January 2026, both landed jobs with salaries of $80,000 per year. To keep things simple and focused, we make a few assumptions:

- Their salaries and tax rates stay constant in real (inflation-adjusted) terms throughout their working lives.

- They don’t have a defined benefit pension plan, which is increasingly uncommon today.

- Their employers don’t offer RRSP matching contributions.

- TFSA contribution limits are indexed to inflation, but for this analysis, we assume a constant real limit of $7,000 per year.

- They work for 35 years and retire at 65.

- They remain in good health and live to age 90. Between ages 66 and 90, they rely on personal savings and government benefits, with any remaining funds passed on to their children or other beneficiaries.

With these assumptions in place, we can see how John and Bob might grow their retirement savings using three common Canadian investment options: the Registered Retirement Savings Plan (RRSP), the Tax-Free Savings Account (TFSA), and a non-registered account.

Both RRSPs and TFSAs offer strong tax advantages, but they work very differently. An RRSP gives you an upfront tax deduction, but withdrawals are fully taxable in retirement. A TFSA, on the other hand, doesn’t provide a deduction when you contribute, but your investments grow and can be withdrawn completely tax-free.

A non-registered account falls somewhere in between. Contributions are made with after-tax dollars, and there’s no upfront deduction. Withdrawals aren’t completely tax-free, but they can be tax-efficient since only part of the investment income is taxed.

To focus on the impact of these differences, this comparison assumes that John and Bob allocate the same amount of gross (pre-tax) income toward their savings goals each year. This ensures that their current lifestyles are identical, even though the specific amounts landing in their accounts differ due to the RRSP’s upfront tax refund.

2. John — the RRSP Saver

John decides to save for retirement using an RRSP. Since he hasn’t contributed during his 20s, he has significant carry-forward room. For this analysis, he contributes $14,400 annually, which represents 18% of his current $80,000 salary.

The table below summarizes CPP, EI, and income taxes payable for an Ontario resident in 2026, with and without an RRSP contribution. The calculations are based on the Personal Tax Calculator by CoPilotTax.

The first row shows John’s after-tax income without any RRSP contribution. The second row reflects the impact of making a full RRSP contribution of $14,400. As shown, the RRSP contribution reduces John’s income tax from $14,128 to $9,708 — a tax savings of $4,420. After accounting for CPP, EI, income taxes, and the RRSP contribution, John’s net take-home income is $50,323.

John invests $1,200 per month, or $14,400 per year, into his RRSP. Assuming a 6% annual real (inflation-adjusted) return, we can estimate the long-term value of his savings. Using the Ontario Securities Commission’s Compound Interest Calculator, John’s RRSP balance grows to approximately $1,648,325 by the time he retires at age 65.

Because the assumed rate of return is already adjusted for inflation, this $1,648,325 balance is expressed in today’s dollars.

Next, let’s examine how the same savings strategy unfolds when contributions are made to a TFSA instead.

3. Bob — the TFSA Saver

Next, let’s consider Bob, who prefers to prioritize a TFSA and, if necessary, a non-registered account over an RRSP. Since contributions to these accounts are made with after-tax dollars, Bob must first pay income tax on his entire $80,000 salary. Based on the 2026 tax rates for Ontario, Bob’s tax summary is as follows:

After accounting for income tax and CPP/EI premiums, Bob’s net income is $60,303. By investing $9,980 into his TFSA and non-registered accounts, his remaining take-home pay becomes $50,323 — matching exactly what John has left after his $14,400 RRSP contribution.

The TFSA Strategy

Bob intends to invest $9,980 annually. While the 2025 TFSA limit is $7,000, Bob has accumulated $76,500 in “carry-forward” room since turning 18 in 2013. By amortizing this room over the next 35 years, he adds an extra $2,185 to his TFSA contribution room. This allows Bob to comfortably contribute $9,185 per year ($7,000 base + $2,185 carry-forward) without hitting his ceiling.

