The RRSP Trap: The Withdrawal Phase & The $1M Reality Check (Part 2)

How the “Double Whammy” of taxes and clawbacks can erase decades of diligent saving.

1. The Recap

In Part 1, we followed two average Canadians, John and Bob, through 35 years of savings. By age 65, the results seemed conclusive:

- John (RRSP): $1,359,868

- Bob (TFSA): $995,863

John has a $364,005 lead. Conventional wisdom says John is the winner. But as we enter the withdrawal phase, we’re about to see how the “tax-deferred” nature of the RRSP becomes a massive liability, while the “invisible” nature of the TFSA becomes a wealth-building superpower.

2. The Retirement Goal: $42,498

To keep this comparison fair, both men aim to maintain the same lifestyle they had while working: a net spending power of $42,498 per year.

In retirement, this money comes from three sources: Canada Pension Plan (CPP), Old Age Security (OAS), and their personal savings. For Bob, there is a “secret” fourth source: the Guaranteed Income Supplement (GIS).

The Government Dividend (2026 Rates)

To reach their spending goal of $42,498, John and Bob rely on three government pillars. Because we are assuming they have both lived in Canada since age 18, they qualify for the full amounts.

- OAS: $742.31/month ($8,908/year)

Note: This is based on a full 40 years of residency in Canada since turning 18. Those with fewer years receive a pro-rated amount. The OAS payments increase by 10% at age 75, though this increase is ignored in this analysis to keep the math simple and conservative. - CPP: Based on their $66k career average, both receive approximately $1,334/month ($16,008/year).

Methodology: This analysis uses the current 2026 rates for all government benefits and deductions. Because CPP, OAS, and GIS are legislated to be adjusted for inflation (indexed to the Consumer Price Index), their “real” value stays consistent over time. Using today’s figures allows for a clear comparison of the tax logic, as both the benefits and the cost of living are expected to rise proportionally in future.

3. Bob’s Retirement Journey

At age 65, Bob’s “on-paper” income looks modest, consisting only of his government pillars:

- OAS: $8,908 ($742.31/month)

- CPP: $16,008 ($1,334/month)

The “Secret” Benefit: Guaranteed Income Supplement (GIS)

Because Bob chose the TFSA strategy, he gains access to a benefit that many middle-class savers completely miss. The GIS is a tax-free monthly payment for seniors with low taxable income.

Even though Bob has a large TFSA to draw from, the CRA does not count TFSA withdrawals as income. As far as the government is concerned, Bob’s only income is his CPP. Based on 2026 data, Bob’s CPP level entitles him to approximately $5,300 per year in tax-free GIS payments.

Note on Timing: While GIS is usually based on the previous year’s income, Bob can file a “Statement of Estimated Income” (Form ISP-3041) with Service Canada because he has retired. This allows him to receive his $5,300 GIS starting in Year 1, rather than waiting for Year 2.

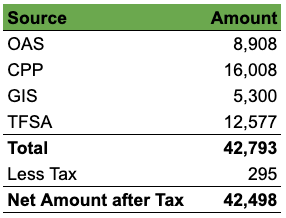

With GIS benefit payments, his total Government benefits total to $30,216 per year. However, GIS payments are tax-free, therefore, he needs to pay tax only on the OAS and CPP payments of $24,916 ($8,908 + $16,008). As per 2026 tax rates for Ontario, the tax payable on this income is only $295, as a 65+ senior, Bob is entitled to the Age Amount credit besides Basic Personal Amount credit.

To meet his retirement requirement of $42,498, Bob needs to withdraw $12,340 from his TFSA. Below is a breakdown of all his income sources, tax and after-tax income.

Growth of Bob’s TFSA during Retirement

At the start of retirement, Bob’s TFSA balance is $995,863. He withdraws roughly $12,577 per year to top up his lifestyle, while the remaining balance continues to grow at an assumed 6% annual real (inflation-adjusted) rate.

Using Dinkytown’s Savings Distribution Calculator, we can project that despite 25 years of consistent withdrawals, Bob’s nest egg doesn’t shrink — it explodes. At age 91, his TFSA is worth approximately $3.5 million.

