The RRSP Trap: Why Middle-Class Canadians Should Be Careful (Part 1)

How the “default” advice of tax deferral can lead to a million-dollar mistake — and how to spot the trap before it’s too late.

For decades, the RRSP has been marketed as the gold standard for retirement savings. But for the average middle-class Canadian, this “tax-deferred” dream can quietly transform into a retirement nightmare.

Through a 35-year data simulation of two identical earners, this article reveals a shocking truth: by choosing a TFSA-first strategy over an RRSP, a typical worker could leave behind an estate about $1 million larger — without changing their lifestyle or saving an extra penny.

This isn’t just about how much you save; it’s about the account you choose and the timing of the tax bill. The real danger isn’t paying the CRA today; it’s giving them a massive, mandatory cut of every dollar you withdraw later while simultaneously disqualifying yourself from thousands in government benefits.

This isn’t a controversial statement — it’s basic math, and I want to walk you through it in plain English.

Inside the “RRSP Trap” Series:

- Part 1: The 35-year simulation of John (RRSP) vs. Bob (TFSA).

- Part 2: The $1 million Reality Check — The impact of withdrawals and clawbacks.

- Part 3: The Stress Test — Does the “Trap” disappear if the market slows down?

1. What is the middle class in Canada?

There is no single official definition of “middle class” in Canada. One practical way to think about it is to look at median individual incomes by age, which reflect what a typical person earns.

According to Statistics Canada’s Canadian Income Survey, 2023 (Income of individuals by age group):

- The median total income (before tax) for individuals aged 25–34 was $49,500.

- The median total income (before tax) for individuals aged 35–44 was $60,900.

Assuming a modest real income growth of about 2% per year, these medians would translate to roughly $51,500 (ages 25–34) and $63,000–$64,500 (ages 35–44) in 2025.

For retirement planning and savings projections, it is reasonable to use an annual income of about $66,000 as a representative benchmark for a typical working-age, middle-class Canadian.

2. Retirement Savings Options for a $66,000 Annual Income

John and Bob are residents of Ontario. They completed their studies at age 24 and started working in entry-level jobs. Over the next six years, they focused on paying off their student loans and, as a result, did not contribute to any registered savings accounts such as an RRSP, TFSA, or FHSA.

At age 30, in January 2026, both John and Bob secured jobs paying $66,000 per year. To keep the analysis simple and focused, the following assumptions apply:

- Their salaries and marginal tax brackets remain unchanged in real (inflation-adjusted) terms throughout their working careers.

- They do not have a defined benefit pension plan, which is increasingly rare today.

- Their employers do not offer RRSP matching contributions.

- Since the TFSA limit is indexed to inflation, we assume it stays at $7,000 in real terms for the purpose of this analysis.

- They work for 35 years and retire at age 65.

- They remain in good health and live to age 90. During ages 66 to 90, they rely on personal savings and government benefits, with any remaining balance passed on to their children or other beneficiaries upon death.

With these assumptions in place, we can now compare how John and Bob might build their retirement savings using two of Canada’s most popular registered accounts: the Registered Retirement Savings Plan (RRSP) and the Tax-Free Savings Account (TFSA).

Although both accounts offer powerful tax advantages, they work very differently. An RRSP provides an upfront tax deduction, but withdrawals are fully taxable in retirement. A TFSA, on the other hand, offers no deduction today, but allows investments to grow and be withdrawn completely tax-free.

To isolate the impact of these differences, the comparison assumes that John and Bob save the same amount of pre-tax income each year, invest in identical portfolios, and earn the same long-term rate of return. The only variable is where the savings are held — RRSP versus TFSA — and how they are taxed over time.

3. John — the RRSP Saver

John chooses to save for retirement using an RRSP. With an annual income of $66,000, his RRSP contribution room is 18% of income, or $11,880.

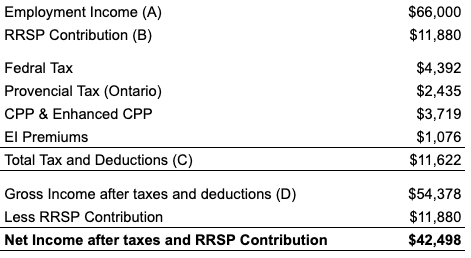

Let’s first look at John’s 2026 income tax return, assuming he contributes the full $11,880 to his RRSP. Using the TaxTips calculator for 2026, the results are summarized below.

As apparent from the results, for a $66,000 annual income, John, who is a resident of Ontario, needs to pay $11,622 tax (including CPP and EI premiums) and will have an after-tax income of $54,378. However, as he has invested $11,880 in an RRSP account, he will have $42,498 in his hand to spend. It is also worth noting that by making an $11,800 RRSP contribution, John reduces his income taxes by approximately $3,179, reflecting the immediate tax benefit of the RRSP deduction.

