The RRSP vs. TFSA Guide for Canadians Earning Under $60,000

Why the TFSA Often Beats the RRSP for Lower-Income Earners — In Plain English

This is my third article for The Canadian Investment & Retirement Roadmap, and this time, I want to talk directly to Canadians who earn under $60,000 per year — because the advice they receive is often generic, incomplete, or simply wrong.

For decades, RRSPs have been promoted as the default retirement plan for everyone. Financial advisors, banks, and even workplace seminars discuss RRSPs as if they are automatically the smartest first choice. But the truth is very different for lower-income and lower-middle-income Canadians.

RRSPs can be powerful — but only if the tax you save when you contribute is higher than the tax you pay when you withdraw. And that’s the part most Canadians never hear clearly explained.

Why I chose the $60,000 income cutoff

If you earn less than about $60,000, you’re already in Canada’s lowest federal tax bracket (ending at $57,375 in 2025). That means you’re paying the lowest rate available — and there’s no lower bracket to “drop” into when you eventually withdraw from your RRSP.

In other words, RRSP contributions cannot lower your tax rate if you’re already in the lowest bracket.

And here’s the key problem: If your RRSP grows over time (as it should), your withdrawals later in life may easily push you into a higher tax bracket than you’re in today. That means you could end up paying more tax in retirement than you saved during your working years.

So for Canadians earning under $60,000, the math often flips:

The RRSP may not just be less beneficial — it can actually leave you worse off.

I want every lower-income Canadian to understand what the banks, and even most financial advisors, won’t always tell you: the TFSA is usually the smarter, safer, and more flexible first choice.

Growth of Money in RRSP and TFSA is Exactly the Same

It’s a common myth that because you put untaxed money in an RRSP and tax-paid money in a TFSA, and because money grows tax-free in both accounts, you’ll end up with more money in an RRSP at retirement. Let’s look at a practical example.

Both John and Bob earn $52,000 a year and live in Ontario.

- John contributes $6,000 to his RRSP. Because RRSP contributions are tax-deductible, he pays no tax on this $6,000, so the full amount goes into his RRSP. (He only pays tax on $46,000 of his income.)

- Bob wants to contribute $6,000 to his TFSA account. Since TFSA contributions are made with after-tax money, he must first pay tax on $6,000. At a combined Federal and Ontario tax rate of 19.55% in 2025, he can invest only $4,827 in his TFSA ($6,000 − $1,173 tax).

Now, assume both accounts grow at 6% annually for 25 years, and at the end, the entire amount is withdrawn. Who ends up with more money: John or Bob?

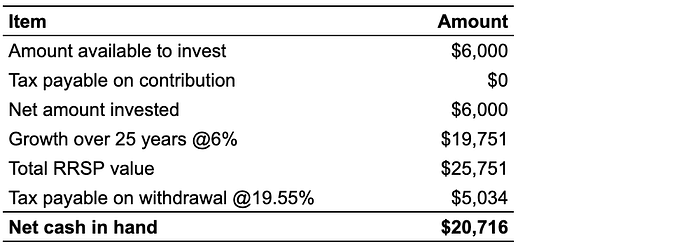

John’s RRSP

John’s $6,000 grows by $19,751 over 25 years, reaching $25,751. When he withdraws, he pays tax on the entire amount, leaving him with $20,716.

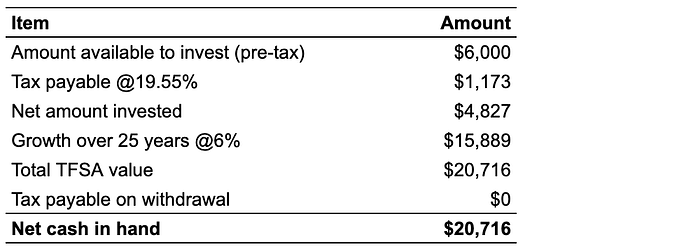

Bob’s TFSA

Bob pays tax upfront, so he invests $4,827. Over 25 years, this grows to $20,716. Since TFSA withdrawals are tax-free, he keeps all $20,716.

✅ The takeaway: At the end, the net cash in hand is exactly the same whether you use an RRSP or a TFSA, assuming the same pre-tax contribution, tax rate, and growth.

This illustrates a key point: the growth of money in RRSPs and TFSAs is identical — the difference is only in when you pay the tax.

RRSP may Push You in a Higher Tax Bracket

If you save a lot in your RRSP, large withdrawals may push you into a higher tax bracket, meaning you pay more tax on the money you take out.

For example, assume you earn $50,000 per year (in the lowest tax bracket) and need $30,000 for an emergency. Withdrawing from your RRSP may require a larger withdrawal — perhaps $40,000 — to cover taxes. Your total income for that year would then be $90,000, pushing you into a higher tax bracket. When you contributed, you saved roughly 19.55% in tax. But now you could end up paying close to 30%.

By contrast, a TFSA withdrawal is completely tax-free. You can withdraw exactly $30,000 with no impact on your taxes.

RRSP Withdrawals May Reduce Old-Age Benefits

RRSP withdrawals can affect income-tested government benefits, including:

- GIS (Guaranteed Income Supplement)

- OAS (Old Age Security)

- Age Amount Tax Credit

- GST/HST Refund

GIS is most affected for low-income retirees.

For example, consider Maya, 65, a single senior with full OAS and $7,200 CPP annually:

- Based on $7,200 of CPP income (OAS is not included in the GIS calculation), she receives $8,369 per year in GIS.

- If she withdraws $6,000 from her RRSP, her total income for calculation of GIS increases to $13,200, and accordingly her annual GIS drops to $4,610, a reduction of $3,759.

- As TFSA withdrawals are not included in the yearly income while calculating GIS, it does not affect GIS. Therefore, Maya will have an additional $3,759 income in hand if she withdraws $6,000 from TFSA instead of RRSP.

This demonstrates a major advantage of TFSAs: retirees keep more of their money.

Note: GIS numbers are based on Nov 2025 published data and may change in future.

In the same way, RRSP withdrawals also reduce the Age Amount tax credit and the GST/HST credit. Although it’s uncommon for low-income retirees, large RRSP withdrawals can also trigger the OAS clawback.

So Which One Should Lower-Income Canadians Use?

If your income is under about $60,000, then:

The TFSA is usually the better choice.

Why?

- Your RRSP deduction is small or insignificant

- Your withdrawal tax rate won’t be lower later

- You may pay more tax in retirement

- RRSP withdrawals can reduce income-tested benefits

- TFSA withdrawals never affect taxes or income-tested benefits

RRSPs can still be worthwhile for lower-income Canadians who receive employer matching contributions, but in most cases, the TFSA still comes out ahead.

Disclaimer: This article is for educational purposes only and is not financial or tax advice. Please consult a qualified tax or financial professional before making any decisions.

What are your thoughts on this post? Share your comments with us.

Stay ahead of the curve. Subscribe here to get notified whenever I publish a new guide or tool.

Share your comment or feedback. We'll get back to you as soon as we can.