RRIF Explained in Plain English

Master the RRIF rules, control your cash flow, and protect your legacy.

RRSPs were introduced in Canada in 1957 to encourage Canadians to save for retirement by offering specific tax advantages. Most Canadians have a fairly good understanding of RRSPs, namely that:

- Contributions are tax-deductible, lowering taxable income.

- Investments within the RRSP grow tax-deferred until the funds are withdrawn, usually in retirement.

However, you may not know that while you may live into your 80s, 90s, or even beyond, an RRSP must be closed by December 31 of the year you turn 71. At this point, you have three options:

- Convert your RRSP into RRIF

- Convert your RRSP into an annuity

- Withdraw the funds as cash (almost never recommended)

The RRIF: Your RRSP’s Second Act

Most Canadians choose the first option: the Registered Retirement Income Fund (RRIF).

Think of it as two phases of the same financial journey: the RRSP is your Savings Phase, where the goal is to save and grow as much wealth as possible while you are working. The RRIF is your Income (or Pension) Phase, where you use the accumulated wealth to generate a flexible self-made pension during the retirement phase. While you can technically open a RRIF at any age, this phase usually begins when you retire.

While additional rules apply to RRIFs, investments held inside a RRIF continue to grow tax-deferred, just like an RRSP.

Converting RRSP to RRIF

Converting your RRSP account to a RRIF is usually a very smooth process. All you need to do is open a RRIF account and transfer your assets from the RRSP “in-kind.” This means you don’t have to sell your stocks, ETFs, or GICs — your investments simply move from one account to the other. Most financial institutions will handle this for free within a few business days.

While you must convert your entire RRSP by age 71, you don’t have to wait until then, and you don’t have to do it all at once. You can convert your RRSP in stages, rather than all at once. For example, if you have $600,000 in your RRSP, you could convert $100,000 into a RRIF now and leave the remaining $500,000 in your RRSP to continue as a savings plan.

Why do a partial conversion?

This strategy can be effective if you retire early or turn 65 and are still working. It allows you to “unlock” just enough income to take advantage of specific tax breaks, like the Pension Income Amount, without being forced to withdraw more than you actually need. We will dive deeper into how this $2,000 tax-free trick works later in this article.

The One-Way Street: No New Contributions

It’s important to remember that a RRIF isn’t just a renamed RRSP — it operates under a different set of rules. The biggest one? You cannot make new contributions to a RRIF.

Unlike an RRSP, where you might have been depositing money for decades, a RRIF only accepts “transfers” from other registered accounts (like your RRSP or another RRIF). Once you have converted to a RRIF, you can no longer use it to lower your taxable income with new deposits.

Roadmap Tip: If you believe you may still need to make RRSP contributions to lower your taxes, you don’t have to convert everything at once. You can convert just a portion of your RRSP into a RRIF and keep the rest in your RRSP to remain “contribution-ready” until December 31 of the year you turn 71.

Roadmap Tip: Once you pass age 71, you can no longer hold an RRSP in your own name or make contributions to it. However, if you still have unused contribution room and a spouse who is age 71 or younger, you can contribute to a Spousal RRSP. This allows you to continue receiving tax deductions against your income even though you are past the age limit for your own plan.

The Mandatory Minimum Withdrawal

Now that the account is set up and the “intake” valve is closed, let’s talk about the “out-take” valve. While an RRSP lets you decide when to take money out, a RRIF comes with a mandatory minimum withdrawal schedule.

Why the Minimum Withdrawal

The government allowed this money to grow tax-deferred for years and now wants to ensure that the tax is eventually collected. To accomplish this, mandatory minimum withdrawals apply each year, based on your RRIF’s value on January 1 and your age (or your spouse’s age, if elected). As these withdrawals increase with age, they can push taxable income higher — potentially reducing or eliminating eligibility for income-tested benefits such as the Guaranteed Income Supplement (GIS) and triggering Old Age Security (OAS) clawbacks.

- The Grace Period: You are not required to make a withdrawal in the calendar year you open a RRIF. Your first mandatory withdrawal starts the following year.

