Pension Income Splitting

Your Simple Guide to Lower Taxes in Retirement

Part 3 of our Income Splitting Series. See also: “Income Splitting for Canadians” and “Spousal RRSP for Income Splitting”.

Retirement in Canada comes with a whole new vocabulary: OAS, CPP, RRIFs, LIFs, and it can feel overwhelming. However, there is one strategy every retired couple should understand, as it is essentially a “free lunch” from the tax department: Pension Income Splitting.

If you or your spouse has a private pension or retirement savings, this simple strategy could save your household thousands of dollars in taxes every year. The best part? You don’t need to be a math whiz to understand it.

Here is the plain-English guide to how it works.

1. What is Pension Income Splitting?

Canada uses a graduated tax system, meaning the more money you make, the higher the percentage of tax you pay on that marginal income. When one spouse has a significantly higher income than the other, the household pays more tax overall.

Pension income splitting allows the higher-income spouse (the transferor) to allocate up to 50% of their eligible pension income to the lower-income spouse (the recipient) for tax purposes only.

No money actually changes hands — you simply tell the CRA to treat part of your pension income as if your spouse earned it. This moves income from a higher tax bracket into a lower one and reduces your total family income tax.

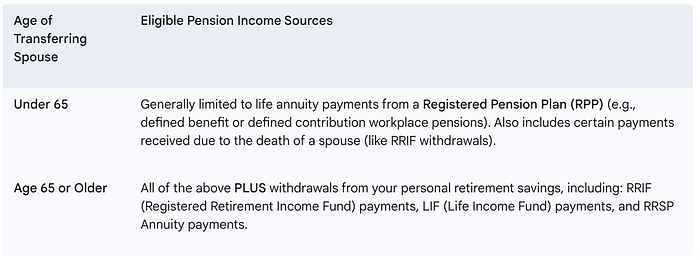

2. Who is Eligible? (The Importance of Age 65)

You can generally use this strategy if you meet these three criteria:

- Relationship: You are married or in a common-law partnership and were living together at the end of the tax year (minor exceptions for medical/educational separation apply).

- Residency: You are a resident of Canada.

- Income: You received eligible pension income.

Importantly, what counts as “eligible” pension income depends on the age of the spouse who is transferring the income, not the spouse receiving it.

What is not eligible: Government benefits are not considered “eligible pension income” for this type of tax split. This includes Old Age Security (OAS) and the Canada Pension Plan (CPP).

CPP cannot be split using the tax-based method. However, CPP retirement benefits can be shared through Service Canada’s Pension Sharing program, which is entirely separate. This process divides only the CPP earned during the years you lived together, and it changes the actual monthly payments, not just your tax return.

3. How Do You Claim the Split?

Pension splitting is handled when you file your annual income tax return.

- The Form: You must use the Canada Revenue Agency (CRA) form T1032 — Joint Election to Split Pension Income.

- The Process: Most modern tax software (like TurboTax or Wealthsimple Tax) will prompt you to optimize your return and handle the math automatically. Most tax software will automatically calculate the optimal split (up to 50%) to maximize tax savings and will generate Form T1032 for you.

- The Filing: Both spouses must complete, sign, and file the T1032 form with their respective tax returns. You must file a new election every year you choose to split income.

4. The Benefits: Why This Strategy Pays Off

The primary benefit of pension income splitting is lowering your household’s overall tax bill. This happens through three major advantages:

A) Instant Tax Savings Through Bracket Balancing

When you shift eligible pension income from the higher-income spouse to the lower-income spouse, more of your combined income is taxed at lower marginal rates. For couples with a significant income gap, this can generate thousands of dollars in annual tax savings.

The tax savings are created because the combined household income becomes more evenly balanced, so less income is taxed at the highest marginal rates.

Let us look at an example.

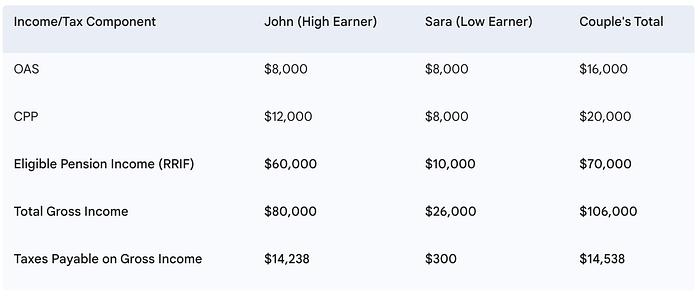

John and Sara, both age 65, live in Ontario, are retired, and receive CPP, OAS, and RRIF withdrawals. John earned more during his working career and therefore has a much larger RRIF. (Taxes shown are based on illustrative 2025 Ontario rates, including applicable credits.)

