FHSA Explained in Plain English

A simple guide to how the FHSA works, who can use it, and why it’s the most powerful way to save for your first home

Homeownership in Canada has been gradually declining, from 69% in 2011 to 66.5% in 2021, and is estimated to be around 65.8% in 2025. This means roughly one in three Canadians still struggle to buy their first home. Owning a home is a big dream for many, but saving for a down payment can be confusing, stressful, and slow. When I bought my first home in 1999, I used the Home Buyers’ Plan (HBP) to withdraw money from my RRSP (Registered Retirement Savings Plan) for the downpayment for the home; however, I had to repay the withdrawn amount to my RRSP over time. After the introduction of the TFSA (Tax-Free Savings Account) in 2009, many people began using it to save for a home down payment, since there is no requirement to repay money withdrawn from a TFSA.

Launched in 2023, the First Home Savings Account (FHSA) is arguably the most exciting savings tool for first-time homeowners in a generation. It’s a true game-changer because it combines the best features of both the RRSP and TFSA, offering tax advantages both when you save and when you withdraw. The FHSA makes it easier for first-time buyers to save smarter and reach their goal faster.

What is an FHSA?

A First Home Savings Account (FHSA) is a special account designed to help first-time home buyers save for a down payment on a qualifying home tax-free.

Who is Eligible to Open an FHSA?

To open a First Home Savings Account (FHSA), you must meet all three of the following conditions at the time you open the account:

- Age: You must be at least 18 years old (or the age of majority in your province, if higher) and no older than 71 by December 31st of the year you open the account.

- Residency: You must be a resident of Canada.

- First-Time Home Buyer Status: At the time you open the account, you must meet the FHSA definition of a first-time home buyer.

The Two-Part First-Time Home Buyer Test (for Account Opening)

You are considered a first-time home buyer if you meet both of the following conditions:

- You did not live in a home as your principal residence that you owned or jointly owned at any time in the current calendar year before the account is opened or at any time in the previous four calendar years.

- You did not live in a home as your principal residence that your spouse or common-law partner owned or jointly owned during that same period (the current year before opening and the previous four calendar years), OR you do not have a spouse or common-law partner at the time you open the account.

In plain English:

You must look back five years (the current year plus the last four). If either you or your spouse/common-law partner lived in a house you or your spouse owned during that time, you generally cannot open an FHSA.

You can open an FHSA at most Canadian financial institutions. It combines the best features of both the RRSP and TFSA: your contributions are tax-deductible (like an RRSP), and any qualifying withdrawals for a first home are tax-free (like a TFSA).

FHSA Contribution Limits: The Key Numbers

The contribution rules for the FHSA are unique — they share features with both the RRSP and TFSA, but also have their own critical differences.

The Two Critical Rules to Know

- Room Starts When You Open It: Your FHSA contribution room does not automatically accumulate when you turn 18 (like a TFSA). Instead, your initial $8,000 of room is only created in the year you open your first FHSA. This makes opening the account early a priority, even if you can’t contribute right away.

- The $8,000 Carry-Forward Cap: If you don’t contribute the full $8,000 in a year, the unused amount is carried forward to the next year, but there is a strict limit. You can only carry forward a maximum of $8,000 of unused room.

Example: Maximizing the Carry-Forward

This unique rule means your absolute maximum contribution in any single year can be $16,000 ($8,000 current year limit plus $8,000 carry-forward).

Unlike an RRSP, your FHSA contribution room is not linked to your income — it’s the same fixed $8,000 for everyone, just like a TFSA.

⚠️ Over-Contribution Penalty

Just like with the RRSP and TFSA, exceeding your FHSA contribution limit can result in penalties from the Canada Revenue Agency (CRA).

The Rule: If you contribute more than your available FHSA contribution room (which, as discussed, is a maximum of $16,000 in any given year), the CRA applies a 1% tax penalty per month on the highest excess amount until it is removed.

In plain English, this means:

- The Penalty is Monthly: The cost adds up fast and continues until the excess amount is removed.

- Action is Required: You must immediately withdraw the over-contributed amount to stop the 1% monthly penalty from accruing.

Pro Tip: Always check your FHSA contribution room on the CRA My Account before making a large contribution to ensure you stay within your limit. Crucially, since you are allowed to have multiple FHSA accounts, be extra careful that the combined contributions across all accounts do not exceed your total limit.