Assuming Bob contributes $765 per month ($9,180 per year) to his TFSA for 35 years at a 6% annual real (inflation-adjusted) return, his balance would grow to approximately $1,050,807 by age 65. (Source: Ontario Securities Commission’s Compound Interest Calculator.) Because we used an inflation-adjusted rate, this value is expressed in today’s purchasing power.

The Non-Registered Account and “Tax Drag”

After maximizing his planned TFSA contributions, Bob has a remaining $800 to invest, which he places in a non-registered account. While this account also targets a 6% gross return (2% dividends and 4% capital gains), it is subject to “tax drag.” Since dividends are taxable in the year they are received, the effective rate of return is reduced to approximately 5.5% at Bob’s current income level. It is important to note that tax drag increases alongside income; at a salary of $130,000, for example, the drag could rise to 0.6%–0.7%, further suppressing the effective growth rate to 5.3%–5.4%.

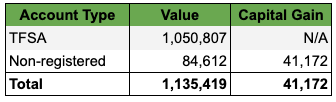

Without diving into the complex arithmetic — which lies beyond the scope of this article — Bob’s non-registered account is projected to reach $84,612 by age 65, including an unrealized taxable capital gain of $41,172.

The Comparison at Age 65

By age 65, Bob’s TFSA and non-registered accounts are expected to have the following balances:

In contrast, John’s RRSP has grown to $1,648,325. At first glance, Bob appears to be at a significant disadvantage, trailing John by $512,906. However, this comparison is incomplete without considering the tax implications of retirement.

During their working years, both men maintained the same net lifestyle of $50,323 per year. To find the true winner, we must now examine their respective tax burdens when they begin withdrawing $48,000 per year (in today’s dollars) between the ages of 66 and 90.

4. Bob’s Retirement Journey

At age 65, Bob becomes eligible for Old Age Security (OAS) and Canada Pension Plan (CPP) benefits. Having resided in Canada for over 40 years since the age of 18, Bob qualifies for the maximum OAS payment. As of January 2026, this is projected to be $742.31 per month, or $8,908 per year.

Note: While OAS payments increase by 10% once a senior reaches age 75, bringing Bob’s annual benefit to $9,798, we have omitted this increase for the sake of simplicity in this analysis.

As for the Canada Pension Plan, the maximum retirement benefit as of January 2026 is $1,433 per month for new beneficiaries at age 65. However, CPP benefits are calculated based on contribution years and earnings relative to the Year’s Maximum Pensionable Earnings (YMPE), which is set at $74,600 for 2026. Since Bob’s career income consistently exceeded this limit and he benefits from the ongoing CPP enhancement, his projected benefit is approximately $1,700 per month, or $20,400 per year.

Retirement Income Breakdown

Bob’s goal is to maintain an annual retirement spend of $48,000. This requirement will be met through his government benefits and supplementary withdrawals from his TFSA and non-registered accounts.

Bob’s Guaranteed Government Income:

- OAS: $8,908

- CPP: $20,400

- Total government benefits: $29,308

To bridge the gap and reach his $48,000 target, Bob must withdraw the remaining $18,692 (plus any applicable income tax) from his private investments. As a reminder, his available portfolios at the start of retirement are:

Maximizing the Non-Registered Account

Since the non-registered account has a relatively small balance, Bob decides to draw from it first. We assume this account continues to grow at a gross annual rate of 6% (comprising 2% dividends and 4% capital gains). To fund his lifestyle, Bob withdraws the entire 6% growth plus additional principal and capital gains.

After three years of these structured withdrawals and the associated tax payments, the non-registered account is reduced to approximately $16,300. This remaining balance represents Bob’s original, after-tax contributions; as a result, he can now withdraw the remainder entirely tax-free.

The Growth of the TFSA

While Bob spent down his non-registered assets, his TFSA remained untouched. During those initial three years, the account continued to compound tax-free at 6%. By the start of his fourth year of retirement, the TFSA balance has surged to $1,251,528.

