RRSP Meltdown Explained: A Plain English Guide for Canadian Retirees

Why waiting until age 71 to withdraw from your RRSP might be the costliest mistake of your retirement.

Many Canadians follow the traditional advice to maximize RRSP contributions and wait until age 71 to convert to a RRIF, aiming for maximum tax-deferred growth. While this sounds logical, it often creates a “tax bomb”: a massive RRIF balance that triggers large mandatory withdrawals, high tax bills, and the dreaded OAS clawback.

As I explored in The RRSP Trap and my guide for earners making $80,000, your hands are often tied by the time you reach your 70s. However, if you are in your 60s, you have a window of opportunity to pivot. It’s time to talk about a strategy that can save you thousands of dollars in taxes during retirement: the RRSP Meltdown.

How the RRSP Meltdown Works (The Mechanics)

At its core, an RRSP Meltdown involves intentionally withdrawing money from your RRSP earlier than required, using a tax-efficient strategy.

If the “RRSP Trap” is the problem, the RRSP Meltdown is the escape. Instead of paying very little tax in your 60s and then facing much higher taxes in your 70s and 80s, you spread your taxes more evenly throughout retirement.

Think of your RRSP like a large block of ice. If you wait until age 72, the government suddenly turns the heat way up, and the ice melts quickly — creating a flood of taxable income. With an RRSP Meltdown, you control the heat earlier, while you’re still in your 60s.

The goal is simple: smooth out your lifetime taxes. You choose to pay some tax earlier at a lower rate, rather than being forced to pay much higher rates later.

What Actually Happens (In Plain English)

During the years after you retire — but before mandatory RRIF withdrawals begin — you slowly draw down your RRSP. You withdraw only as much as makes sense at your current tax rate, instead of letting the account grow untouched.

After paying the tax, the money you withdrew doesn’t sit idle. It is reinvested — typically into a TFSA, where future growth is tax-free, and/or into a non-registered account.

Note: Of course, TFSA contributions are limited by available contribution room, so any excess is invested in a non-registered account.

When this approach is combined with delaying CPP and OAS, the RRSP Meltdown becomes even more effective, because your taxable income in those early retirement years stays lower.

Over time, this reduces the size of your RRSP. By the time you reach age 72:

- Your RRSP balance is smaller

- Required withdrawals are lower

- Your tax bracket stays more manageable

- Your OAS benefits are less likely to be clawed back

This isn’t about avoiding taxes — it’s about controlling when you pay them.

To see how an RRSP Meltdown works in practice, let’s walk through a simple example.

A Tale of Two Retirees: The Cost of Waiting

To see the power of the Meltdown in action, let’s look at two neighbours living in Ontario: John and Linda.

Both are 65 years old and recently retired. Both have worked hard to save $1,359,888 in their RRSPs. They each need about $42,498 per year (after-tax) to maintain their lifestyle. While their starting points are identical, their strategies are opposites.

1. John: The “Wait and See” Strategy

John follows the traditional path I explored in The RRSP Trap: The $1M Reality Check. He wants to keep his tax bill as low as possible today.

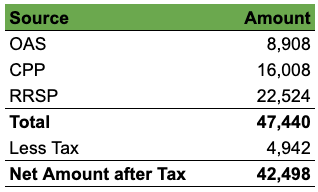

- Age 65–71: John withdraws only $22,524 from his RRSP annually, supplementing it with OAS and CPP. He pays very little tax (roughly $4,942) and feels like he’s winning.

- The Balloon Effect: Because John is barely touching his capital, his RRSP continues to grow. Assuming a 6% real growth rate (inflation-adjusted), his account balloons to $1,762,460 by the time he turns 71.

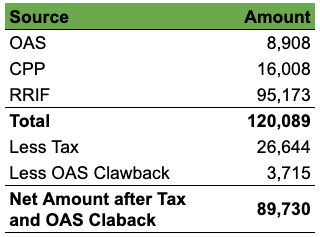

- Age 72 (The Trap): Now, the government steps in. John is forced to convert to a RRIF and withdraw a minimum of 5.4% of $1,762,460, i.e $95,173.