The Double Tax Advantage: Contributions and Growth

The First Home Savings Account (FHSA) is the only registered plan in Canada that offers a double tax benefit when used for a first home purchase. It operates by combining the best features of an RRSP and a TFSA.

1. Tax Deduction on Contributions (Like an RRSP)

When you contribute money to your FHSA, you can claim that amount as a deduction on your annual income tax return.

- How it works: This deduction lowers your total taxable income, potentially moving you into a lower tax bracket and resulting in a larger tax refund for the year you contributed.

- Flexibility: Just like with an RRSP, you are not required to claim the deduction in the year you contribute. You can carry the deduction forward indefinitely and use it in a future year when you expect to be in a higher income tax bracket, maximizing your tax savings.

Pro Tip: Unlike an RRSP, contributions made in the first 60 days of the calendar year cannot be deducted on your tax return for the previous year. FHSA contributions can only be deducted in the year they are made or in a future year.

2. Tax-Free Growth and Withdrawal (Like a TFSA)

Money held in your FHSA grows tax-free, so you don’t pay tax on any interest, dividends, or capital gains while it remains in the account.

More importantly, when you withdraw funds to buy your first home, the entire amount, including both your original contributions and all investment growth, is completely tax-free and not included in your taxable income.

This is the FHSA’s biggest advantage: you get a tax deduction when you contribute (saving tax today) and a tax-free withdrawal when you buy your home (saving tax in the future).

Withdrawing Your Money: The Rules

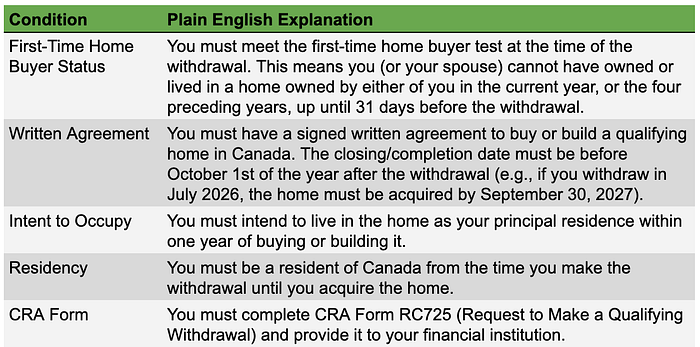

The FHSA is unique because, unlike an RRSP, you don’t have to repay the money you take out for a home purchase. However, to keep the withdrawal completely tax-free (the ultimate benefit), you must follow a strict set of rules.

Qualifying Withdrawals (Tax-Free)

A withdrawal is considered a qualifying withdrawal when it is used to buy or build your first home. If you meet all the required conditions, the entire amount withdrawn, including any investment growth, is tax-free.

Key Difference from the RRSP Home Buyers’ Plan: Unlike the Home Buyers’ Plan (HBP), money withdrawn from an FHSA does not need to be repaid.

What happens if I have already bought a home without withdrawing from the FHSA?

Don’t panic if you’ve already signed the papers and moved in! You have a 30-day grace period from the date you acquire the home to make your tax-free qualifying withdrawal from the FHSA. If you wait until day 31, you lose the ‘first-time homebuyer’ status for that account, and any withdrawal would then be taxable.

What Happens After the First Qualifying Withdrawal?

A countdown begins! Once you make your first qualifying withdrawal, you have until October 1st of the following calendar year to:

- Acquire the home: You must officially take possession/ownership of the property by this date.

- Make additional withdrawals: Any further tax-free withdrawals for that same home must also be completed by this October 1st deadline (or within 30 days of acquiring the home, whichever comes first).

Finally, you have until December 31st of that same following calendar year to:

- Close the FHSA account entirely: Any remaining funds must be transferred to an RRSP/RRIF (tax-free) or withdrawn as taxable income.

Non-Qualifying Withdrawals (Taxable Immediately)

If you take money out of your FHSA and the withdrawal is not made for the purpose of acquiring a first home (e.g., you use the funds to pay off debt, buy a car or invest in a taxable account), it is considered a non-qualifying withdrawal.

- Tax Impact: The full amount withdrawn is added to your taxable income for the year, just like an RRSP withdrawal.

- Withholding Tax: Your financial institution is required to deduct and remit a withholding tax to the government as a prepayment toward your tax bill.