Year 4: The Transition Point

In his fourth year of retirement, Bob’s only taxable income consists of his OAS ($8,908) and CPP ($20,400) payments. On this combined $29,308, his total tax liability is just $1,128.

To maintain his $48,000 after-tax spending goal, Bob executes the following:

At the end of year 4, Bob’s TFSA account is expected to have an account balance of $1,322,888, as he withdrew on $3,520 while it grew by 6%.

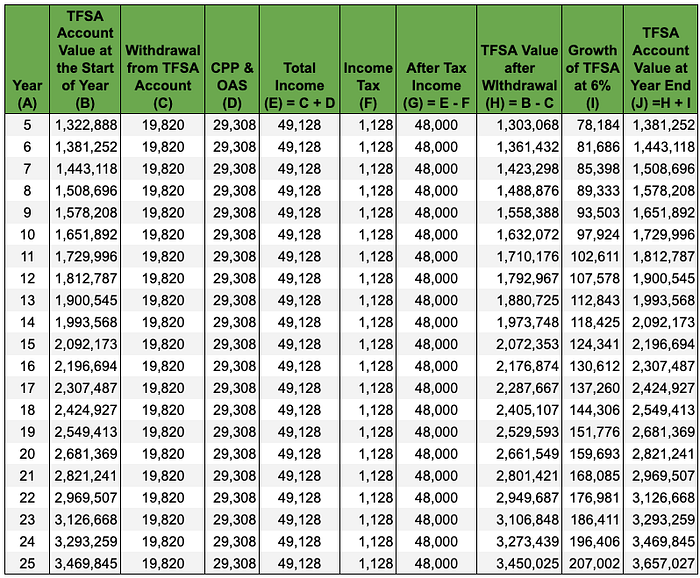

Long-Term Projections (Year 5 and Beyond)

From Year 5 onward, Bob’s strategy becomes remarkably simple. He continues to receive his $29,308 in government benefits and withdraws the remaining $19,820 (which covers his lifestyle and the small tax on his pension) from his TFSA.

Because the TFSA continues to grow at a 6% inflation-adjusted rate, its value actually outpaces his withdrawals. As shown in the table below, by the end of his 25th year in retirement (age 90), Bob’s TFSA balance has grown to a staggering $3,657,027!

The most significant advantage of this strategy is that the entire remaining balance in Bob’s TFSA is completely tax-free. Unlike an RRSP, which is often subject to a massive ‘tax hit’ upon the owner’s death, Bob’s TFSA allows him to pass his wealth on undiluted. If Bob were to pass away after age 90, his estate or named beneficiaries would receive the full $3,657,027 — with no income tax payable on the balance whatsoever.

5. John’s Retirement Journey

Like Bob, John retires at age 65, but he does so with a substantial $1,648,325 in his RRSP. His government benefits are identical to Bob’s, providing a total of $29,308 annually from OAS and CPP.

However, John faces a different set of rules when it comes to funding his lifestyle. To maintain an after-tax income of $48,000, he must supplement his government pensions with withdrawals from his RRSP. Unlike TFSA withdrawals — which do not count as income — every dollar John takes from his RRSP is fully taxable. This means John must withdraw a significantly larger “gross” amount just to cover the resulting tax bill.

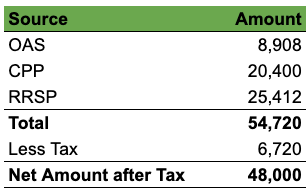

The table below summarizes John’s retirement income, taxes, and resulting after-tax income.

As shown above, John pays $6,720 in income tax, nearly six times more than Bob. This disparity exists because Bob’s TFSA withdrawals are invisible to the Canada Revenue Agency (CRA), while John’s RRSP withdrawals are added to his pensions, pushing him into a higher effective tax bracket.