Baseline Scenario: Without Pension Income Splitting

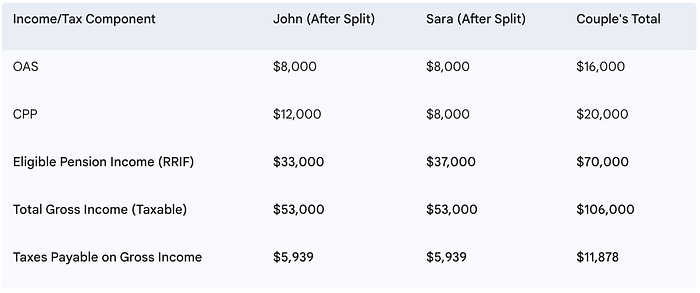

John can elect to split up to 50% of his eligible pension income — in this case, $30,000 (50% of his $60,000 RRIF income).

The scenario below illustrates the impact of splitting $27,000 of John’s eligible pension income with Sara on their combined income taxes.

Scenario: After Optimal Pension Income Splitting

(John transfers $27,000 of eligible pension income to Sara)

This split creates a perfectly balanced taxable income of $53,000 each, which keeps both spouses in the same moderate tax bracket and prevents John’s higher income from being taxed at a higher marginal rate. As a result, their combined tax bill drops to $11,878, significantly lower than it would have been without income splitting. The savings come entirely from reallocating existing income — not from changing total household income.

Summary of the Example:

- Without splitting: Family pays $14,538 in tax

- With splitting: Family pays $11,878

- Total savings: $2,660

B) Maximizing the Pension Income Credit

This is one of the least-understood advantages of income splitting.

The government offers a Pension Income Tax Credit (a non-refundable credit) on the first $2,000 of eligible pension income. This credit provides a tax saving of approximately $400 per person (combining the federal and typical provincial credits).

- Without splitting: Only the spouse receiving the pension income can claim this credit, yielding about $400 in savings for the household.

- With splitting: If you split at least $2,000 of eligible pension income, the receiving spouse may also be able to claim this credit. This essentially doubles the benefit: your household can now claim two pension credits, one for each spouse, for total savings of about $800, provided the receiving spouse does not already have $2,000 or more of their own eligible pension income to claim the credit.

Important Note on Age: For the receiving spouse to claim the credit on transferred RRIF or LIF income, they must be age 65 or older. If the receiving spouse is under 65, they can only claim the credit on transferred income if it originates from an eligible source for those under 65 (like a lifetime RPP annuity).

C) Protecting Your OAS (Old Age Security)

If your personal net income exceeds a certain threshold (the OAS “clawback” limit), the government starts reducing (clawing back) your OAS payments. By splitting your income and lowering your personal net income, you reduce the risk of hitting the threshold, helping you retain 100% of your OAS benefits.

The bottom line is that Pension Income Splitting is a risk-free, simple way to manage your retirement income and maximize your family’s after-tax cash flow. If you are a retired Canadian couple with a pension, this is a conversation you need to have with your tax professional every single year.

Key Takeaways

- Pension income splitting is one of the simplest and most powerful tax tools available to retired Canadian couples.

- You can elect to transfer up to 50% of eligible pension income to your spouse on your tax return — no money needs to move.

- The strategy reduces household tax, increases eligibility for pension credits, and can help protect OAS from clawback.

- You must file Form T1032 each year you want to split income, and most tax software will automatically generate this form for you.

- Government pensions like CPP and OAS are not eligible for this tax split.

- CPP can be shared separately through Service Canada, but that is a different program with different rules.

Disclaimer: This article is for educational purposes only and is not financial or tax advice. Tax rules can change and vary by province — especially in Quebec. Please consult a qualified tax or financial professional before making any decisions.

What are your thoughts on this post? Share your comments with us.

Stay ahead of the curve. Subscribe here to get notified whenever I publish a new guide or tool.

Share your comment or feedback. We'll get back to you as soon as we can.