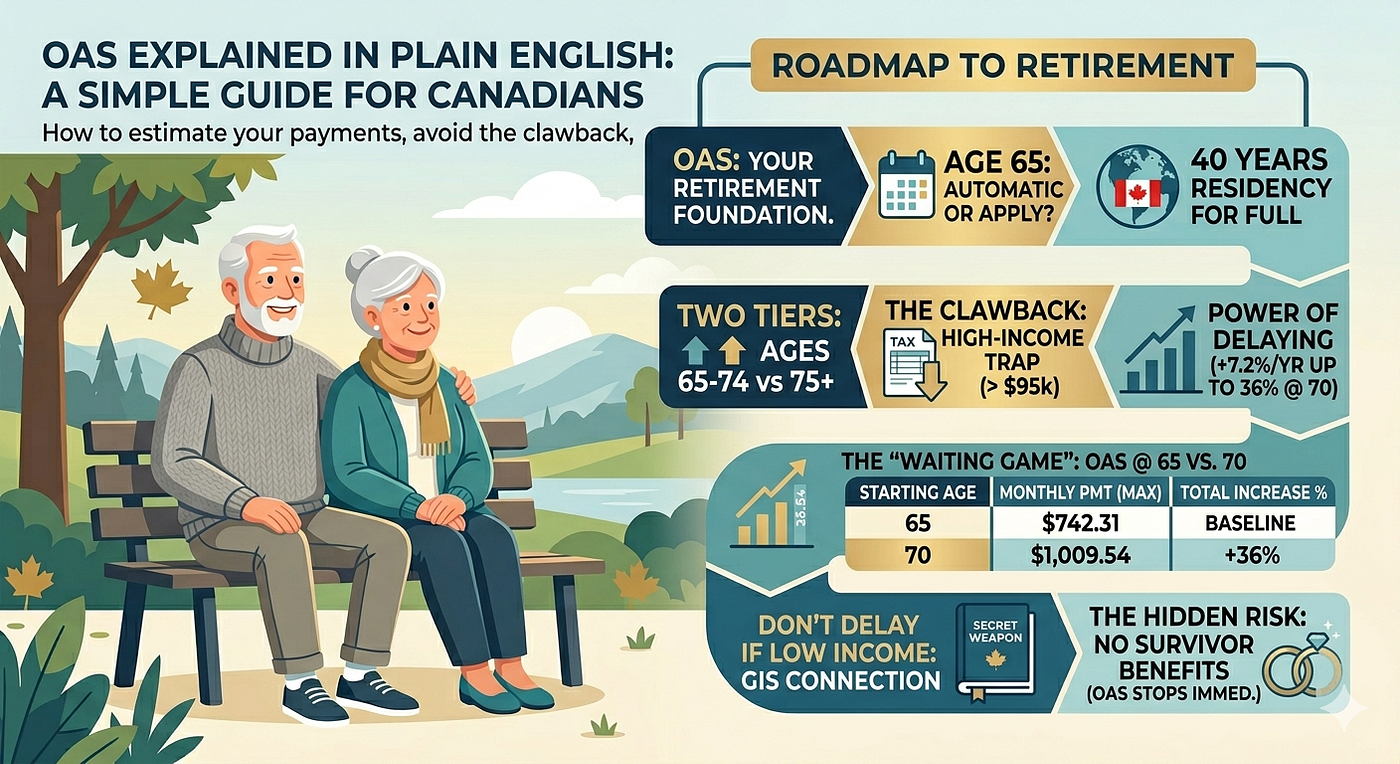

OAS Explained in Plain English: A Simple Guide for Canadians

How to estimate your payments, avoid the clawback, and decide when to start.

When it comes to retirement in Canada, the federal government provides two main pillars of income support: the Canada Pension Plan (CPP) and Old Age Security (OAS). Together, they form the financial foundation of retirement income for millions of seniors. However, they work very differently.

The Canada Pension Plan is a contributory program — meaning your benefit depends on how much you worked and how much you contributed to the system over your lifetime.

Old Age Security, on the other hand, is a residency-based pension. It is a monthly payment available to most Canadians aged 65 and older, regardless of whether you ever worked or even if you’re still working today.

On the surface, OAS seems simple: you turn 65 and start receiving payments. But beneath that simplicity, there are important details — residency requirements, age-based increases, and a “clawback” that can reduce your benefits if your income is too high.

Let’s break it all down so you can make the most of this important retirement foundation.

1. Who Is Eligible for OAS?

To qualify for Old Age Security, you don’t need a work history — but you do need to meet residency requirements.

At a high level, you must meet three basic requirements:

- Be 65 or older

- Be a Canadian citizen or legal resident

- Have lived in Canada for at least 10 years after age 18

Full vs Partial OAS

- 40 years of residency after age 18 → Full OAS pension

- 10 to 39 years → Partial OAS pension

As of early 2026, the maximum OAS pension (age 65–74) is $742.31 per month.

If you haven’t lived in Canada for the full 40 years, your pension is reduced proportionally.