John continues this pattern of withdrawing $25,412 annually for the next six years. However, a major shift occurs when he turns 71: he is legally required to convert his RRSP into a Registered Retirement Income Fund (RRIF), which introduces mandatory minimum withdrawal rates that may far exceed his actual spending needs.

The RRIF Conversion

Before we look at the mandatory withdrawals starting at age 72, let’s examine the state of John’s portfolio. By continuing to grow at a 6% annual real (inflation-adjusted) rate, John’s RRSP balance is projected to reach a massive $2,150,288 by the time he turns 71. (Source: Dinkytown’s Savings Distribution Calculator.)

At this milestone, federal law requires John to convert his RRSP into a Registered Retirement Income Fund (RRIF).

Withdrawals from RRIF

The defining characteristic of a RRIF is the mandatory minimum withdrawal. Unlike an RRSP, where you choose when to take money out, a RRIF requires you to withdraw a specific percentage of the account’s total value every year. These minimums are not based on what John needs to live, but on a government-mandated percentage of his account balance as of January 1st each year. (For details, see Section 4 of The RRSP Trap: The Withdrawal Phase & The $1M Reality Check (Part 2))

The $113,000 “Tax Problem”

At the end of his 6th year of retirement (age 71), John’s RRIF has grown to $2,150,288. Under the RRIF minimum withdrawal rules, he must withdraw 5.28% of this balance, equal to $113,535.

Whether John actually needs this amount to cover his expenses is irrelevant to the Canada Revenue Agency (CRA); he must withdraw the minimum and report it as taxable income. This forced withdrawal creates a “snowball effect” of negative tax consequences, the most punitive of which is the OAS Clawback.

OAS Clawback (Recovery Tax)

As defined by the Government of Canada, if your net world income exceeds a specific annual threshold, you must repay part or all of your Old Age Security pension. This is officially known as a “recovery tax.”

For 2026, the OAS clawback threshold is projected to be $95,323. For every dollar John earns above this limit, the government “claws back” 15 cents of his OAS.

Clawback Calculation Example: If a senior’s net income is $100,000, they exceed the threshold by $4,677. The recovery tax would be: $4,677 x 15% = $701.55.

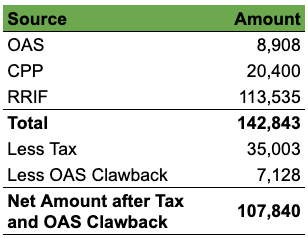

John’s Tax Summary in the 7th Year of Retirement

In this milestone year, John’s total taxable income — comprising his mandatory RRIF withdrawal, CPP, and OAS — reaches approximately $142,843. This elevated income triggers a cascade of taxes and benefit clawbacks that significantly reduce his actual “spendable” cash.

The tax summary for this income is shown below:

Analysis of the Summary

As the data illustrates, John is now paying a staggering $42,131 in combined taxes and clawbacks. While his net income of $107,840 is well above his $48,000 spending goal, he is essentially being forced to “burn” over $42,000 of his savings just to satisfy the CRA.

Furthermore, because his income is so high, John loses the Age Amount tax credit entirely, and his OAS is reduced by nearly 80%. In contrast, Bob continues to receive his full OAS and pays almost zero tax, allowing his capital to remain invested and growing.

