Spousal RRSP for Income Splitting

A simple, practical guide to how couples can reduce their lifetime tax bill.

In my previous article, Income Splitting for Canadians, I discussed three strategies Canadian couples with uneven income can use to split income to reduce taxes and build wealth.

- The high-earning spouse gives money to the low-earning spouse for investing in a TFSA.

- The high-earning spouse loans money to the low-earning spouse for investment.

- The high-earning spouse pays most or all household expenses, while the low-earning spouse invests as much of their own income as possible.

In this article, I will describe another strategy — Spousal RRSP — which is very effective in splitting income during the working phase as well as retirement. A Spousal RRSP is one of the simplest and most effective ways to fix the imbalance where one partner earns more than the other. It allows couples to split income well before age 65 and throughout retirement, significantly reducing lifetime taxes.

This guide explains how it works, when it makes sense, and how to use it strategically.

What Is a Spousal RRSP?

A Spousal RRSP is an RRSP opened in the lower-income spouse’s name (the annuitant), but funded by the higher-income spouse (the contributor). While these are the official terms, in common language, the low-income spouse is often called the owner and the higher-income spouse the contributor of the spousal RRSP account.

- Note: The spousal RRSP account is also available to common-law partners. In fact, the CRA officially names it “Spousal or Common-Law Partner RRSP.” In this article, any reference to spouse is also applicable to a common-law partner.

How the Spousal RRSP Works?

- The contributor makes a contribution to the Spousal RRSP out of their available RRSP contribution room.

- The annuitant who owns the account controls the account and makes the investment decisions, that how and where to invest the contribution money. A Spousal RRSP account may be self-directed or managed by a financial institution.

- Investment growth stays tax-deferred like a traditional RRSP account.

- Withdrawals are taxed as income to the annuitant (owner), which is the low-income spouse. (Note: The crucial exception to this is the 3 Calendar-Year Attribution Rule, which is explained later in this article.)

This structure allows a high-earner to shift future taxable income to their low-income spouse — legally and efficiently.

Example — John and Sara

Let us understand the working of Spousal RRSP with the help of an example. John and Sara are a couple who live in Ontario. John earns an annual income of $140,000, and Sara earns $35,000 per year.

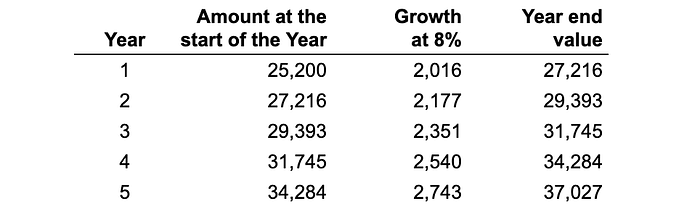

John earns an annual income of $140,000. For the purposes of this example, let’s assume his RRSP contribution room for the year is $25,200 (18% of his earned income, up to the annual maximum). He has two contribution options for $25,200.

- Contribute $25,200 to his individual RRSP account.

- Contribute $25,200 to Sara’s Spousal RRSP account.

At $140,000 yearly income, John’s marginal tax rate is 43.41% as per the 2025 tax rates. At this marginal tax rate, he would save significant taxes (approximately $10,883), whether he contributes this amount to his RRSP or Sara’s Spousal RRSP.

Like a regular RRSP, the investments in a Spousal RRSP will continue to grow tax-free. However, when the money is withdrawn after a few years or in retirement, it will be taxed in Sara’s hands. Since Sara’s income at the time of withdrawal is expected to be significantly lower than John’s, the couple will pay low taxes as compared to if the money were invested in John’s RRSP.

Let us assume that both RRSP and Spousal RRSP grow at 8% per year. The account value at the end of 5 years will be $37,027.

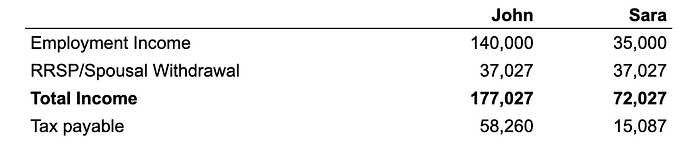

Assuming that John and Sara’s annual income remains the same after 5 years, at current (2025) tax rates, here are the taxes payable on their employment income:

Next, assume the full amount ($37,027) is withdrawn in the 6th year. As 100% of RRSP withdrawals are taxed as ordinary income, the following table illustrates the effect of the withdrawal on their income taxes.