Example: How Partial OAS Works

OAS is calculated on a simple pro-rata basis:

- 10 years of residency → 10/40 = 25%

→ $742.31 × 25% = $185.58/month - 20 years of residency → 20/40 = 50%

→ $742.31 × 50% = $371.16/month - 30 years of residency → 30/40 = 75%

→ $742.31 × 75% = $556.73/month

👉 In simple terms, each year you live in Canada after age 18 adds 1/40 (2.5%) of the full OAS pension.

Important: Once your OAS starts, your “partial” percentage is locked in. It does not increase later just because you continue living in Canada.

Good news: Your OAS payments are adjusted regularly for inflation, so the dollar amount you receive will increase over time to help keep up with the cost of living.

How OAS Residency Years Are Counted

When we say you need 40 years of residency after age 18 for full OAS, it does not mean you must be physically in Canada every single day of those 40 years.

You can travel or spend part of the year outside Canada and still have that year count toward OAS residency, as long as Canada remains your primary place of residence.

In general:

- Short trips and vacations outside Canada do not affect your OAS residency years.

- Even if you spend several months a year outside Canada (for example, wintering in another country), that year may still count toward OAS, depending on your residency status.

- The government looks at where you normally live, not just how many days you were physically present in Canada.

2. The Two Tiers of OAS (2026 Rates)

As of early 2026, OAS is divided into two age-based categories to provide additional support to older seniors as living costs rise.

- Ages 65 to 74: The maximum monthly payment is $742.31.

- Ages 75 and older: You receive an automatic 10% increase, bringing the maximum monthly payment to $816.54.

The government reviews these amounts every three months — in January, April, July, and October — to keep up with inflation, as measured by the Consumer Price Index (CPI).

In simple terms, if the cost of living goes up, your OAS payments are adjusted so that your purchasing power does not fall behind.

3. The “Clawback”: The High-Income Trap

OAS is designed to provide a basic level of income for seniors, but if your income is considered too high, the government will require you to repay part (or all) of your OAS. This is officially called the OAS Pension Recovery Tax, but most people simply call it the OAS clawback.

The 2026 Threshold

For the 2026 tax year, the clawback starts when your net income exceeds $95,323.

The 15% Rule

Once your income is above this threshold, you must repay 15 cents of OAS for every $1 of income above $95,323.

Example:

If your income is $105,323, that is $10,000 above the threshold, you would repay 15% × $10,000 = $1,500 of your OAS.

The Full Cutoff

If your income becomes high enough, your OAS will be completely clawed back. As of March 2026, the approximate income at which OAS is fully eliminated is:

- Ages 65–74: Around $155,000

- Ages 75+: Around $160,000+ (because the OAS pension is higher)

The exact number changes slightly every year because OAS payments and thresholds are indexed to inflation.

💡 Pro-Tips to Avoid the Trap:

- Pension Income Splitting: If you are married or in a common-law relationship, you may be able to “split” up to 50% of your eligible pension income (like RRIF or private pension payments) on your tax return. This can lower the higher earner’s net income, potentially keeping them below the OAS clawback threshold.

For a step-by-step look at how this works, see my article: Pension Income Splitting. - CPP Pension Sharing: Unlike the tax-time splitting mentioned above, you can apply to Service Canada to “share” your CPP retirement pension with your spouse. If one spouse has a very high CPP and the other has very little, sharing can move that income to the lower earner, helping the higher earner stay under the OAS clawback limit.

- The “RRSP/RRIF Meltdown”: Large mandatory RRIF withdrawals after age 71 often spike your income right into the clawback zone. Some retirees choose to start withdrawing from their RRSP/RRIF before they start their OAS. By “melting down” these accounts early, you reduce the size of the future mandatory payments, protecting your OAS checks later in life.

Learn more about this strategy here: RRSP Meltdown Explained: A Plain English Guide for Canadian Retirees.

4. Should You Delay Until Age 70?

You can start OAS as soon as you turn 65, but you are not required to. If you do not need the income immediately, you can delay your start date up to age 70 in exchange for a guaranteed increase in your payments.

It is important to know that this isn’t an “all-or-nothing” choice. You can choose to delay by a few months, a single year, or the full five years.

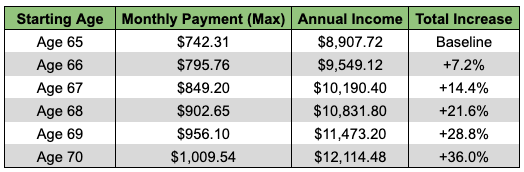

- The Bonus: For every month you delay, your payment increases by 0.6%. That works out to a 7.2% increase per year.

- The Total: If you wait the full five years until age 70, your monthly OAS payment will be 36% higher for the rest of your life.

- The “Break-Even” Point: This is the most common question: “Is it worth missing five years of cheques?” If you take OAS at 65, you get a head start. If you wait until 70, you start at zero, but with a much larger monthly payment. Mathematically, the break-even point is usually around age 82.

The Simple Rule: If you are in good health and your family history suggests you’ll live well into your 80s or 90s, delaying is a powerful way to protect yourself against “longevity risk” (the risk of outliving your money).

