RRSP Explained in Plain English

A simple, practical guide to contribution room, deductions, withdrawals, and how the RRSP really works

While the TFSA is the most flexible and universally beneficial account for Canadians, the RRSP — the Registered Retirement Savings Plan — is often viewed as the most powerful retirement savings tool, especially for individuals with moderate to high incomes. At least, that’s what most financial advisors and planners say. But as with most things in Canadian personal finance, it’s not as simple as it sounds.

RRSPs are misunderstood even more than TFSAs. Before we explore whether a TFSA or RRSP is better, or who actually benefits the most from contributing to one, it’s important to start with a clear, plain-English explanation of what an RRSP really is — and what it is not.

1. What an RRSP Actually Is

RRSPs were introduced in Canada in 1957 to encourage Canadians to save for retirement by offering specific tax advantages. In simple terms:

- When you contribute (invest) some money in an RRSP account, you don’t pay any tax on that investment on your tax return for that year (or for the year in which the RRSP contributions are claimed). You can make an RRSP contribution in 2025 and claim the deduction on your 2025, 2026, or 2027 tax return. (More on this flexibility later.)

- Your investments grow tax-free while inside the account.

- You pay tax only when you withdraw, usually in retirement.

- You can have one or multiple RRSP accounts, depending on your financial institutions or investment preferences.

What can you hold inside an RRSP? Almost anything:

- Canadian, US and global Stocks

- ETFs and index funds

- Mutual funds

- Bonds

- GICs

- Cash

RRSPs are especially useful for holding U.S. dividend-paying stocks and ETFs, because they are exempt from the 15% U.S. withholding tax (something TFSAs cannot avoid).

What you can’t hold:

Certain assets are not RRSP-eligible, such as unlisted private securities, physical gold, and cryptocurrencies like Bitcoin or Ethereum. However, crypto ETFs and gold ETFs are eligible, which is how most investors get exposure to those assets inside an RRSP.

In a nutshell, RRSPs offer three major benefits:

- A tax deduction when you contribute

- Tax-deferred growth while the money is invested

- Fully taxable withdrawals later, including your original contribution

This structure allows you to defer tax today, grow investments without tax drag, and pay tax only when money comes out.

2. Contribution Room — How It Works

Every year, you earn new RRSP contribution room based on the previous year’s earned income. As of 2026, the formula is:

18% of last year’s earned income, up to an annual maximum of $33,010.

Earned income includes:

- Salary or wages

- Self-employment income

- Net rental income

- Certain disability payments

Earned income does not include:

Investment income, dividends, interest, pension income, or CPP/OAS.

CRA provides your total RRSP contribution room on your Notice of Assessment, and you can also view it in CRA My Account.

Unused RRSP room carries forward forever

If you don’t contribute in a given year, the unused room carries forward indefinitely. You can use it in any future year, even decades later.

The “First 60 Days” Rule

Unlike most tax deadlines that end on December 31, the RRSP gives you extra time. You can make contributions for a specific tax year up to 60 days into the following calendar year.

- The Moving Deadline: In most years, this deadline is March 1. However, if that day falls on a weekend or a holiday, the CRA extends it to the next business day.

- Example: For the 2025 tax year, March 1, 2026, is a Sunday. Therefore, the official deadline is Monday, March 2, 2026.

- Leap Years: In leap years (like 2028), the 60th day actually falls on February 29.

- This “grace period” allows you to calculate your final income for the year and make a last-minute contribution to lower your tax bill.

Dual-Purpose Window:

RRSP contributions made in the first 60 days of the year give you flexibility. You can apply them to the previous tax year to generate an immediate refund, or carry them forward and deduct them in the current tax year, based on the new contribution room you earned on January 1.

Pro-Tip: Don’t Skip the Paperwork:

If you make an RRSP contribution in the first 60 days of the year, you must still report it on your tax return for the previous year — even if you don’t plan to claim the deduction yet. This notifies the CRA that the contribution was made and should be tracked as an unused contribution, available for you to deduct in a future year when it’s most beneficial.

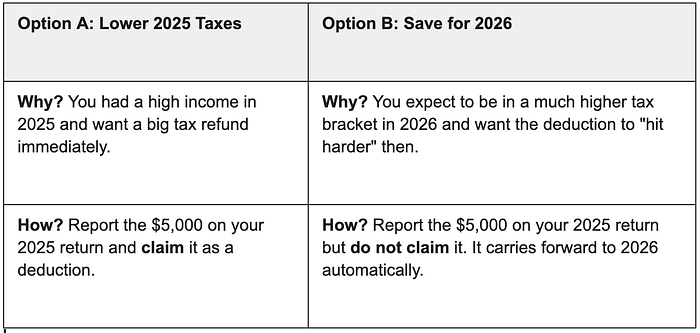

Strategy in Action: The March Decision:

Imagine it is February 2026, and you contribute $5,000 to your RRSP. You have two ways to use that receipt:

Watch Out: The Over-Contribution Penalty

It is important not to exceed your total contribution limit. If you contribute more than your allowed room:

- The $2,000 Buffer: The CRA allows a lifetime cumulative over-contribution of $2,000 without penalty (essentially a “math error” cushion).