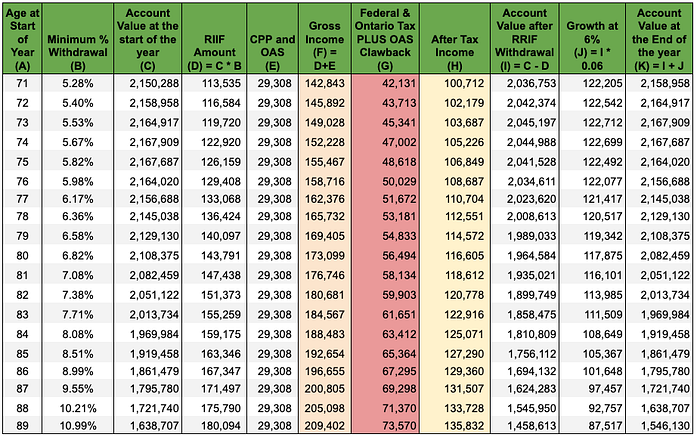

The table below provides a year-by-year breakdown of the RRIF account value at the start of each year, the required minimum withdrawals, gross income (including CPP/OAS), income taxes, OAS clawbacks, and net after-tax income. It also shows the RRIF’s continued growth at a 6% annual real (inflation-adjusted) rate and the resulting year-end balance from age 72 to age 90.

- Column B shows the minimum RRIF withdrawal percentage for each age (for example, 5.28% at age 71). Note that this percentage increases as John gets older.

- Column C shows the RRIF value at the start of the year.

- Column D shows the required RRIF withdrawal. For the first year, this is $2,150,288 × 5.28% = $113,535.

- Column E shows combined OAS and CPP income during retirement. Since both benefits are inflation-adjusted, this amount remains constant at $29,308 in real terms.

- Column F shows total gross income, calculated as the RRIF withdrawal (Column D) plus OAS and CPP income (Column E).

- Column G shows total income tax payable, including the OAS clawback, calculated using the 2026 Ontario tax rules from the TaxTips income tax calculator.

- Column H shows the after-tax income.

- Column I shows the RRIF balance after withdrawals (Column C − Column D).

- Column J shows the annual growth on the remaining RRIF balance at a 6% real rate of return.

- Column K shows the RRIF balance at the end of the year (Column I + Column J), which becomes the starting balance for the following year.

Analysis of the 18-Year Projection

The data in this table highlights three critical trends that define John’s retirement:

The “Forced Depletion” Effect:

While John’s portfolio continues to earn a healthy 6% return, the mandatory withdrawal rate eventually overtakes the growth rate.

Persistent OAS Clawback:

Because his mandatory withdrawals stay well above the $95,323 threshold for most of his retirement, John loses a significant portion of his OAS benefit every single year. In the 11th year of retirement, when the RRIF withdrawal becomes $126,159, John loses all OAS payment to OAS clawbacks!

The Mounting Tax Bill:

Even after his lifestyle needs are met, John is forced to withdraw “excess” money that is taxed at his highest marginal rate. Over the retirement period, John pays a staggering $1,123,331 in combined taxes and clawbacks.

By contrast, because TFSA withdrawals are not considered income, Bob’s total tax bill during the same retirement phase is under $35,000.

The “Surplus Income” Reality

During this later phase of retirement, John’s after-tax income significantly exceeds his actual spending needs of $48,000 per year. However, he does not have the flexibility to simply reduce his withdrawals; RRIF rules mandate that he take out a predefined minimum percentage every year, regardless of his lifestyle requirements.

Based on the OAS clawbacks and higher taxes John pays, it might appear that Bob has pulled ahead. However, a raw comparison shows that John’s after-tax income throughout retirement remains significantly higher than Bob’s. To ensure a true “apples-to-apples” comparison, we must ask: What happens if John invests this excess income instead of spending it? In the following section, we analyze how allocating this surplus to a TFSA and a non-registered account affects the final outcome.

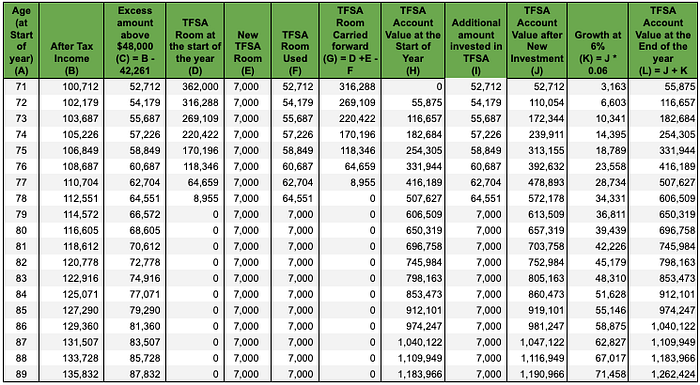

John Invests the Extra Income

As shown in Column H of Figure 1, John’s forced RRIF withdrawals provide him with far more cash than he needs. Rather than increasing his lifestyle spending, John diligently reinvests every spare penny, starting with his TFSA.