The “Waiting Game”: OAS at 65 vs. 70

Note: These calculations are based on the current 2026 baseline. In reality, the “Age 70” amount will likely be even higher because the base amount is adjusted for inflation every three months.

5. When Delaying is a MISTAKE

While the 36% “bonus” for waiting until age 70 sounds tempting, there is one major exception where delaying is a costly mistake: The GIS Connection.

If you are a low-income senior, you may be eligible for the Guaranteed Income Supplement (GIS). This is a monthly non-taxable benefit designed to help those with little income beyond their OAS.

Here is the catch: You cannot receive the GIS unless you are already receiving OAS. Delaying OAS also delays GIS.

If you delay your OAS until age 70, you are also delaying your GIS for five years. For many seniors, the combined value of the OAS and GIS payments starting at age 65 far outweighs the “bonus” they would get by waiting. By the time the higher age-70 payments “catch up,” you might have left tens of thousands of dollars on the table that you could have used earlier in retirement.

Pro-Tip: If you think you might qualify for low-income support, I highly recommend reading my previous deep-dive: GIS: The Secret Weapon for Low-Income Retirement in Canada. It explains the specific income thresholds and how to ensure you don’t miss out on this “secret” benefit.

6. How to Apply (Don’t Assume It’s Automatic!)

One of the most common misconceptions about OAS is that the government “just knows” when to start paying you. While many are enrolled automatically, it isn’t true for everyone.

- The Automatic Path: If Service Canada has enough information about your history, they will automatically enroll you. You should receive a letter in the mail the month after you turn 64 telling you that you’re all set.

- The Manual Path: If you haven’t received that letter by the time you are 64 and a half, you likely need to apply manually. This often happens if you’ve lived outside of Canada for a period of time or if Service Canada is missing certain records.

- Retroactive Payments: If you are already 65 and realized you never applied, you can request “back-payments” for up to 11 months from the date Service Canada receives your application.

Crucial Note on Delaying: If you receive an automatic enrollment letter but you have decided to delay your OAS to get the higher payments mentioned in Section 4, you must contact Service Canada immediately to “opt-out.” If you don’t, the payments will start automatically at 65, and you will lose the ability to earn that 7.2% annual increase.

For more details on how to apply for OAS (and GIS, if applicable), refer to my article: GIS: The Secret Weapon for Low-Income Retirement in Canada.

7. The Hidden Risk: What Happens When a Spouse Passes Away?

When we plan for retirement as a couple, we tend to look at our “household income” — the total of two CPPs and two OAS payments. However, there is a critical difference in how these two pillars handle the death of a spouse.

- OAS has NO Survivor Benefits: This is the part that catches many people off guard. OAS stops immediately upon death. While there is a temporary ‘Allowance’ for low-income survivors aged 60–64, there is no permanent ‘OAS Survivor Pension’ once you are over 65.

- CPP has Survivor Benefits: If your spouse passes away, you may be eligible for a CPP Survivor’s Pension. While it isn’t the full amount (it’s usually 36% to 60% of their pension, capped at a certain maximum), it provides some continued support.

The “Survivor’s Income Gap”

If a couple is receiving two maximum OAS cheques (~$1,484 per month combined in 2026), that income is instantly cut in half to $742.31 the moment one spouse dies.

When you combine the total loss of one OAS payment with the reduced survivor portion of the CPP, a surviving spouse can see their monthly government income drop by $1,000 to $1,500 or more.

Strategy Tip: If your retirement plan relies heavily on these two pillars, it is essential to have a “Survivor Scenario” in place. This might mean having a larger TFSA cushion or ensuring your life insurance or private pensions (RRIF) are set up to bridge this specific gap.

8. Conclusion: Your Personal Retirement Roadmap

Old Age Security is often called a “pension,” but in reality, it is a residency-based social safety net. While it seems like a straightforward monthly cheque, the decisions you make around it — when to start, how to manage your other income to avoid the clawback, and how to protect a surviving spouse — can have a major impact on your quality of life in your 70s, 80s, and beyond.

There is no “one-size-fits-all” answer. If you are in excellent health and have other savings to live on, delaying OAS to age 70 is one of the best “guaranteed returns” you will ever find. On the other hand, if your income is lower, taking OAS at 65 to unlock the GIS “secret weapon” is almost always the smarter move.

Final Checklist for your OAS Strategy:

- Verify your residency: Ensure you know if you qualify for a full or partial pension.

- Watch the threshold: If your income is near $95,000, plan your RRIF or investment withdrawals carefully.

- Check your mailbox: If you are 64 and haven’t received an enrollment letter, contact Service Canada.

- Plan for the “Gap”: Ensure your surviving spouse has a financial cushion for the day those two OAS payments become one.

Retirement planning isn’t just about how much you save — it’s about how well you understand the rules of the road. By mastering the pillars of OAS and CPP, you can build a retirement foundation that is both stable and secure.

Disclaimer: This article is for educational purposes only and is not financial or tax advice. Please consult a qualified tax or financial professional before making any decisions.

What are your thoughts on this post? Share your comments with us.

Stay ahead of the curve. Subscribe here to get notified whenever I publish a new guide or tool.

Share your comment or feedback. We'll get back to you as soon as we can.