All of this remaining balance is completely tax-free. If Bob were to pass away after age 91, his estate would receive approximately $3,542,682, with no income tax payable on the TFSA balance.

4. John’s Retirement Journey

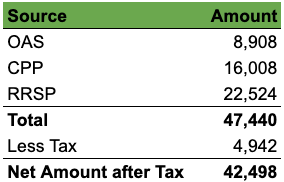

Like Bob, John also retires at age 65, but with $1,359,888 in his RRSP account. His OAS and CPP benefits during retirement are similar to Bob’s, providing total annual government benefits of $24,916.

To maintain an after-tax retirement income of $42,498, John must supplement his government benefits with withdrawals from his RRSP. Unlike TFSA withdrawals, all RRSP withdrawals are fully taxable, so John must withdraw a larger gross amount to account for the additional income tax payable on those withdrawals.

The table below summarizes John’s retirement income, taxes, and resulting after-tax income as per 2026 tax rates for Ontario.

Notice that John pays $4,942 in income tax, which is significantly higher than Bob’s $295. This difference arises because TFSA withdrawals are entirely tax-free, whereas RRSP withdrawals are fully taxable as income. Besides, because of higher income, John is not entitled to receive any GIS.

John continues to withdraw $22,524 per year from his RRSP for six years, until he turns 71. At that point, he is required to convert his RRSP into a Registered Retirement Income Fund (RRIF).

Before moving on to RRIF withdrawals starting at age 72, let us first examine the value of John’s RRSP at the end of these six years. Assuming the account continues to grow at a 6% annual real (inflation-adjusted) rate, Dinkytown’s Savings Distribution Calculator estimates that John’s RRSP balance would increase to $1,762,460 by age 71.

Withdrawals from RRIF

The key difference between an RRSP and a RRIF is that once funds are in a RRIF, you are required to withdraw a minimum amount every year. This minimum is expressed as a percentage of the RRIF’s value at the beginning of the year and increases as you age. The required withdrawal rate is 4% at age 65, 5.28% at age 71, and gradually rises to 20% by age 95.

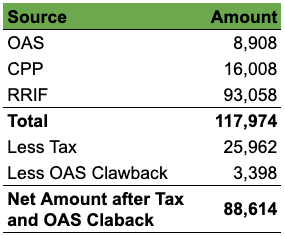

Now in the 7th year of retirement, John must withdraw 5.28% of his RRIF balance of $1,762,460, which works out to $93,058. Whether he actually needs this money or not is irrelevant — he is required to withdraw the minimum amount and pay tax on it. This can have significant tax consequences, including triggering the OAS clawback.

OAS Clawback (Recovery Tax)

As per the Government of Canada:

If your net world income exceeds a threshold amount, you have to repay part or your entire OAS pension. Part or your entire OAS pension is reduced as a monthly recovery tax.

For 2026, the OAS clawback begins when net income exceeds $95,323. The recovery tax is calculated at 15 cents for every dollar of income above this threshold. For example, if your 2026 net income is $100,000, you must repay 15% of the $4,677 above the threshold ($100,000 − $95,323).

John’s Tax Summary in the 7th Year of Retirement

John’s income in the 7th year of retirement is summarized below. In addition to a substantial income tax bill, his higher income results in an OAS clawback of $3,398 on the portion of income above $95,323. Due to his elevated income level, John is also no longer eligible for the Age Amount tax credit.