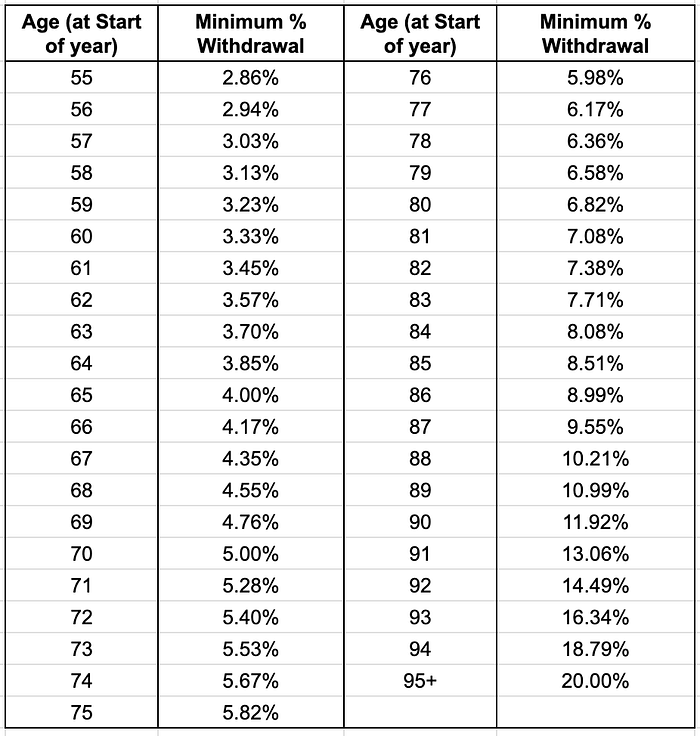

- The 2026 Percentages: The older you get, the higher the percentage becomes. The table below shows selected minimum RRIF withdrawal rates for 2026:

Roadmap Tip: The Spousal Age Election

When you first set up your RRIF, you can choose to base your minimum withdrawals on your spouse’s age instead of your own. If your spouse is younger, this results in a lower mandatory withdrawal, allowing more of your money to remain in the tax-sheltered “bucket” for a longer period.Important: This election must be made before your first RRIF withdrawal, and once chosen, it cannot be changed.

You must elect to use your spouse’s age at the time you establish the RRIF. Once the first minimum withdrawal is processed, this decision is permanent and cannot be changed.

How RRIF Withdrawals Are Taxed

It’s important to remember: every dollar you withdraw from a RRIF is taxable income. Much like employment income during your working years, the CRA treats your RRIF withdrawals as income that must be reported on your tax return.

However, there is a crucial distinction between withdrawing the Minimum Amount and taking out Additional Funds.

1. The Minimum Amount: No “Upfront” Tax

When you withdraw only the mandatory minimum amount, your financial institution is not required to withhold tax at source. You receive the full amount directly.

- The catch: This money is still fully taxable. You simply settle the tax owing when you file your income tax return the following spring.

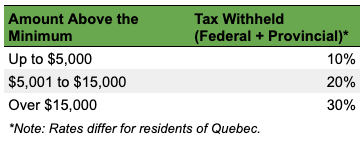

2. Withdrawals Above the Minimum: Withholding Tax Applies

If you choose to withdraw more than the minimum amount — perhaps to fund a large purchase or a special trip — the rules change. Your financial institution must withhold tax at source on the excess portion and remit it to the CRA on your behalf. Think of this as a prepayment toward your final tax bill. For most of Canada, the withholding rates are:

Roadmap Tip: Don’t be misled — just because the bank withholds 10% does not mean that’s your final tax bill. If your total income puts you in a 30% marginal tax bracket, you’ll owe the remaining 20% when you file your return.

Why Consider Converting Your RRSP Early?

While you are only forced to close your RRSP at age 71, many Canadians find it beneficial to start this process strategically earlier. Converting even a portion of your RRSP to a RRIF in your 60s can be a brilliant tax move for two main reasons.

The “Age 65” Sweet Spot: The Pension Income Credit

As promised earlier, here’s the tax opportunity available once you turn 65.

Starting at age 65, the first $2,000 of eligible RRIF withdrawals each year may qualify for the Federal Pension Income Amount. This is a non-refundable tax credit that can make that $2,000 nearly tax-free at the federal level.

The strategy: Even if you don’t need the cash yet, once you’re 65 or older, it often makes sense to convert a small portion of your RRSP to a RRIF, withdraw $2,000, and claim this credit. It’s essentially a “use-it-or-lose-it” tax break offered by the government.

2. No Withholding Tax on Minimums

This is a hidden advantage of the RRIF. When you withdraw money from an RRSP, the financial institution must take withholding tax (10% to 30%) immediately. However, with a RRIF, there is no withholding tax on the minimum withdrawal.

The Benefit: You get 100% of your money upfront. While you still owe the tax at the end of the year, you have the use of that money in the meantime, allowing it to stay invested or sit in a high-interest account for a few extra months.

Consider an example:

John is 65 years old and has retired with $500,000 in his RRSP. He is following the traditional advice to wait until age 71 to convert his RRSP to a RRIF. He receives $18,000 in OAS and CPP but needs an additional $21,000 each year to support his lifestyle.

