The Non-Registered Account Explained in Plain English

Non-registered accounts complement TFSAs and RRSPs, providing flexibility for Canadians who have already maximized other registered savings options.

Most Canadians understand their TFSA and RRSP, but few fully understand the third pillar of investing: the non-registered account. Yet for many Canadians, especially those in the middle- and higher-income range, non-registered accounts can be incredibly powerful for long-term retirement planning and for transferring wealth to the next generation. This article breaks it down in plain English: what it is, how it works, how it’s taxed, and how it compares with your TFSA and RRSP. If you’ve ever wondered when or why to use a non-registered account, this guide will give you clear, practical answers.

What Is a Non-Registered Account?

A non-registered account is simply an account that is not a registered or special-purpose account like an RRSP, TFSA, FHSA, RESP, or RDSP. Because it isn’t registered under any specific government program, it doesn’t come with the tax advantages or restrictions attached to those accounts — but it does offer complete flexibility, unlimited contribution room, and full access to your money at any time.

In that sense, your chequing, savings, and high-interest savings accounts are also non-registered accounts. There are no contribution limits and no withdrawal restrictions — you can put in as much as you want and take out money whenever you want. There are no age-related requirements, and you can continue using the account for as long as you like.

Other assets, such as a rental property or cottage (other than your principal residence), are also considered non-registered for tax purposes, even if not held inside a bank or brokerage account.

You can hold almost anything inside it:

- Stocks and ETFs

- Mutual funds

- Bonds

- GICs

- Cash

- Gold and other precious metals

- and more

How Non-Registered Accounts Are Taxed

Non-registered accounts give you flexibility and unlimited contribution room, but the trade-off is that investment income is taxable in the year it is earned. The tax treatment varies depending on the type of income: capital gains, dividends, or interest. Understanding these differences can help you invest more efficiently and reduce your overall tax bill.

1. Capital Gains — the Most Tax-Efficient Income

When you sell an investment for more than you paid for it, the profit is called a capital gain. Only 50% of a capital gain is taxable in Canada, which makes it the most tax-efficient type of income for non-registered accounts.

Example:

- Buy a stock for $10,000

- Sell it later for $15,000

- Capital Gain = $5,000

- Taxable amount = $2,500 (i.e. 50% of the Capital Gain)

- If your marginal tax rate is 30%, tax = $750

The remaining $4,250 ($5,000 - $750) is yours to keep. You only pay the tax when you sell, giving you control over the timing and potentially lowering the taxes you owe each year.

For example, imagine you invested $5,000 each year over the last 10 years in a non-registered account. If the stocks you bought have appreciated and the current value of your account is $200,000, you don’t pay any tax until you sell those shares to realize a profit. This can continue for decades, even into retirement — allowing non-registered account holders to choose exactly when to pay tax on their profits, which provides tremendous flexibility for long-term planning.

Capital gains also come with a related concept called a capital loss. A capital loss happens when you sell an investment for less than what you paid for it. Capital losses aren’t pleasant, but they do happen, and they can actually be useful. You can use capital losses to reduce the taxes you owe on your capital gains.

This is known as tax-loss harvesting — if some investments lose value, you can sell them to realize a capital loss and use that loss to offset taxable gains from other investments, reducing your overall tax bill.

2. Dividends — Tax Credits Can Help

Dividends are payments made by a company to its shareholders out of its profits. When you own shares in a company, you may receive dividends as a way for the company to share its earnings with you.

Dividends from eligible Canadian companies are taxed at a much lower rate than interest income (such as GIC interest). This is because the CRA assumes the company has already paid corporate tax before distributing the dividend. To avoid taxing the same income twice, individuals receive a dividend tax credit (DTC).

This makes eligible Canadian dividends more tax-efficient than interest income. Dividend tax credit calculations can be confusing, so let’s walk through a simple example.

You receive $10,000 in eligible Canadian dividends

Gross-up

The actual dividend received ($10,000) is increased by 38% to determine the taxable dividend amount, i.e.

Grossed-up amount = $10,000 × 1.38 = $13,800

This “gross-up” reflects the company’s pre-tax earnings before paying corporate income tax.