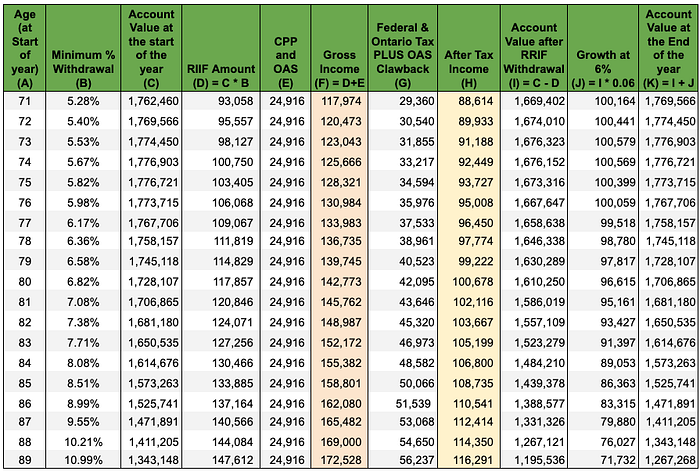

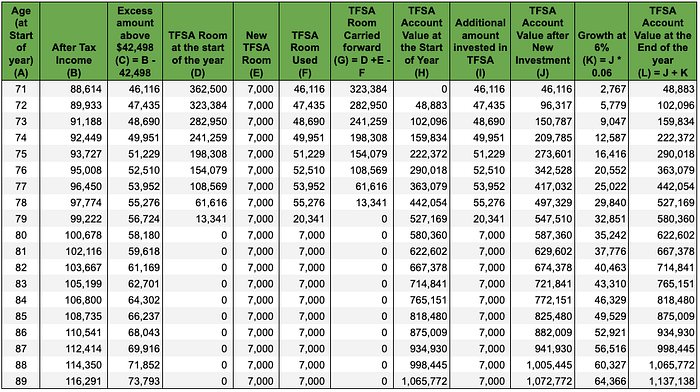

The table below shows the RRIF account value at the start of each year, required RRIF withdrawals, gross income, income taxes and OAS clawbacks, after-tax income, RRIF growth at a 6% annual real (inflation-adjusted) rate, and the year-end RRIF account value from age 72 to age 90.

- Column B shows the minimum RRIF withdrawal percentage for each age (for example, 5.28% at age 71). Note that this percentage increases as John gets older.

- Column C shows the RRIF value at the start of the year.

- Column D shows the required RRIF withdrawal. For the first year, this is $1,762,460 × 5.28% = $93,058.

- Column E shows combined OAS and CPP income during retirement. Since both benefits are inflation-adjusted, this amount remains constant in real terms at $24,916.

- Column F shows total gross income, calculated as the RRIF withdrawal (Column D) plus OAS and CPP income (Column E).

- Column G shows total income tax payable, including the OAS clawback, calculated using the 2026 Ontario tax rules from the TaxTips income tax calculator.

- Column H shows the after-tax income.

- Column I shows the RRIF balance after withdrawals (Column C − Column D).

- Column J shows the annual growth on the remaining RRIF balance at a 6% real rate of return.

- Column K shows the RRIF balance at the end of the year (Column I + Column J), which becomes the starting balance for the following year.

As the mandatory RRIF withdrawal percentages increase with age, John is forced to withdraw progressively larger amounts each year. This leads to higher gross income and, consequently, higher income taxes and OAS clawbacks. Over the retirement period shown, John pays a staggering $834,387 in combined taxes and clawbacks. By contrast, in the earlier retirement phase, John paid only $7,375 in taxes.

During this later phase of retirement, John’s after-tax income significantly exceeds his annual spending needs of $42,498. However, he cannot simply withdraw less from his RRIF — the rules require him to take out a predefined minimum percentage every year, regardless of whether the income is needed.

Based on the OAS clawbacks and higher taxes paid by John, it may appear that Bob has pulled ahead during retirement. However, John’s after-tax income throughout retirement is significantly higher than Bob’s. The key question, then, is what happens if John invests this excess income instead of spending it.

In practice, this is a difficult hurdle. Behavioural economics suggests that when retirees are forced to take larger mandatory withdrawals, they often view the money as “found income” and spend it, a phenomenon known as lifestyle inflation. In contrast, Bob has total control over his TFSA draws.

In the next section, we analyze how allocating the surplus to a TFSA and a non-registered account affects the overall outcome, ensuring a true apples-to-apples comparison by assuming John has the discipline to save every extra cent.

John Invests the Extra Income

As shown in Column H of Figure 2, John’s after-tax income during retirement is significantly higher than his annual spending needs of $42,498. Rather than spending the excess, John chooses to invest it, starting with his TFSA.

