The RRSP Trap: Why Middle-Class Canadians Should Be Careful (Part 3)

A stress test of the 5% real return: Why lower growth rates won’t save you from the “Tax-and-Clawback” cycle.

In The RRSP Trap: Why Middle-Class Canadians Should Be Careful (Part 1), I demonstrated how a middle-aged Canadian could potentially leave behind an estate about $1 million larger simply by prioritizing a TFSA over an RRSP.

While the response was overwhelmingly positive, some readers questioned my use of a 6% inflation-adjusted (real) growth rate. The concern was that if actual returns were lower, the “RRSP Trap” might disappear.

I maintain that a 6% real (inflation-adjusted) return is a conservative and historically grounded expectation. To put this in perspective, as of December 2025, the 10-year annualized total return for the S&P 500 has exceeded 16% in CAD terms. Similarly, the MSCI World (Global) index has delivered an annualized return of approximately 12.6% over the last decade.

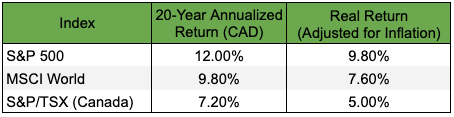

The following table shows the 20-year performance for three major indexes in Canadian dollars:

While the Bank of Canada officially targets 2.0% inflation, the average has been pushed slightly higher by the significant “inflation spike” of 2021–2023. Over the last 20 years (2005–2025), Canada’s average annualized inflation rate has been approximately 2.2%.

When we subtract inflation from market performance, the results remain robust. The following table shows the 20-year inflation-adjusted (real) returns for these indexes:

By using a 6% assumption in my analysis, I am essentially building in a 3 to 4% “safety buffer” to account for potential market cooling or higher-than-expected inflation. If your portfolio is well-diversified and primarily equity-based, achieving this 6% baseline should not be difficult. If your returns are consistently lower, it is often a sign of poor diversification or — more commonly — paying excessive management fees that erode your wealth.

While a 6% annual real return is historically conservative and well within reach for a disciplined investor, I recognize that the future rarely perfectly mirrors the past. To ensure this strategy remains robust even in a ‘lower-for-longer’ growth environment, let us see how the TFSA vs. RRSP analysis unfolds if real annual returns drop to 5%.

Note: The FP Canada 2025 Projection Assumption Guidelines — the standard used by certified financial planners — suggest a real return of approximately 4.5% to 5.0% for diversified equity portfolios.

1. Meet the Candidates

To understand the impact of lower returns, let’s revisit our two middle-class Canadians: John and Bob. Both are 30 years old, earn a steady employment income of $66,000 per year, and commit to saving $11,880 (pre-tax) annually over the next 35 years.

- John (The RRSP Route): John contributes his full $11,880 to his RRSP. Based on 2026 Ontario tax rates, this contribution saves him $3,179 in taxes. After accounting for his contribution and this refund, his take-home “net” income is $42,498.

- Bob (The TFSA Route): Bob pays his taxes first. To match John’s lifestyle exactly, he invests $8,358 into his TFSA. This leaves him with a net income of $42,498 — exactly the same as John’s.

Both will hold their investments for 35 years until age 65. Let’s see how the “RRSP Trap” functions when we compare a 6% real return against a more conservative 5% “stress-test” scenario.

2. The 35-Year Growth Phase (Age 65)

John invests $990 per month ($11,880/year) into his RRSP, while Bob invests $725 per month ($8,700/year) into his TFSA. (Bob can contribute these amounts because he utilized his carry-forward TFSA room).

Using the Ontario Securities Commission’s Compound Interest Calculator (compounded annually), the account values for John and Bob at age 65 are as follows:

Note: Bob’s TFSA figures reflect the $725/month contribution over 35 years.

At a 6% growth rate, John’s RRSP appears to be ahead by $364,025. Even when we stress-test the math at 5%, the gap remains a substantial $293,742 in John’s favour.

On paper, John looks like the clear winner. But this is where the “Trap” is set. John’s $1.1M to $1.36M balance is a gross figure — a shared account with the CRA. Bob’s balance, however, is 100% his to keep.

