Income Splitting for Canadians

A simple, practical guide to how couples can legally reduce their household tax bill.

In most Canadian families today, both partners rarely earn the exact same income. Sometimes there’s a single earner while the other focuses on managing the home and children, especially during the school years. In other cases, one partner earns more — a 60/40 or 70/30 split is common. Income can also shift when one spouse takes parental leave, returns to school, works part-time, or is unable to work due to illness. Since Canada taxes individuals rather than households, the natural question is: Are there any legitimate ways to share or split income to reduce the overall family tax bill?”

One thing a higher-earning partner cannot do is simply gift or transfer money to the lower earner to invest. CRA does not permit this due to attribution rules:

If money or property is gifted, loaned or transferred to a spouse or common-law partner, and that money or property is invested by the receiving spouse or common-law partner to generate income, that income, including any interest, dividends and capital gains, will normally be attributed back to the person who gave the gift or loan.

In other words, John, earning $100,000 can’t give $30,000 to his spouse Sara to invest and enjoy the returns. CRA attribution rules will require all income and capital gains from the investments made by Sara using that $30,000 back to John. That is, John will need to include all income from that investment in his tax return.

However, there are three ways to overcome the attribution rules:

- Give money to your spouse or common-law partner to invest in their TFSA.

- Loan money to your spouse or common-law partner at an interest rate prescribed by CRA.

- The high-earning spouse covers most or all household expenses, allowing the low-earning spouse to invest as much of their own income as possible.

Giving Money to Spouse or Common-Law Partner for Investing in TFSA

A high-earning spouse can legally give money to their low-earning spouse for investing in their TFSA without triggering the attribution rules. This is explicitly stated in the CRA document RC4466 Tax-Free Savings Account (TFSA), Guide for Individuals, under the Contributions section:

You can give your spouse or common-law partner money so that they can contribute to their own TFSA, and this amount or any earned income from that amount will not be allocated back to you. The total contributions you each make to your own TFSAs cannot be more than your TFSA contribution room.

This strategy is especially useful when the high-income spouse has already maximized both their RRSP and TFSA. Instead of investing additional funds in a non-registered account, where interest, dividends, and capital gains are taxable, the higher-income spouse can gift money to the lower-income spouse to invest inside their TFSA.

The benefits include:

- Tax-free growth: All income and growth inside the spouse’s TFSA remains completely tax-free.

- Tax-free withdrawals: The low-earning spouse can withdraw funds at any time without triggering tax.

- Flexible use of withdrawals: Withdrawn amounts can be used for any purpose, including retirement income or gifting to children or other family members.

In effect, gifting money to the lower-earning spouse for TFSA contributions shifts future investment growth into a tax-free environment held by the spouse, with no attribution back to the giver.

💡 Tip: This is an ideal strategy for single-income households where the non-earning spouse has unused TFSA contribution room but no funds to utilize it.

Prescribed-Rate Spousal Loan

This is a legal and easy way to split income for couples where one partner earns more than the other, or even when the other partner does not earn any income.

How it works

- The high-income spouse lends money to the low-income spouse at the CRA’s fixed prescribed interest rate. (The current rate, as of December 2025, is 3%.) The high-income spouse can also lend money to the non-earner spouse.

- The loan must take the form of a formal written agreement — typically a demand promissory note. This note must specify the lender, borrower, principal amount, and an interest rate that must be equal to or more than the CRA’s prescribed rate on the date it is signed.

- The lower-income spouse (borrower) invests the loaned money.

- All investment income (interest, dividends, and capital gains) generated from these investments is taxed in the lower-income spouse’s hands, and they can deduct the interest expense paid on the loan for income tax purposes, effectively reducing their taxable income.

- The borrower must pay the interest on the loan by January 30th of the following year. (E.g., interest for a 2025 loan must be paid by January 30th, 2026).

- The lender must report the interest received on their income tax return.

- Crucial Rule: If the borrower fails to pay the interest by January 30th, all subsequent income and capital gains on that investment will be permanently attributed back to the lender (high-income spouse), nullifying the tax benefit.

This may seem to be a bit confusing. Let’s walk through a simple example.

Example: John and Sara

A couple, John and Sara live in Ontario. John earns an annual income of $90,000 per year, and Sara, who takes care of the home and children, does not work and earns no income.

- At $90,000 annual income, John’s marginal tax rate is about 29.65% as per 2025 tax rates. This means that, if John earns an additional $1,000 income, he would pay tax at 29.65%, i.e. $296.50 tax on $1,000.

- Since Sara earns no income, her marginal tax rate is effectively 0% up to the basic personal amount. Therefore, it makes perfect sense to generate extra investment income in Sara’s hands.

- John has already used all the contribution rooms available for his RRSP and TFSA accounts.

- John has $20,000 sitting in his chequing account. Instead of investing that $20,000 in his non-registered account, he decides to loan $20,000 to Sara to enable her to invest in a non-registered account.

- They sign a demand promissory note, which states that John is lending Sara $20,000 at the CRA’s prescribed 3% annual interest rate. This note does not need to be notarized or bear a lawyer’s stamp to be legally valid or effective.

- To create a proper transaction trail, John transfers $20,000 from his separate individual account to Sara’s individual bank account.

- Sara invests that money. All investment income generated will be taxed in Sara’s name, as long as she pays the accrued interest by January 30th of the next year.

- To maintain a clear paper trail, Sara pays the interest from her own individual bank account to John’s individual bank account. John must report this interest as income on his tax return.