- The Result: His mandatory withdrawal is now $95,173. When added to his OAS and CPP, his total income spikes to $120,089. Based on 2026 tax rates, John is now in a much higher bracket and faces a significant OAS clawback. He is effectively paying a “success penalty” on his savings in RRSP.

The following is his tax summary during the 7th year of retirement as per 2026 tax rates.

2. Linda: The “RRSP Meltdown” Strategy

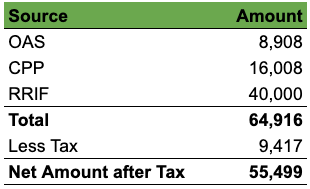

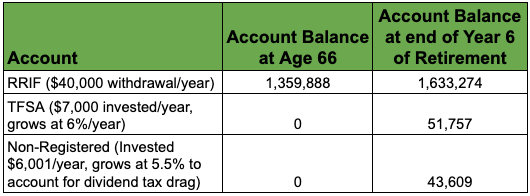

Linda decides to “melt” her account early. Even though she doesn’t need the extra cash to live on, she converts her RRSP to a RRIF immediately at age 65 and starts withdrawing $40,000 every year.

- Age 65–71: Linda pays slightly more tax today because her income is higher.

However, she takes that “extra” $13,001 in after-tax cash and moves it into her TFSA and a non-registered account. By shifting money from the “taxable” bucket (RRIF) to her TFSA and non-registered account, she is proactively protecting her future self. She is moving funds away from an account where every dollar is taxed as income and into accounts that offer tax-free growth and preferential tax treatment.

After six years, here is a summary of her accounts, assuming she contributes $7,000 to her TFSA each year and invests $6001 in a non-registered account.

Note: Linda can maximize this strategy if she has extra TFSA room available. By investing more funds into her TFSA, she increases her tax-free growth potential and ensures that those assets remain tax-exempt throughout her retirement.

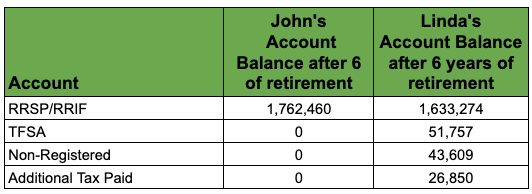

Here is a side-by-side summary comparing Linda, who withdraws $40,000, with John, who withdraws $22,524, after the first six years of retirement.

Age 72 (The Payoff): After six years of “melting,” Linda has accomplished three major goals:

- Lower RRIF Balance and OAS Protection: Her balance is roughly $129,186 lower than John’s. This decreases the RIIF withdrawal in the 7th year of retirement by almost $7,000, resulting in lower tax and reduced OAS clawback.

- A Tax-Free Powerhouse (TFSA): Linda now has a TFSA balance of $51,757. Because this account is fully tax-sheltered, every dollar of growth stays in her pocket. At a 6% real growth rate (inflation-adjusted), this single account is expected to be worth $156,595 over the next 19 years — wealth she can spend whenever she wants without ever paying another cent in tax.

- Strategic Flexibility (Non-Registered): She also has $43,609 in a non-registered account. Even accounting for “dividend drag,” the account is estimated to grow at a 5.5% annual rate to roughly $143,121 over the next 19 years. Unlike RRIF withdrawals — which are taxed at 100% as ordinary income — withdrawals from this account are taxed favourably.

💡 Pro-Tip: Watch Out for the “Dividend Gross-Up”

In a non-registered account, Canadian dividends are taxed in the year they are earned. However, for tax purposes, eligible dividends are “grossed up” by 38%. This means if you receive $1,000 in cash dividends, the CRA views your income as $1,380 when calculating your total net income.

If your retirement income is nearing the OAS clawback threshold ($95,323 for 2026), this “phantom income” could trigger a benefit reduction. To protect your OAS, consider holding dividend-heavy stocks inside your TFSA and focusing on capital-growth investments (like certain ETFs or stocks that pay little to no dividends) in your non-registered account.

The following table illustrates the comparative tax and OAS clawback summary for John and Linda in the 7th year of retirement.

The lower tax burden and reduced OAS clawback will continue throughout the rest of Linda’s retirement.