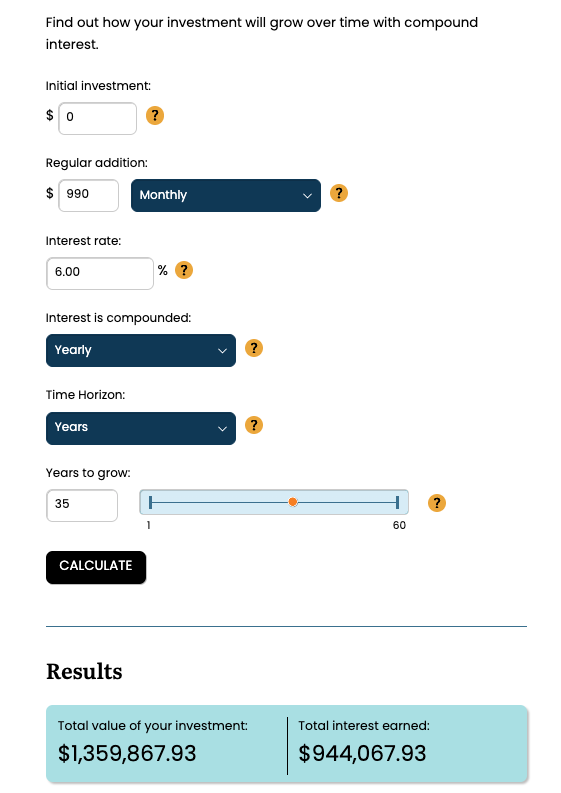

John invests $990 per month, or $11,880 per year, into his RRSP. Assuming a 6% annual real (inflation-adjusted) return, we can estimate the long-term value of his savings. Using the Ontario Securities Commission’s Compound Interest Calculator, John’s RRSP balance grows to approximately $1,359,888 by the time he retires at age 65.

By the end of the year in which John turns 65, his RRSP account would be worth $1,359,868 in today’s dollars, since the assumed 6% rate of return is already adjusted for inflation.

4. Bob — the TFSA Saver

Next, let us turn our attention to Bob. Bob opts for a different path: he ignores the RRSP and focuses entirely on his Tax-Free Savings Account (TFSA).

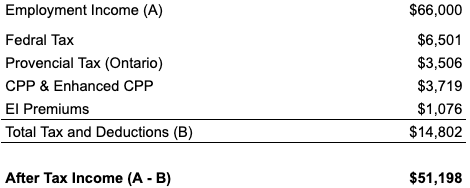

Because TFSA contributions are made with after-tax dollars, Bob must pay the full tax on his $66,000 income first. After paying income tax and CPP/EI premiums, Bob’s take-home pay is $51,198.

To match John’s lifestyle exactly, Bob invests $8,700 into his TFSA, leaving him with $42,498 in his pocket — to the penny, the same spending power as John.

Bob has plenty of room for this strategy. Having turned 18 in 2014, he has accumulated significant “carry-forward” room. With approximately $76,500 in unused space plus the new 2026 limit, he can comfortably contribute $8,700 per year for his entire 35-year career.

Assuming that Bob contributes $725 per month ($8,700 per year) to his TFSA for 35 years, earning a 6% annual real (inflation-adjusted) return, as per the Ontario Securities Commission’s Compound Interest Calculator, Bob’s TFSA balance would grow to approximately $995,863 by the end of the year in which he turns 65.

This amount is expressed in today’s dollars, since the assumed 6% rate of return is already adjusted for inflation.

5. The Verdict (On Paper)

After 35 years, the scoreboard looks like this:

- John (RRSP): $1,359,868

- Bob (TFSA): $995,863

John appears to be the undisputed winner. He followed the traditional advice, maximized his deductions, and built a “mountain of gold” that is $364,005 larger than Bob’s.

But in the Canadian retirement system, a larger account doesn’t always mean a better life. In Part 2, we follow them through their entire retirement journey to see what happens when they actually start spending that money. We’ll reveal the “Secret Benefit” the government offers to seniors that John’s RRSP completely blocks — and how Bob’s “smaller” account actually buys him a more expensive lifestyle for decades to come.

Are you ready to see why a $1.3 million RRSP might actually be a trap?

Click here for Part 2: The Withdrawal Phase & The $1M Reality Check

Disclaimer: This article is for educational purposes only and is not financial or tax advice. Please consult a qualified tax or financial professional before making any decisions.

What are your thoughts on this post? Share your comments with us.

Stay ahead of the curve. Subscribe here to get notified whenever I publish a new guide or tool.

Share your comment or feedback. We'll get back to you as soon as we can.