Because John prioritized his RRSP during his working years and never contributed to a TFSA, he enters retirement with a massive amount of accumulated “catch-up” room. Assuming the annual TFSA limit has averaged $7,000 (inflation-adjusted), his total available contribution room at age 65 is approximately $362,000.

Figure 2 (below) illustrates John’s strategy of funnelling his RRIF surplus into this tax-sheltered space, allowing it to grow at a 6% annual real (inflation-adjusted) rate.

The Transition at Age 79

Initially, John’s ample carried-forward contribution room allows him to shelter all surplus income above $48,000 within his TFSA. However, by age 79, he exhausts his accumulated “catch-up” room and is thereafter limited to the standard annual TFSA contribution of $7,000.

Despite this ceiling, John’s TFSA remains a powerful wealth-builder, compounding tax-free at a 6% inflation-adjusted rate. By the time he reaches age 90, his TFSA balance alone has grown to a significant $1,262,424.

Dealing with “Tax Drag”

During the final 11 years of this projection, John’s forced RRIF withdrawals continue to climb, far exceeding his available TFSA room. He directs this remaining overflow into a non-registered account.

Unlike the TFSA, this account is subject to “tax drag.” Because dividends and interest are taxable in the year they are received, the effective rate of return is suppressed. Without diving into the complex arithmetic — which lies beyond the scope of this article — John’s non-registered account is projected to reach $1,121,354 by age 90. This balance includes an unrealized (and eventually taxable) capital gain of $237,549.

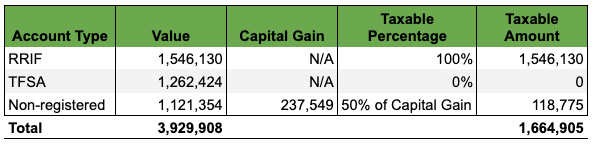

The Final Estate Summary (Age 90)

By age 90, John has successfully managed his forced RRIF withdrawals by reinvesting his surplus. His total wealth across all accounts is impressive, as shown:

The Terminal Tax Bill

If John were to pass away at age 90, the Canada Revenue Agency (CRA) would treat his assets very differently. While the TFSA balance ($1.262M) flows to his estate entirely tax-free, the other accounts trigger a massive final tax event:

- RRIF Inclusion: The full balance of his RRIF ($1,546,130) is included as taxable income on his final return.

- Capital Gains: 50% of the unrealized capital gains in his non-registered account ($237,549) also become taxable.

- The 53.5% Bracket: This massive spike in income — totalling over $1.66M in a single year — pushes John into the highest marginal tax bracket. In Ontario, this means more than half of his registered savings could be lost to taxes.

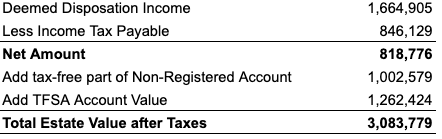

The following summary presents the final tax return and the net value of the estate after all applicable taxes have been paid.

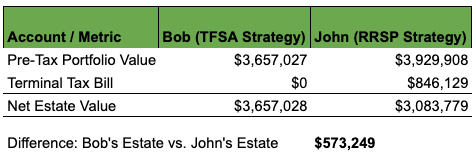

6. Comparing Bob’s and John’s Retirement Journeys

If both Bob and John were to pass away at age 90, the net values of their estates — after settling all final taxes — tell a definitive story.