- The RRSP Scenario: To get $21,000 “in hand,” John must ask for a $30,000 withdrawal. Because it’s an RRSP, the bank automatically withholds 30% ($9,000). John gets his $21,000, but he has “pre-paid” $9,000 to the CRA. Based on the approximate 2026 Ontario tax rates, his actual tax bill on a $48,000 income ($18k + $30k) would only be roughly $5,064. John has overpaid by nearly $4,000 and has to wait until next spring to get that refund back from the government.

- The RRIF Scenario: If John converts to a RRIF, he can take his 4% minimum withdrawal ($20,000) with zero tax withheld at the source. He gets the full $20,000 immediately. Furthermore, by using a RRIF, he can claim the Pension Income Credit, which can reduce his total tax bill even further to $2,940. He keeps his cash flow high and keeps his money working for him longer.

3. The “RRSP Meltdown” Strategy

The “Meltdown” strategy is about smoothing out your taxes. If you wait until age 71 and have a very large RRSP, the mandatory minimums might push you into a much higher tax bracket, potentially triggering “clawbacks” on your Old Age Security (OAS).

By converting early, you can start chipping away at that large balance sooner. This “melts down” the total amount in your account so that when you hit 71, your mandatory payments are smaller and more manageable.

Roadmap Tip: Think of an early conversion as “tax-bracket management.” It’s often better to pay a little bit of tax at a low rate now than to be forced to pay a lot of tax at a high rate later.

To learn more about the RRSP Meltdown strategy, see the article: RRSP Meltdown Explained: A Plain English Guide for Canadian Retirees

4. Pension Income Splitting (The “Family Tax Saver”)

Perhaps the most powerful advantage for couples is the ability to “split” your income for tax purposes. If you have a higher income than your spouse, you can notionally allocate up to 50% of your RRIF income to them.

- The Age 65 Rule: While income from a workplace pension can be split at any age, income from a RRIF can only be split once the person making the withdrawal turns 65.

- RRSP vs. RRIF: Withdrawals made directly from an RRSP are not eligible for pension splitting, regardless of your age. You must convert the funds to a RRIF to take advantage of this.

- The Result: By shifting income from a high-tax-bracket spouse to a lower-bracket spouse, you can significantly reduce the total tax your household pays.

For a deeper dive into how this works and why it’s a game-changer for couples, see my full guide: Pension Income Splitting

The Final Roadmap Stop: What Happens at the End?

No one likes to think about it, but a key part of the RRIF strategy is deciding what happens to the money when you pass away. If you don’t set this up correctly, the CRA could become your biggest heir, taking up to 50% of the account’s value in taxes on your final return.

For those with a spouse or common-law partner, you have two main choices on your RRIF application: Beneficiary or Successor Annuitant.

1. Naming a Beneficiary

If you name your spouse as a Beneficiary, the RRIF is essentially “collapsed” when you pass away. The money can be rolled over to your spouse’s RRSP or RRIF tax-free, but it involves a fair amount of paperwork.

2. Naming a Successor Annuitant (The Smoother Path)

If you name your spouse as the Successor Annuitant, they simply “step into your shoes.” The RRIF contract continues uninterrupted; your spouse becomes the new owner, and the investments aren’t sold; your spouse becomes the new owner of the account.

The Benefit: Because your spouse becomes the new owner, the tax shelter remains perfectly intact with zero interruption.

- Withdrawals: Your spouse takes over the responsibility for the mandatory minimum withdrawals. If you hadn’t finished taking your minimum for the year you passed away, your spouse withdraws the rest.

- Flexibility: Your spouse keeps the same investments (stocks, GICs, ETFs) and can choose to change the withdrawal amounts or frequency they like.

- Simplicity: It is, by far, the easiest way to protect a surviving spouse from a massive tax bill and a mountain of paperwork during a difficult time.

Roadmap Tip: If you want your RRIF to go to your children or a charity instead of a spouse, you must name them as Beneficiaries. Just keep in mind that unless the beneficiary is a financially dependent child, the full value of the RRIF will likely be taxed as income on your final tax return.

Conclusion: Turning the Tap On

Moving from an RRSP to a RRIF is a major milestone. It marks the moment your hard-earned savings start working for you. By understanding the minimums, taking advantage of age-65 tax credits, and setting up your successors correctly, you ensure that your “Income Phase” is as smooth and tax-efficient as possible.

Happy retirement — you’ve earned it!

Disclaimer: This article is for educational purposes only and is not financial or tax advice. Tax rules can change and vary by province — especially in Quebec. Please consult a qualified tax or financial professional before making any decisions.

What are your thoughts on this post? Share your comments with us.

Stay ahead of the curve. Subscribe here to get notified whenever I publish a new guide or tool.

Share your comment or feedback. We'll get back to you as soon as we can.