3. Bob’s Retirement Journey

As established in Part 2 of this article, based on 2026 tax rates for an Ontario resident, Bob enters retirement at age 65 with a solid foundation. He is expected to receive total OAS and CPP benefits of $24,916 (in today’s dollars). On top of his other benefits, he will receive roughly $5,300 annually from the Guaranteed Income Supplement (GIS).

To maintain his target after-tax lifestyle of $42,498, Bob only needs to withdraw $12,577 per year from his TFSA. Because TFSA withdrawals are not considered “taxable income,” his total tax bill remains a negligible $295 (tax on his base CPP/OAS).

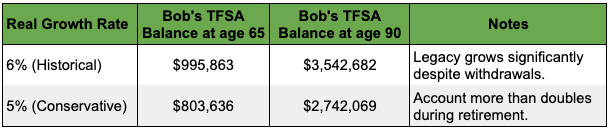

The real magic happens with his remaining balance. Because he only withdraws a small fraction of his wealth, his TFSA continues to compound. At the end of a 25-year retirement (age 90), Bob’s account balance is staggering:

4. John’s Retirement Journey: The Calm Before the Storm

For the first six years of retirement (age 65 to 71), John’s experience seems manageable. To maintain his $42,498 after-tax lifestyle, John withdraws $22,524 annually from his RRSP.

When combined with his $24,916 in CPP and OAS benefits, his total gross income is $47,440. After paying $4,942 in taxes (based on 2026 Ontario rates), he hits his target spendable income exactly.

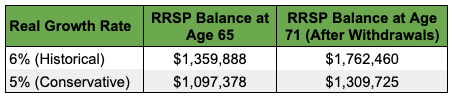

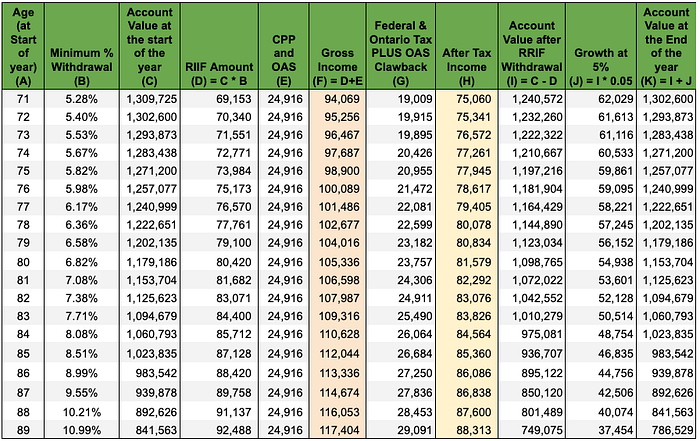

However, because his RRSP balance is so large, his small withdrawals are not enough to deplete the account. In fact, the account continues to grow faster than he is spending it. By the time he reaches age 71 — the deadline to convert his RRSP into a RRIF (Registered Retirement Income Fund) — his balance has ballooned:

Withdrawals from RRIF

At age 71, the flexibility of the RRSP ends. John is required by law to convert his RRSP into a RRIF (Registered Retirement Income Fund) and begin mandatory annual withdrawals. These minimums are not based on what John needs to live, but on a government-mandated percentage of his account balance as of January 1st each year. (For details, see Section 4 of Part 2 of the article.)

The table below illustrates the “Final Reckoning.” Even with a conservative 5% real growth rate, John’s large account balance triggers a chain reaction of high taxable income, spiked marginal tax rates, and the dreaded OAS clawback.

John’s Secondary Investments: TFSA and Non-Registered

Because John’s forced RRIF withdrawals provide an after-tax income significantly higher than his $42,498 annual spending, he is left with a “problem” Bob doesn’t have: he must find a new home for his extra cash.

Since John never used his TFSA earlier in life, he enters retirement with approximately $362,500 in carry-forward room. He diligently funnels his surplus RRIF income back into a TFSA, which continues to grow at a 5% real rate. By age 90, this “secondary” TFSA has grown to $921,059.