Taxation at your marginal rate

The grossed-up amount is added to your other income and taxed at your marginal tax rate (MTR). For example, if your other income is $60,000 and you live in Ontario, in 2025, the $13,800 would be taxed at an MTR of approximately 29.65%.

Dividend Tax Credit (DTC)

The DTC is then applied to reduce your tax payable. It has federal and provincial components, both calculated on the grossed-up amount.

For Ontario in 2025, the combined DTC on $13,800 is approximately $3,453.

Net tax effect

The DTC reduces the tax you would otherwise owe on the grossed-up dividend. Because the DTC is calculated solely on the grossed-up dividend amount, and not your income bracket, the relative benefit is largest at lower income levels.

In some cases, especially for individuals in lower income brackets, eligible dividends can even result in lower total tax payable compared to having no dividend income at all. This becomes clear when you look at the numbers.

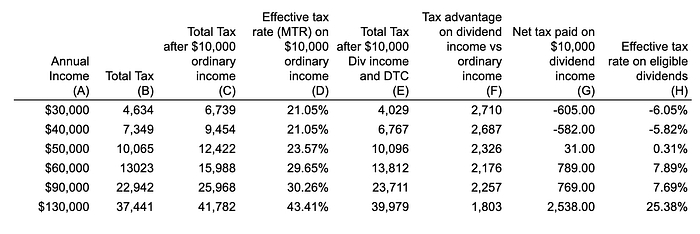

Below is a simple illustration.

- Column A contains the annual salary income for Ontario residents.

- Column B shows the total tax payable on that income, based on the Wealthsimple tax calculator for 2025 tax rates.

- Column C shows the total tax payable when the same person earns an additional $10,000 of ordinary income, such as interest income or RRSP withdrawals (which are 100% taxable).

- Column D shows the marginal tax rate applied to the additional $10,000 of ordinary income, calculated as:

(C − B)÷10,000 - Column E shows the tax payable when the person instead receives $10,000 of eligible Canadian dividends, after applying the dividend gross-up and DTC.

- Column F shows the tax advantage of receiving eligible dividends instead of ordinary income, calculated as: C−E

For example, if Column C is $6,739 and Column E is $4,029, the tax advantage is $2,710. - Column G shows the net tax payable on the $10,000 dividend itself.

- Column H shows the effective tax rate on that dividend income.

Two important conclusions emerge from this comparison:

- Across all income levels, the effective tax rate on eligible dividends is significantly lower than the marginal tax rate on ordinary income.

- For incomes below approximately $40,000, receiving an additional $10,000 of eligible dividends actually reduces total tax payable — a surprising result that highlights how powerful the DTC can be at lower income levels.

Finally, keep in mind:

- Dividends from non-eligible Canadian companies receive a smaller tax credit than the one discussed above.

- Foreign dividends — such as those from U.S. companies — do not qualify for the Canadian dividend tax credit. They are taxed at your full marginal rate and may also be subject to foreign withholding tax. However, you may be able to claim a foreign tax credit to offset some or all of the withholding tax, reducing your net tax payable.

3. Interest — Least Tax-Efficient Income

Interest income is fully taxable at your marginal tax rate, making it the least tax-efficient income in a non-registered account. This includes:

- GIC interest

- Bond interest

- High-interest savings products

Example:

If you earn $1,000 in interest and your marginal tax rate is 40%, you pay $400 in tax.

Because 100% of interest income is taxable at your marginal rate, many investors avoid holding interest-heavy investments in non-registered accounts if other options (TFSA or RRSP) exist.

Advantages of a Non-Registered Account

1. Unlimited Contribution Room

Unlike RRSPs and TFSAs, which have fixed contribution limits, non-registered accounts allow you to invest as much as you want. This is especially valuable for Canadians who:

- Have already maxed out their TFSA and RRSP

- Want to invest large amounts (e.g., inheritance, bonuses, proceeds from a home or business sale)

- Plan to retire early and need flexible, unrestricted funds

2. Full Flexibility

You can withdraw money at any time with no penalties, no withholding tax, and no restrictions. You have complete control — contribute or withdraw whatever your financial situation requires.

3. Capital Gains Are Tax-Efficient

As discussed earlier, only 50% of capital gains are taxable. This gives long-term, growth-focused investors a major advantage: low annual taxes and full control over when to realize gains (and therefore when to pay tax).