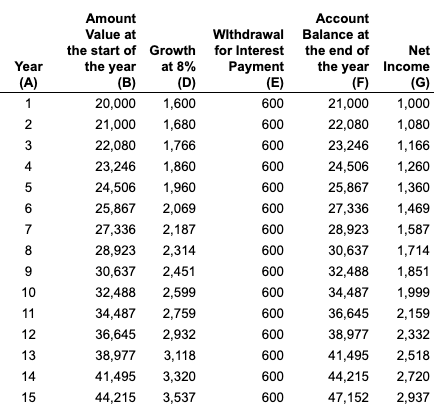

Sara invests the money in stock ETFs in a non-registered account that generates an 8% return. On the $20,000 loan, Sara pays $600 in interest payments (3% of $20,000) to John for the entire year. Let us assume that this arrangement continues for 15 years. The following table illustrates Sara’s Investment Account details.

- Column B contains the account value at the start of the year. It starts at $20,000, the loan value.

- Column C contains the growth of the account at 8%, i.e. B x 0.08

- Column D is the interest payable at 3% of $20,000, i.e. $600. This remains fixed during the entire duration of the loan.

- Column E displays the year-end account value after paying the $600 interest, i.e. C + D — E

- Column F displays Sara’s net income for the year, i.e. D — E

Sara will need to include Net Income from column F in her tax return.

- Sara’s investment account grows at 8%, but she pays $600 (3%) in deductible interest. Her net income from the investment is 5% ($1,600 growth — $600 interest deduction = $1,000 net income in year 1).

- Since Sara has no other income, and her net investment income is well within the basic personal amount ($16,129 for 2025), she pays no tax.

- John pays tax on the $600 interest income at his marginal rate (29.65%), which works out to be about $177 every year or about $2,655 over 15 years.

- At the end of 15 years, Sara’s investment account value is $47,152. She liquidates $20,000 worth of the investments and pays back the entire loan amount.

- After paying back the loan, her investment account value is $27,152, which can continue to grow with no link to John’s tax return.

Thus, at the cost of $2,655 in tax over 15 years, John has effectively shifted $27,152 into Sara’s hands — completely within CRA rules.

In essence, this strategy successfully converts highly taxed income (taxed at John’s 29.65% rate) into growth that is either tax-free or taxed at Sara’s low rate. The prescribed-rate spousal loan is one of the most powerful and effective methods available to Canadian families for long-term tax minimization and family wealth creation.

Key Considerations for the Prescribed-Rate Loan

- Net Return Requirement: For the strategy to work, the lower-income spouse’s investments must earn a return higher than the loan’s prescribed interest rate. If the return equals the prescribed rate, the net income benefit disappears.

- Fixed Interest Rate Advantage: The prescribed rate agreed upon in the promissory note is fixed for the entire duration of that specific loan, regardless of any future changes to the CRA’s quarterly prescribed rate. This feature allows for powerful long-term planning when rates are low.

- Multiple Loans are Permitted: The high-earning spouse is permitted to make multiple, separate loans to the low-earning spouse over time. Each loan, however, must be established at the prescribed rate applicable on the day that the specific loan is executed.

- Consequence of Missed Interest Payment: If the low-earning spouse fails to make the interest payment by January 30th of the following year, the strategy is compromised. All subsequent income and capital gains from that investment will be permanently attributed back to the high-income spouse. If this occurs, the most conservative approach is to repay the original loan immediately and, if desired, enter into an entirely new loan agreement at the current prescribed rate.

Using Household Cash-Flow to Shift Savings to the Low-Earning Spouse

In addition to gifting money for TFSA contributions or using a prescribed-rate spousal loan, couples can also take advantage of a simple and completely legal cash-flow strategy:

The high-earning spouse pays most or all household expenses, while the low-earning spouse invests as much of their own income as possible.

This works because attribution rules do not apply to income earned from a person’s own savings or salary. When the low-income spouse invests their money:

- The investment income is taxed at their lower marginal rate,

- There is no attribution to the higher-income spouse, and

- The couple effectively shifts more investment growth into the hands of the lower-taxed spouse.

This approach is particularly effective when:

- The low-earning spouse earns some income, but not enough to contribute meaningfully after covering household bills.

- The high-earning spouse has surplus cash flow and is already maximizing their own tax-advantaged accounts.

- The couple wants to reduce overall family taxes without loans, formal structures, or CRA reporting.

By structuring family finances this way — high-earner covers spending, low-earner invests — the couple achieves a gradual, natural form of income splitting that is fully compliant with Canadian tax rules.

Final Thoughts: Taking Control of Your Family’s Taxes 💰

Income splitting isn’t about avoiding taxes — it’s about using the rules the CRA already provides to reduce your family’s overall tax burden. By proactively structuring your savings and investments, you can achieve significant, long-term wealth creation.

The three compliant strategies covered here — TFSA Gifting, the Prescribed-Rate Spousal Loan, and Strategic Cash-Flow Allocation — offer different levels of complexity and compliance requirements.

Note: In addition to the strategies covered in this article, options like Spousal RRSPs and pension income splitting can also help reduce a couple’s overall tax burden. You can learn more in the related articles: Spousal RRSP for Income Splitting and Pension Income Splitting.

Disclaimer: This article is for educational purposes only and is not financial or tax advice. Please consult a qualified tax or financial professional before making any decisions.

What are your thoughts on this post? Share your comments with us.

Stay ahead of the curve. Subscribe here to get notified whenever I publish a new guide or tool.

Share your comment or feedback. We'll get back to you as soon as we can.