Now, let us compare the total taxes payable by the couple in both scenarios (Employment Tax + Withdrawal Tax):

Scenario A: Withdrawal from John’s Individual RRSP

In this case, the couple’s total tax payable is the sum of John’s total tax (on $140,000 employment + $37,027 withdrawal) and Sara’s tax on her employment income ($35,000).

- John’s Total Tax ($58,260) + Sara’s Employment Tax ($5,916) = $64,176

Scenario B: Withdrawal from Sara’s Spousal RRSP

In this case, the couple’s total tax payable is the sum of John’s tax on his employment income ($140,000) and Sara’s total tax (on $35,000 employment + $37,027 withdrawal).

- John’s Employment Tax ($41,782) + Sara’s Total Tax ($15,087) = $56,869

Tax Savings:

- Tax savings with the Spousal RRSP vs RRSP: $64,176 — $56,869 = $7,307

Thus, the spousal RRSP resulted in a tax saving of $7,307 for a single contribution of $25,200 over 5 years. As long as Sara’s annual income is significantly lower than John’s annual income, Spousal RRSP will result in significant tax savings, whether the money is withdrawn during the working phase or retirement.

3-Calendar-Year Attribution Rule

When using a Spousal RRSP, couples must be careful about the 3 Calendar-Year Attribution Rule, as it affects whether the withdrawals will be taxed in the hands of the contributor or the plan owner.

The 3-calendar-year attribution rule for spousal RRSPs states that if the annuitant (the spouse who owns the plan) withdraws funds within the same calendar year a contribution was made or within the next two calendar years, the withdrawn amount must be included in the contributing spouse’s taxable income.

This rule intends to prevent couples from exploiting the tax system by having a higher-earning spouse contribute to a lower-earning spouse’s Spousal RRSP for an immediate tax deduction, followed by a quick withdrawal taxed at the lower-income spouse’s rate. In other words, in the absence of this rule, a higher-earning spouse could contribute $25,000 to a Spousal RRSP owned by the low-earning spouse in Dec 2025, get a tax deduction at a high marginal tax rate on their 2025 tax return, and then the lower-earning spouse could withdraw that $25,000 in early 2026, and use it for any purpose, including reinvestment or household expenses.

It is crucial to remember this is a 3-calendar-year rule, not a 36-month rule. If contributions are made in 2025 (even in December), the annuitant (Spousal RRSP owner) must wait for two full calendar years (2026 and 2027) before withdrawing funds. Any withdrawal made on January 1, 2028, or later will be taxed in the annuitant’s (owner’s) hands. Withdrawals before this date will be attributed to and taxed in the contributor’s hands, which nullifies the original tax benefit.

Another point to remember in the context of the 3-calendar-year rule is that whenever a new contribution is made to a Spousal RRSP, the 3-calendar-year window resets. That is, after contributing in 2025, if another contribution is made in 2026, the annuitant (plan owner) now must wait until January 1, 2029, for withdrawals to be taxed in the annuitant’s hand.

The Aggregate Rule: Why Multiple Accounts Won’t Work

A common misconception is that a couple can bypass the attribution rule by segregating contributions into multiple Spousal RRSP accounts. However, the CRA applies the 3-calendar-year rule to all spousal plans held by the annuitant in aggregate.

The rule is triggered if the contributor has made a contribution to any Spousal RRSP for that specific partner within the three-year window. The CRA does not track each account in isolation; instead, it looks at the total “tainted” contributions made by the spouse across all spousal accounts.

Example of the “Aggregate Trap”:

To illustrate how easily this rule can be triggered, consider the following scenario:

- Year 1: You contribute $5,000 to Spousal RRSP A.

- Year 2: You stop contributing to Account A and open Spousal RRSP B, contributing $5,000 there.

- Year 3: You contribute another $5,000 to Spousal RRSP B.

- Year 4: Your spouse withdraws $5,000 from Spousal RRSP A.

Even though you haven’t contributed to Account A for three calendar years, the $5,000 withdrawal is fully attributed to you (the contributor). This is because you made contributions to Account B during the three-calendar-year window (Year 2, Year 3, and Year 4). From the CRA’s perspective, a contribution to one spousal plan is a contribution to all.