- The Penalty: If you exceed your limit by more than $2,000, you will be charged a 1% monthly tax on the excess amount.

Because 12% per year is a very steep price to pay, it is always best to double-check your limit on your latest Notice of Assessment before making a large contribution.

Note: For more details on RRSP Contribution Rules, see Understanding RRSP Overcontribution Rules.

Important: No Income — No New Room

Unlike the TFSA, RRSP contribution room is tied directly to earned income. If you don’t earn income in a given year, you do not generate new room for the next year.

3. How the RRSP Tax Deduction Works

This is where much of the confusion around RRSPs begins.

When you contribute to your RRSP, you receive a tax deduction that reduces your taxable income for the year.

Example:

- Income: $100,000

- RRSP contribution: $10,000.

- You are taxed as if you earned $90,000

Because of this reduction in taxable income, most people receive a tax refund.

A refund is not “free money”

Many people mistakenly think the refund is a bonus from CRA.

It isn’t.

Your employer deducts income tax from every paycheque based on your full income. That means you already prepaid tax on the $10,000 you later contributed to your RRSP. When you file your tax return, CRA simply returns the tax you overpaid — because your taxable income was reduced after the fact.

In other words:

- You paid tax on $100,000 during the year

- You should have paid tax on $90,000

- CRA refunds the difference

- You essentially gave the government an interest-free loan for up to a year

💡 Tip: Reduce tax withheld from your paycheques

If you regularly contribute to your RRSP, you can avoid overpaying tax in the first place.

Submit Form T1213 — Request to Reduce Tax Deductions at Source to CRA (usually in November for the following year).

If approved, give the letter to your employer so they deduct less tax from each paycheque — meaning you get the benefit of the RRSP deduction throughout the year instead of waiting for a refund.

💡 Tip: Contribute now, deduct later

You can contribute to your RRSP now, but delay claiming the deduction until a future year.

This makes sense if:

- You expect to move into a higher tax bracket, or

- Your income will rise significantly in the near future.

Because RRSP deductions reduce income from the top, a $10,000 deduction saves much more tax at a $120,000 income than at a $70,000 income. Delaying the deduction can therefore increase your tax refund, or reduce your tax payable when your income is higher.

4. Withdrawals — When and How They Are Taxed

This is the part most Canadians misunderstand.

All RRSP withdrawals are taxable as income.

You can withdraw money from your RRSP at any time, even before “retirement.” But every withdrawal has tax consequences.

If you withdraw $20,000 from your RRSP:

- It is added to your income for that year

- Your financial institution withholds 10–30% at the time of withdrawal, depending on the amount and type of withdrawal.

- You ultimately pay tax at your marginal tax rate, which may be higher or lower than the withholding.

- A higher income for that year may reduce income-tested benefits like the GST/HST Credit, GIS, and OAS.

- You cannot recontribute the amount withdrawn. Once taken out, that RRSP contribution room is permanently lost.

There are only two exceptions: withdrawals that do not have the withholding tax at the time of withdrawal:

- Home Buyers’ Plan (HBP) — withdrawals must be repaid over 15 years.

- Lifelong Learning Plan (LLP) — withdrawals must be repaid over 10 years.

Most withdrawals occur after retirement, either directly from the RRSP or from the RRIF (Registered Retirement Income Fund) account(s).

5. Converting RRSPs to RRIFs

You can keep your RRSP until the end of the year you turn 71. However, by December 31 of that year, it must become:

There is no minimum age to convert an RRSP into an RRIF. While most Canadians wait until age 71, some convert earlier for tax-planning reasons. You can also convert only part of your RRSP and leave the rest untouched.