What If I Don’t Buy the Home After Withdrawing?

If you make a qualifying withdrawal but ultimately do not acquire a qualifying home by the final deadline (October 1st of the year following the withdrawal), the CRA will automatically reclassify that withdrawal from a qualifying withdrawal (tax-free) to a taxable withdrawal.

- The Tax Consequence (The Clawback): The entire amount you withdrew (both your contributions and the investment growth) will be added to your taxable income for the year the deadline passed. For example, you make a qualifying withdrawal in 2026. You have until October 1, 2027, to buy the home. If you miss this deadline, the entire withdrawal amount is added to your income for the 2027 tax year.

Crucial Action Step: The Fail-Safe Option:

If you make a qualifying withdrawal and realize you will not meet the deadline, there is no way to put the funds back into the FHSA. However, you can prevent the withdrawal from being immediately taxed by transferring the funds to your RRSP:

- Transfer to RRSP: You can transfer the withdrawn funds (or any remaining funds in the FHSA) directly to your RRSP or RRIF on a tax-free basis. This transfer does not use up your available RRSP contribution room.

- Deadline: This tax-free transfer must happen before your maximum participation period ends (which is December 31st of the year following your first qualifying withdrawal).

In plain English: If the home purchase falls through, immediately transfer the funds into your RRSP to keep them tax-sheltered and avoid paying a hefty tax bill that year.

⚠️ IMPORTANT: FHSA vs. TFSA Withdrawal Rule

Please be aware of a critical distinction from the Tax-Free Savings Account (TFSA): The FHSA contribution room is lost permanently when you withdraw funds.

Unlike a TFSA, where any amount withdrawn is added back to your contribution room in the following year, FHSA withdrawals do not restore contribution room. Whether the withdrawal is a tax-free qualifying withdrawal or a taxable non-qualifying withdrawal, the amount withdrawn is permanently removed from your FHSA.

Even after making withdrawals, your lifetime FHSA contribution limit remains capped at $40,000 and cannot be replenished.

In plain English: Once you take money out of an FHSA, you can’t put it back.

The Final Deadline: When the Account Must Close

Regardless of your home-buying success, every FHSA has a hard-stop date called the Maximum Participation Period. The entire FHSA must be closed by December 31st of the year in which the earliest of the following three events occurs:

- You Buy a Home: The year following your first qualifying home withdrawal.

- The 15-Year Limit: The 15th anniversary of opening your first FHSA.

- Age Limit: The year you turn 71 years old.

What Happens to Unused Funds if the Deadline is Met?

If the 15-year or Age 71 deadline arrives and you haven’t bought a home, the FHSA is designed with a great fail-safe: You can roll the funds into your retirement savings. You have two options for the money remaining in the FHSA

- Tax-Free Transfer: You can transfer the entire amount (contributions + growth) directly to your RRSP or RRIF without affecting your existing RRSP contribution room. This is the recommended option to keep the funds tax-sheltered.

- Taxable Withdrawal: You can withdraw the funds as cash, but the entire amount will be fully added to your taxable income for that year.

Final Takeaway: Is an FHSA Worth It?

For Canadians planning to buy their first home, the FHSA is one of the most powerful savings tools ever introduced. It uniquely combines an upfront tax deduction (like an RRSP) with a tax-free withdrawal for a home purchase (like a TFSA) — a combination no other account offers.

Used correctly, an FHSA can:

- Help you build a down payment faster

- Reduce your taxes today

- Eliminate taxes when you buy your first home

Even if your homeownership plans change, the FHSA still works in your favour. Any unused balance can be transferred to your RRSP or RRIF on a tax-free basis, effectively turning the FHSA into an additional retirement savings vehicle.

One final, powerful note on “stacking” savings: If both partners are eligible, you and your spouse or common-law partner can each use your full FHSA (contributions plus growth), in addition to withdrawing up to $60,000 each from your respective RRSP Home Buyers’ Plans (HBP). Together, this allows a couple to access a significantly larger pool of tax-advantaged funds for a down payment than ever before.

In short: If you qualify and expect to buy a home within the next 15 years, opening an FHSA early — even with small contributions — can be one of the smartest financial moves you make.

What are your thoughts on this post? Share your comments with us.

Stay ahead of the curve. Subscribe here to get notified whenever I publish a new guide or tool.

Share your comment or feedback. We'll get back to you as soon as we can.