The Only Real Solution: The “Complete Stop”

Because of this aggregate rule, the only way to ensure withdrawals are taxed in the lower-earning spouse’s hands is to completely cease all contributions to all Spousal RRSPs for that specific spouse for at least two full calendar years.

If the couple wishes to continue saving for retirement during this “waiting period,” the higher-earning spouse should contribute to their own individual RRSP instead. This allows the Spousal RRSP “clock” to run out across all accounts without being reset by new contributions.

Exceptions to the 3-Calendar-Year Attribution Rule

There are a few exceptions to the 3-calendar-year attribution rule. The important ones include:

- The death of either spouse or the breakdown of the marriage/common-law relationship, resulting in separation.

- A withdrawal made under the Home Buyers’ Plan (HBP) or the Lifelong Learning Plan (LLP).

- For a spousal Registered Retirement Income Fund (RRIF), the attribution rule does not apply to the minimum annual withdrawal amount.

Example: The 3-Year Attribution Rule Lifecycle:

Suppose you make your final contribution to a Spousal RRSP in 2026. Your spouse then converts the account to a Spousal RRIF later that same year.

- In 2026 (Year of Conversion): There is no mandatory minimum. Any withdrawal made this year will be taxed in your hands (the contributor) because the 3-year window is active.

- In 2027 & 2028: Your spouse takes the mandatory minimum withdrawal (e.g., $3,000). This specific minimum amount is taxed in your spouse’s hands. However, if they withdraw more than the minimum, that extra amount is still taxed in your hands.

- In 2029 (The “All-Clear”): Three full calendar years (2026, 2027, and 2028) have now passed since your last contribution. Your spouse can now withdraw any amount they want from the RRIF — not just the minimum — and the entire sum will be taxed in their hands, regardless of your previous contributions.

Other Rules applicable to Spousal RRSP

We have discussed the most important rules that govern Spousal RRSPs. Here are the other rules that you should be aware of:

- Spousal RRSP contributions use the contributor’s RRSP room, not the spouse’s.

- You can contribute to a Spousal RRSP until the end of the year the annuitant spouse turns 71, regardless of the contributor’s age.

When to Think Twice About a Spousal RRSP

While highly effective, the Spousal RRSP may not be the optimal choice if:

- The Low-Income Spouse Expects Higher Income Later: If the low-income spouse expects to earn significantly more than the contributor during retirement (e.g., due to a large future pension or inheritance), the benefit of income splitting is reduced or eliminated.

- Control over Funds is an Issue: Since the account is legally owned by the annuitant (the low-income spouse), they retain sole authority over investment decisions and future withdrawals. The contributor has no legal control over the funds once the contribution is made.

Why Use a Spousal RRSP?

I am sure that after reading the article up to this point, you have a fairly good idea why a couple should use a Spousal RRSP. In brief, it is a powerful tool to balance assets between partners when one spouse earns significantly more than the other.

Spousal RRSPs help to:

- Even out their future retirement income streams by preventing one partner’s RRSP from growing too large.

- Reduce the couple’s combined current-year taxes by claiming the deduction at the high-earner’s marginal tax rate.

- Reduce the couple’s combined retirement tax bill by splitting taxable RRSP withdrawals between two partners who hold nearly the same account values.

- Even out withdrawals from their RRSP (and Spousal RRSP) accounts, thereby reducing the combined taxes payable.

- Help prevent or reduce Old Age Security (OAS) clawbacks in retirement for the higher-earning partner.

- Reduce taxes when a partner receives a one-time, large income (e.g., a bonus or severance) during a particular year.

- Simplify estate planning and reduce final tax liability by distributing retirement assets between spouses, which minimizes the eventual large tax hit that occurs when the last surviving spouse passes away.

- Help plan for an early retirement (See the next section.)

Ultimately, it will result in lower taxes payable during their lifetime. For many couples, equalizing retirement income can result in savings of tens of thousands of dollars in lifetime taxes.

Using Spousal RRSP for Early Retirement Planning

Most government benefits, like OAS and CPP, typically start at age 65. If a couple plans to retire early, perhaps at age 55 or 60, a Spousal RRSP is an excellent tool to enable income splitting prior to age 65. (After age 65, couples can take advantage of Pension Income Splitting, which we will discuss in the next article.) Let us understand this strategy using the example of John and Sara.

John, aged 30, earns an employment income of $140,000, and Sara, also aged 30, earns an employment income of $35,000.