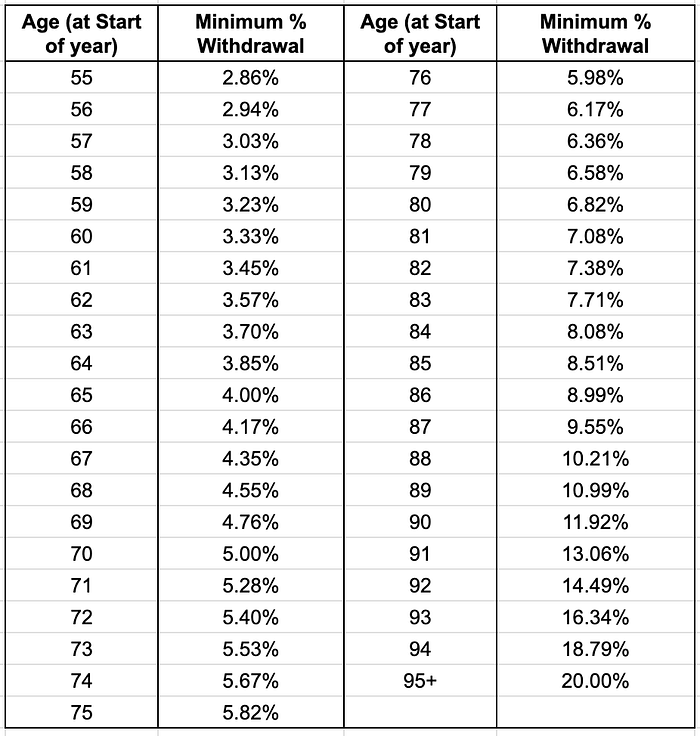

However, once you open a RRIF, you must begin mandatory annual withdrawals in the following year. The minimum withdrawal percentage is determined by your age (or your spouse’s age, if elected) and increases each year as you get older.

The table below shows selected minimum RRIF withdrawal rates for ages 55 and above.

As mentioned earlier, RRIF withdrawals always begin in the year after you set up the account. For example, if you open your RRIF in the year you turn 71, your first minimum withdrawal occurs at age 72, based on the account value on January 1 of that year.

This requirement is one of the major drawbacks of building a very large RRSP. Mandatory withdrawals can force you to take out more than you need — potentially pushing you into a higher tax bracket in retirement.

6. What Happens to Your RRSP/RRIF When You Die

When an RRSP or RRIF holder dies, the tax outcome depends on who inherits the account.

1. Rollover to a Spouse or Common-Law Partner

If your spouse or common-law partner is named as the beneficiary on your RRSP contract — or as the successor annuitant on your RRIF — the full value of the account can be transferred to their RRSP or RRIF on a tax-deferred basis.

In practice:

- The funds pass directly to the surviving spouse.

- The transfer bypasses the estate, avoiding probate fees in most provinces, except in Quebec, where most beneficiary designations must be made through a Will.

- No tax is paid at your death.

- Your spouse will pay tax only when they withdraw funds from their RRSP/RRIF.

This is the most tax-efficient outcome.

2. The Importance of Naming Your Spouse or Common-Law Partner as a Direct Beneficiary on Your RRSP/RRIF

If you fail to name your spouse or common-law partner as a direct beneficiary:

- Full Value Taxed: The entire RRSP/RRIF is included in the deceased’s final income tax return.

- High Tax Rate: The lump sum may push income into the highest tax bracket (≈50%).

- Estate Pays: Taxes reduce the net inheritance for your spouse or other heirs.

💡 Workaround: A rollover to a spouse is sometimes possible via CRA forms (T2019/T1090), but it is messy, slow, and risky compared to simply naming the spouse as beneficiary or successor annuitant.

✅ Best practice: Always name your spouse/common-law partner directly.

If you have no surviving spouse or choose not to pass your RRSP/RRIF to them, you can name a child or another person as beneficiary. In this case, the full value is included in your final tax return, and the beneficiary receives the account value after taxes.

Planning for the eventual transfer of your RRSP or RRIF is critical — the tax outcome can vary widely depending on your beneficiary choices.

3. When the Last Surviving Spouse Dies

Once the surviving spouse passes away, there is no further rollover available. The entire RRSP/RRIF balance becomes fully taxable on their final tax return, often pushing income into the highest tax bracket. Whatever remains after tax goes to the beneficiaries.

This is why strategies like gradually drawing down RRSPs/RRIFs (“RRSP meltdown”) can help reduce the eventual tax burden on the estate — and I will cover this strategy in a future article.

7. Common Misunderstandings About RRSPs

❌ “RRSPs are always good — put as much as you can!”

Not necessarily. The benefit depends heavily on your income today versus your income in retirement. As I will explain in a future article, RRSPs are most advantageous only for some Canadians.

❌ “RRSP refunds are free money.”

They’re not. Refunds simply return prepaid tax you already contributed through your withholdings.

❌ “RRSPs help low-income Canadians.”

Generally, they do not. If your income is low, the tax deduction provides little value, and future RRSP/RRIF withdrawals may reduce important income-tested benefits like the GIS (Guaranteed Income Supplement).

❌ “RRSP withdrawals only affect taxes.”