What Could Linda Do to Proactively Reduce Her RRSP?

One of the best decisions Linda could make is to stop contributing to her RRSP in her 60s. Instead, she could direct new savings toward her TFSA and non-registered accounts.

In addition, Linda could choose to make extra withdrawals from her RRSP, as long as those withdrawals do not push her into a higher tax bracket. For example, if her taxable income is $66,000, she would be in the middle Ontario tax bracket (29.65%), which extends up to $94,907 (based on 2026 Ontario tax rates).

This means she could withdraw up to $29,000 from her RRSP and still remain in the same tax bracket. Doing so would gradually reduce her RRSP (and future RRIF) balance, leading to lower taxes in later years and potentially reducing or eliminating OAS clawback.

Bonus: Two “Secret” Advantages of Early RRIF Conversion

Most people view the RRIF as the “end stage” of their savings, but converting a portion of your RRSP to a RRIF as soon as you turn 65 unlocks two major benefits that are unavailable to RRSP holders.

1. The $2,000 “Tax-Free” Gift (The Pension Income Tax Credit)

Once you turn 65, the Canadian government allows you to claim the Pension Income Tax Credit. This credit makes the first $2,000 of eligible pension income effectively tax-free at the federal level (and provides a similar credit provincially).

The catch? Simple RRSP withdrawals do not qualify for this credit. To claim it, the money must come from a RRIF (or a life annuity/pension).

By converting just enough of your RRSP to a RRIF to withdraw $2,000 a year, you are essentially “laundering” that money through the RRIF to make it tax-free. Over a decade, that’s $20,000 in income you’ve taken out without giving a penny of it to the CRA.

2. No Withholding Tax = Better Cash Flow

When you make a withdrawal from an RRSP, the bank is legally required to withhold tax (between 10% and 30%) and send it to the government immediately. You eventually get the difference back when you file your taxes, but you lose that ‘float’ for several months in the meantime.

The RRIF Advantage: There is zero withholding tax on the mandatory minimum withdrawal from a RRIF.

This gives you much better control over your cash flow. If your minimum withdrawal is $10,000, you get the full $10,000 in your pocket. You still report it as income and pay the tax at the end of the year, but in the meantime, you can keep that money working for you — or use it to fund your TFSA earlier in the year.

3. Pension Income Splitting

Another massive perk that begins at age 65 is Pension Income Splitting. This strategy allows you to split up to 50% of your eligible RRIF income with your spouse to lower your combined tax bill.

It is important to note that this is not allowed with standard RRSP withdrawals — one of the many reasons to consider an early conversion. By using pension splitting, you aren’t just shifting income to a lower tax bracket; you are also reducing your individual “net income,” which can help you reduce or even completely avoid the OAS clawback. If one spouse is in a higher bracket, this “shift” can save a household thousands in both taxes and preserved benefits. For a deep dive into the mechanics of this move, see my article: Pension Income Splitting.

Final Thought: Don’t Let Age 71 Become an Expensive Mistake

The “RRSP Trap” is built on a single, outdated piece of advice: Wait until age 71 to touch your money. But as we’ve seen, “waiting” is often the most expensive choice you can make.

By initiating an RRSP Meltdown in your 60s, you aren’t just moving money; you are proactively taking control of your tax bill. Between preserving your OAS benefits, claiming the Pension Income Tax Credit, and utilizing Income Splitting, the cumulative impact isn’t just a few hundred dollars — it is a strategy that can easily save you tens of thousands of dollars in taxes over the course of your retirement.

Your retirement savings are the result of decades of hard work. Don’t let a “bloated RRIF” at age 72 hand a massive chunk of that effort back to the CRA. Start looking at your “gap years” today, and turn that tax trap into a tax-free legacy.

Disclaimer: This article is for educational purposes only and is not financial or tax advice. Tax rules can change and vary by province — especially in Quebec. Please consult a qualified tax or financial professional before making any decisions.

What are your thoughts on this post? Share your comments with us.

Stay ahead of the curve. Subscribe here to get notified whenever I publish a new guide or tool.

Share your comment or feedback. We'll get back to you as soon as we can.