- Sara’s income is too low to give any advantage of saving in an RRSP. She would invest all savings, including any money gifted by John, in her TFSA account.

- John plans to use $25,000 of his contribution room for an RRSP contribution. This contribution results in initial tax savings of approximately $10,807 (based on the marginal tax rate of about 43.41%).

- Instead of saving the entire amount in his individual RRSP account, he contributes $12,500 each to his individual RRSP and Sara’s Spousal RRSP accounts.

- John continues this pattern of contributions for 25 years. He invests any additional savings in his TFSA account or other non-registered accounts.

Assuming that the RRSP accounts earn an inflation-adjusted growth of 6%, after 25 years, both RRSP accounts will have a value of $726,955 each.

Note: I am using an inflation-adjusted return; therefore, the value of $726,955 represents its purchasing power in today’s dollars. If you feel that your accounts will earn lower returns, the account values will reduce accordingly. For example, at 5% inflation-adjusted returns, the end value will be about $626,418.

Now, both John and Sara are 55. They want to retire now and need about $94,000 after-tax income.

- Based on current tax rates, a $60,000 withdrawal from an RRSP results in $13,023 in tax, yielding an after-tax income of $46,977.

- Therefore, if both John and Sara withdraw $60,000 from their respective RRSP accounts, they will have a combined after-tax income of about $94,000.

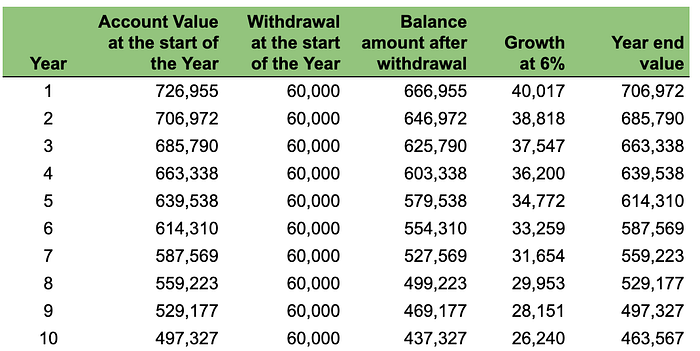

Assuming that their RRSP accounts continue to earn an inflation-adjusted growth of 6%, the following table illustrates changes in the accounts for 10 years, until they turn 65.

The couple’s total contributions amounted to $625,000 ($25,000 x 25). Over the first 10 years of retirement (age 55–65), they withdraw a total of $1,200,000 ($600,000 from each RRSP account). Notice that these accounts still hold a substantial balance of $927,114 ($463,557 each), which they can use for the next phase of retirement (65+). As CPP, OAS, and other credits kick in at age 65, they will need to withdraw a much smaller amount (about $26,000 each) to get after-tax income of about $94,000 per year.

Key Takeaway

The key takeaway here is the significant tax efficiency achieved between ages 55 and 65. By equalizing the RRSP balances early on, John and Sara were able to draw $1,200,000 in taxable income during their pre-65 years, minimizing their tax bracket exposure in every single year. This strategy allows couples to bridge the income gap until government benefits begin, maximizing the value of their RRSP savings while ensuring they pay the least amount of tax possible on their early retirement withdrawals.

🚀 Final Thoughts

The Spousal RRSP is arguably the most powerful income-splitting strategy available to Canadian couples with uneven incomes. It provides tax relief during the high-earning years (via the deduction) and prevents massive tax inefficiency during retirement (via the withdrawal split).

As demonstrated in the examples of John and Sara, strategic use of a Spousal RRSP can deliver two major advantages:

- Lower Annual Taxes: Immediate tax savings in the working years.

- Financial Longevity: The ability to efficiently fund an early retirement and protect government benefits like OAS in later life.

If your retirement assets are heavily weighted toward the higher-earning spouse, evaluating a Spousal RRSP strategy is a crucial step toward achieving tax-efficient retirement and realizing potential savings of tens of thousands of dollars over your lifetime.

Note: Pension income splitting can also help to reduce a couple’s overall tax burden. You can read more about this in the article: Pension Income Splitting.

Disclaimer: This article is for educational purposes only and is not financial or tax advice. Please consult a qualified tax or financial professional before making any decisions.

What are your thoughts on this post? Share your comments with us.

Stay ahead of the curve. Subscribe here to get notified whenever I publish a new guide or tool.

Share your comment or feedback. We'll get back to you as soon as we can.