Withdrawals can also affect several income-tested benefits and credits, including:

- GIS (Guaranteed Income Supplement)

- GST/HST Credit

- The Allowance / Allowance for the Survivor

- Age Amount

- OAS clawback

❌ “I don’t need to name a beneficiary on my RRSP/RRIF — it automatically goes to my spouse or children.”

If you don’t, the account usually passes to your estate, and the full RRSP/RRIF value is included in your final tax return, often resulting in a huge tax bill for your heirs. Naming a beneficiary or successor annuitant avoids this and is far more tax-efficient and straightforward.

8. When RRSPs Work Best

RRSPs are most effective when:

- Your employer offers RRSP matching.

If your employer offers an RRSP matching program, they will contribute to your RRSP based on your own contributions — typically matching up to 100% to a maximum percentage, such as 5%. This is effectively free money.

For instance, with an annual income of $100,000 and a 5% matching program, contributing $5,000 would result in an additional $5,000 from your employer. Your RRSP balance becomes $10,000 instantly. Always take full advantage of this opportunity. - Your income today is high, and your income in retirement will be lower.

In this case, the tax deduction today is valuable, and withdrawals later will be taxed at a lower rate. This only works if you invest the tax refund, not spend it. - You want to defer tax strategically.

RRSPs can be useful for long-term planning and tax smoothing, especially when coordinated with withdrawal strategies, RRIF conversion timing, and government benefits.

📌 Additional Benefit for Parents: RRSP Contributions Can Increase Your Canada Child Benefit (CCB)

One often-overlooked advantage of RRSP contributions is their positive impact on the Canada Child Benefit (CCB).

The CCB is an income-tested benefit. Its payments are based on your Adjusted Family Net Income (AFNI). Because RRSP contributions are a tax deduction, they effectively reduce your net income, which in turn reduces your AFNI. When your AFNI drops, the government’s mandatory CCB clawback decreases, which means your monthly CCB payments increase.

This provides a powerful double benefit for parents: an immediate tax reduction and an increase in their Canada Child Benefit (CCB) payments.

The exact increase in CCB payments depends on your AFNI, the number of children, and their ages. However, the immediate benefit of the AFNI reduction is substantial.

As a general idea, for every $1,000 contributed to an RRSP, the resulting increase in your annual CCB payments will typically fall within the range of $32 to $135, as per 2024 tax year rates.

- The lower end ($32) applies to families with one child and higher AFNI (over $81,222).

- The higher end ($135) applies to families with two or more children whose AFNI falls in the mid-income range ($37,487 to $81,222), where the highest CCB reduction rate applies.

By strategically timing and maximizing your RRSP contributions, you can effectively lower your tax bill while putting more money back into your pocket every month through increased CCB payments.

9. When RRSPs May Not Be the Best Choice

RRSPs are less effective when:

- Your income is low or modest

- You expect a similar or higher income in retirement

- RRIF minimum withdrawals may push you into higher tax brackets

- You may qualify for GIS (RRSP/RRIF withdrawals reduce it)

- You need flexibility, or may need access to your money earlier

10. Final Thoughts

RRSPs are a powerful tool — but not always the right tool. For decades, Canadians have been told to “max out your RRSP” without understanding how the tax rules work or how forced RRIF withdrawals could affect them later in life.

The RRSP can save you a lot of tax, or it can cost you a lot of tax. It all depends on timing, your income level, and how you use it.

Continue Your Roadmap

If you’re wondering where to go next, I’ve broken down the RRSP strategy for different income levels and retirement stages:

- Earning under $60,000? You might be better off prioritizing your TFSA. Read: The RRSP vs. TFSA Guide for Canadians Earning Under $60,000

- Earning around $80,000? This is the “danger zone” where the wrong choice can be costly. Read: The RRSP vs. TFSA vs. Non-Registered Guide for Canadians Earning $80,000

- Worried about the “Success Penalty”? Learn why saving too much in an RRSP can lead to a massive tax bill later. Read: The RRSP Trap: Why Middle-Class Canadians Should Be Careful (Part 1)

- Planning your exit strategy? While your RRSP must close at 71, many choose to roll it into a RRIF to provide a steady income. Read: RRIF Explained in Plain English and RRSP Meltdown Explained: A Plain English Guide for Canadian Retirees

The goal of The Canadian Investment & Retirement Roadmap is to help you move from “blind trust” in generic advice to a sophisticated plan that keeps more money in your pocket.

Disclaimer: This article is for educational purposes only and is not financial or tax advice. Please consult a qualified professional before making any decisions.

What are your thoughts on this post? Share your comments with us.

Stay ahead of the curve. Subscribe here to get notified whenever I publish a new guide or tool.

Share your comment or feedback. We'll get back to you as soon as we can.