Despite earning the same salary and living the same lifestyle, Bob leaves behind $573,249 more than John. ($3,657,028 vs $3,083,779)”

The Illusion of Wealth

At first glance, this outcome seems impossible. John entered retirement “ahead,” with a $1.6M RRSP compared to Bob’s $1M TFSA. Yet, despite starting with 60% more capital, John leaves a legacy that is half a million dollars smaller.

John’s “mountain of gold” was an illusion; a massive portion of it never actually belonged to him — it belonged to the CRA.

7. Final Takeaway: RRSPs Aren’t “Bad” — But They’re Often Misused

This analysis proves that for middle-income Canadians — including those earning $80,000 annually — the TFSA-first strategy is often superior to the conventional RRSP-first wisdom. Just as we saw in our previous $66,000 income case study, the “tax-free out” of a TFSA consistently beats the “tax-deduction in” of an RRSP over the long term.

The Three Pillars of the “RRSP Trap”

Why did John’s larger portfolio underperform? He fell victim to the three structural traps we’ve explored in this series:

- The Bracket Trap: Mandatory RRIF withdrawals forced John into a higher tax bracket than he was in during his working years.

- The OAS Hit: Those same withdrawals triggered the “Recovery Tax,” effectively acting as a 15% surcharge on his income.

- The Estate “Income Dump”: Upon death, the remaining RRIF was taxed as if John earned it all in a single year, triggering a tax rate of over 50%.

The Core Lesson

The real risk for Canadians isn’t failing to save; it is deferring taxes without a clear exit strategy. Before you maximize your next RRSP contribution, ask yourself:

- Will my mandatory income trigger a clawback of my government benefits?

- How much of my children’s inheritance am I accidentally signing over to the CRA?

The Bottom Line: Your contribution decisions determine your tax refund today, but your withdrawal strategy determines your true wealth tomorrow.

What’s Next?

The choice between a TFSA and an RRSP isn’t a one-size-fits-all decision — it changes dramatically as your career and income progress. To help you navigate these shifts, I am continuing this series with a focus on the next major income milestone:

- The $120,000 Earner Analysis (Coming Soon): Conventional wisdom says that six-figure earners must use RRSPs for the high upfront tax refund. We’ll put that to the test to see if a 43% tax break today can survive a 53% RRIF “tax bomb” and the total loss of OAS benefits tomorrow.

- The RRSP Meltdown Strategy: If you already have a large RRSP, you aren’t necessarily stuck with John’s fate. In my latest guide, I explore “Meltdown” techniques — such as early strategic drawdowns and tax-bracket smoothing — designed to strip money out of your RRSP at a lower tax rate today to avoid a massive tax hit later.

Check out the guide: RRSP Meltdown Explained: A Plain English Guide for Canadian Retirees.

Master the Exit Strategy: Income Splitting

As we saw with John’s $573,249 estate shortfall, the real danger of the RRSP is the “tax concentration” at death. If you are a high earner or part of a dual-income household, these guides will help you dismantle that tax bomb before it goes off:

- Income Splitting for Canadians: Start here for a comprehensive overview of how to shift income from a high-earning spouse to a lower-earning one.

- Spousal RRSP for Income Splitting: The most effective way to balance your retirement accounts decades before you retire, ensuring neither spouse gets pushed into a “punitive” tax bracket.

- Pension Income Splitting: Learn how to split RRIF and pension income at age 65 to protect your OAS and lower your household’s combined tax bill.

Stay tuned as we continue to dismantle the myths of Canadian retirement planning and help you keep more of what you earn!

Disclaimer: This article is for educational purposes only and is not financial or tax advice. Please consult a qualified tax or financial professional before making any decisions.

What are your thoughts on this post? Share your comments with us.

Stay ahead of the curve. Subscribe here to get notified whenever I publish a new guide or tool.

Share your comment or feedback. We'll get back to you as soon as we can.