4. Ability to Harvest Capital Losses

If an investment drops in value and you sell it at a loss, that capital loss can be used to offset capital gains, reducing your tax bill. Capital losses can also be carried forward indefinitely or applied to offset capital gains from the previous three tax years. This strategy is not available in a TFSA or RRSP.

5. No Forced Withdrawals

RRSPs must convert to RRIFs and begin mandatory withdrawals at age 71. Non-registered accounts have no age limits, no minimum withdrawals, and no timing rules.

Disadvantages of a Non-Registered Account

1. You Pay Tax Every Year

Even if you don’t withdraw money, you may still owe tax on:

- Dividends

- Interest

- Fund distributions

Eligible Canadian dividends are taxed favourably, but interest and high distributions can still create a tax burden. By holding more low-dividend or non-dividend growth stocks in your non-registered account, you can reduce this impact.

2. More Record-Keeping

You must track adjusted cost base (ACB) and realized capital gains or losses for tax filing. Most financial institutions now track ACB and provide year-end summaries, so while this is a responsibility, it’s not a major obstacle.

3. Less Tax Shelter for High-Turnover Funds

ETFs or mutual funds with frequent internal trading often generate taxable annual distributions. In an RRSP or TFSA, these are sheltered — but in a non-registered account, they create a tax drag. This can be managed by choosing the right investment mix for your non-registered account.

4. Interest Income Is Highly Taxed

GICs, bonds, and other interest-producing investments generate fully taxable income. Because 100% of interest income is taxable, it is the least tax-efficient type of return to hold in a non-registered account. High-interest investments are often better held in a TFSA or RRSP to avoid the full marginal tax hit.

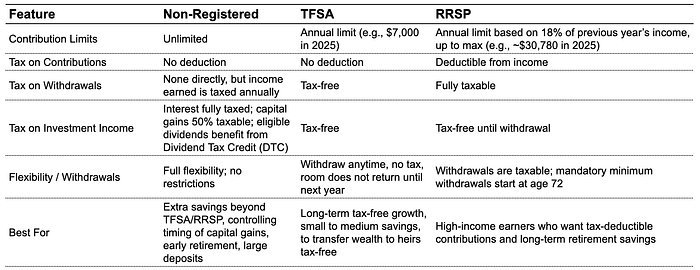

Non-Registered vs TFSA vs RRSP

Here’s a quick comparison to help you see how non-registered accounts fit alongside TFSAs and RRSPs:

Note: This section provides a quick side-by-side comparison. In future articles, I’ll dive deeper into Non-registered vs TFSA and Non-registered vs RRSP — including when each account makes the most sense depending on your income, taxes, and long-term goals.

Final Thoughts

Non-registered accounts are an important part of a Canadian’s investment toolkit. They provide flexibility, unlimited contribution room, and control over taxes, making them ideal for investors who have already maximized TFSA and RRSP contributions or want to manage the timing of their capital gains.

Key takeaways:

- Tax efficiency matters: Capital gains and eligible dividends are taxed more favourably than interest, and capital losses can be carried forward indefinitely or applied to the previous three years’ gains.

- Flexibility is powerful: You can withdraw anytime without restrictions, giving you options for early retirement, large purchases, or unexpected needs — unlike RRSPs, which have mandatory minimum withdrawals starting at age 72.

- Strategic planning pays off: By holding the right mix of investments — such as low-dividend growth stocks or tax-efficient funds — you can reduce the annual tax burden.

- Complement, don’t replace: Non-registered accounts work best alongside TFSAs and RRSPs to maximize long-term wealth accumulation and tax efficiency.

- Wealth transfer considerations: TFSAs allow tax-free transfers to heirs, while non-registered accounts can also be planned strategically to minimize taxes on estate transfers.

Non-registered accounts help you grow, protect, and manage wealth, giving you more control over taxes, withdrawals, and timing of capital gains.

Disclaimer: This article is for educational purposes only and is not financial or tax advice. Please consult a qualified tax or financial professional before making any decisions.

What are your thoughts on this post? Share your comments with us.

Stay ahead of the curve. Subscribe here to get notified whenever I publish a new guide or tool.

Share your comment or feedback. We'll get back to you as soon as we can.