Because John has never contributed to a TFSA, he has accumulated substantial contribution room. Assuming the TFSA annual limit has averaged $7,000 per year (inflation-adjusted), his total available TFSA contribution room at retirement is approximately $362,500. The following figure illustrates how John uses this contribution room and how his TFSA grows at a 6% annual real (inflation-adjusted) rate.

Initially, John has ample carried-forward TFSA contribution room, allowing him to invest all surplus income above $42,498 into his TFSA. Around age 79, however, he exhausts most of this accumulated room and can thereafter contribute only the new annual TFSA limit of $7,000.

Despite these limits, John’s TFSA continues to grow tax-free at a 6% inflation-adjusted annual rate. By age 90, the TFSA balance reaches $1,337,138.

During the final 11 years of retirement, John’s excess income exceeds his available TFSA contribution room. He therefore invests the remaining amount in a non-registered account. Because dividends earned in a non-registered account are taxable in the year they are received, this creates a “tax drag” that reduces the effective rate of return.

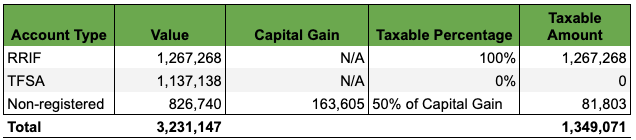

Without delving into the detailed calculations — which are beyond the scope of this article — John’s non-registered account is projected to be worth $826,640 at age 90, with an unrealized (taxable) capital gain of $163,605.

At age 90, John’s account balances are as follows:

If John were to pass away at age 90, the TFSA balance would flow to his estate tax-free. However, the full RRIF balance would be included as income on his final tax return, and 50% of the capital gains in the non-registered account would also become taxable. The large RRIF balance would push John’s marginal tax rate close to 50%.

The following summary shows the final tax return and the net value of the estate after all applicable taxes are paid.

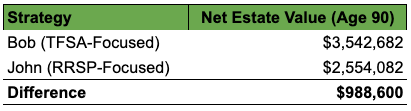

7. Comparing Bob’s and John’s Retirement Journeys

If both Bob and John were to pass away at age 90, their net estate values after paying final taxes would be dramatically different.

The Verdict: Despite starting retirement with a larger balance, John leaves behind nearly $1 million less in net value to his heirs. This isn’t because Bob was a better investor — it’s because Bob was a more tax-efficient “spender.”

8. Final Takeaway: Breaking the “Tax Deferral” Mindset

The reason for this $1M gap is the Double Whammy of the Canadian retirement system:

- The Benefit Loss: John’s RRIF withdrawals are “forced income.” This disqualified him from $5,300/year in tax-free GIS, while Bob’s TFSA withdrawals were “invisible” to the government, letting him collect the bonus every year.

- The Tax Time Bomb: John spent decades deferring taxes only to pay them all at once at his highest lifetime tax bracket upon death.

The Core Lesson: RRSPs aren’t “bad,” but they are often misused by the middle class. The real risk isn’t failing to save — it’s deferring taxes without an exit strategy.

Ask yourself before your next contribution:

- The Bracket Trap: Will my mandatory RRIF withdrawals push me into a higher tax bracket than I’m in now?

- The Clawback Hit: Will my retirement income trigger a loss of OAS or GIS benefits?

- The Estate Bill: Am I building a nest egg for my family, or a massive payday for the CRA?

What’s Next? The math changes as your income rises. In the next parts of this series, I break down the “Trap” under different scenarios:

- Part 3: The 5% Stress Test — Does the trap disappear if the market underperforms?

- The $80,000 Analysis: How the TFSA-first strategy builds a $573,000 larger legacy than the RRSP.

- The $120,000 Earner Analysis (Coming Soon)

Stay tuned!

Disclaimer: This article is for educational purposes only and is not financial or tax advice. Please consult a qualified tax or financial professional before making any decisions.

What are your thoughts on this post? Share your comments with us.

Stay ahead of the curve. Subscribe here to get notified whenever I publish a new guide or tool.

Share your comment or feedback. We'll get back to you as soon as we can.