However, even a maximized TFSA isn’t enough to hold all of John’s forced RRIF wealth. He is eventually forced to invest the remaining surplus in a non-registered account. Here, he meets a new enemy: Dividend Tax Drag. Because he must pay taxes on his investment earnings every year (even if he doesn’t sell), his effective growth rate is lower than 5%. By age 90, this taxable account holds $289,059, including a capital gain of $11,064.

At age 90, John’s investment accounts are expected to have the following values:

The “Death Tax” Reality

If John were to pass away at age 90, while the TFSA balance flows to his estate entirely tax-free, the RRIF balance is a different story — the full RRIF balance would be included as income on his final tax return, and 50% of the capital gains in the non-registered account would also become taxable. The large RRIF balance would push John’s marginal tax rate close to 50%. Based on 2026 Ontario tax rates, John’s final tax bill will consume nearly half of his RRIF’s value. Here is the final breakdown:

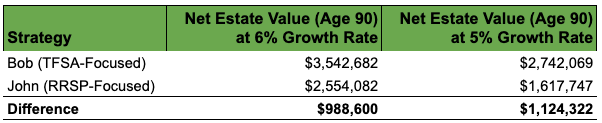

5. Comparing Bob’s and John’s Retirement Journeys

If both Bob and John were to pass away at age 91, the net value of their estates — after all taxes and clawbacks — tells a powerful story.

Why the “Gap” Widened to Over $1.1 Million

At first glance, you might expect lower returns to favour John (since his mandatory withdrawals are smaller). However, the GIS “Bonus” acts as a powerful equalizer for Bob:

- The GIS Growth Multiplier: Bob received approximately $5,300 every year in tax-free GIS payments. Because he didn’t “need” this money to maintain his lifestyle, it stayed in his TFSA, compounding tax-free. At 5%, that “extra” GIS alone grew into a significant portion of his final estate.

- The “Tax Floor”: Even with lower returns, John still faces a minimum tax floor. He is forced to withdraw from his RRIF, which continues to trigger taxes and disqualify him from the GIS. Bob’s “tax rate” on his TFSA withdrawals remains 0%, no matter what the market does.

- Efficiency in Scarcity: In a lower-return environment, every dollar lost to tax hurts more. John’s losses to the CRA and OAS clawbacks represent a larger percentage of his total growth than they did at 6%.

The Lesson: The TFSA is “Recession-Proof”

This proves that the RRSP Trap isn’t just a “bull market problem.” Even in a conservative 5% growth environment, the structural advantage of the TFSA — combined with the “secret” GIS benefit — creates a million-dollar difference in legacy.

Final Score at 5%: Despite John having a larger “paper” portfolio for his entire life, Bob ends up leaving $1,124,322 more to his heirs. The TFSA didn’t just win; it dominated.

6. Final Word: Rethinking the “Default” Strategy

For decades, Canadians have viewed the RRSP as the default retirement strategy. We are lured by the immediate gratification of a tax refund, often ignoring the long-term “partnership” we are signing with the CRA — a partnership where the government eventually dictates how much you must withdraw and how much of your inheritance they will keep.

As John and Bob’s journeys demonstrate, this partnership is expensive. Even when we “stress-test” the math with a conservative 5% real return, the TFSA’s structural advantages are undeniable. By keeping his income “invisible,” Bob didn’t just avoid taxes; he qualified for a $5,300 annual government bonus (GIS) that John was forced to walk away from.

The RRSP is not inherently “bad,” but for a middle-class earner, it is a bet that your future tax rate will be lower than it is today. As John discovered, if your investments actually grow, that is a very difficult bet to win. Don’t let a $3,500 refund today cost you a million-dollar legacy tomorrow.

The Bottom Line: Contribution decisions matter, but your withdrawal strategy determines your true wealth.

Disclaimer: This article is for educational purposes only and is not financial or tax advice. Please consult a qualified tax or financial professional before making any decisions.

What are your thoughts on this post? Share your comments with us.

Stay ahead of the curve. Subscribe here to get notified whenever I publish a new guide or tool.

Share your comment or feedback. We'll get back to you as soon as we can.