CPP Explained in Plain English: The 2026 Guide to Maximizing Your Pension

Everything you need to know about the new CPP2 limits, the “Age 70” strategy, and why the Canada Pension Plan isn’t a black box.

If you’ve lived and worked in Canada, you’ve probably seen “CPP” deducted from your paycheque for years. But for many Canadians, the Canada Pension Plan (CPP) remains a black box. Similar to my guides on the RRSP, TFSA, and RRIF, this article explains CPP in plain language so you can better plan your retirement.

1. What is the CPP?

The Canada Pension Plan (CPP) is a contributory public pension program. It is not a welfare program — it is a defined-benefit pension plan. You receive a monthly payment for life based on your contribution history and your average pensionable earnings during your working career.

The more you earn (up to yearly limits) and the longer you contribute, the larger your pension will be. CPP payments are also indexed to inflation, meaning they increase over time to help preserve purchasing power.

2. The Rules of Contribution

By law, most people working in Canada between the ages of 18 and 70 who earn more than $3,500 per year must contribute to CPP.

The Two-Tier System (The CPP Enhancement)

Since 2019, the CPP has been gradually enhanced to provide higher retirement benefits for future retirees.

Tier 1 (Base CPP)

5.95% on earnings between $3,500 and $74,600, known as the Year’s Maximum Pensionable Earnings (YMPE). (The first $3,500 you earn is a “Basic Exemption” where no CPP is deducted).

Tier 2 (CPP2)

An additional 4% contribution on earnings between $74,600 and $85,000, up to the Year’s Additional Maximum Pensionable Earnings (YAMPE). Note that the $3,500 exemption does not apply to this second tier; you pay the 4% on the full $10,400 gap.

The Employee vs. The Self-Employed

If you are an employee, you pay half of the required contribution, and your employer pays the other half.

If you are self-employed, you must pay both portions — the employee and employer shares. This is calculated when you file your annual income tax return.

2026 Maximum Contributions

For those earning $85,000 or more, the total maximum contributions are:

- Employee: $4,646.45 (comprising $4,230.45 Base CPP + $416.00 CPP2

- Self-Employed: $9,292.90 (comprising $8,460.90 Base CPP + $832.00 CPP2)

The Future Payoff: Moving from 25% to 33%

This enhancement represents a fundamental shift in the CPP’s role in your retirement.

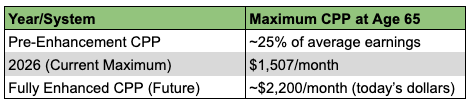

- The Original System (Pre-2019): For decades, the “Base CPP” was designed to replace only 25% of your average work earnings. The government’s philosophy was that the CPP should only be a modest foundation, leaving you to cover the remaining 75% through RRSPs and workplace pensions.

- The Enhanced System: For every year you work after 2019, your contributions are building toward a 33.33% replacement rate.

Expected Maximum CPP Under the Enhanced System

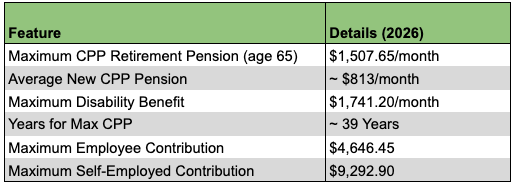

Today (2026), the maximum CPP retirement pension at age 65 is $1,507.65 per month. However, this amount still mostly reflects the old CPP system, because the CPP enhancement only began in 2019. Workers retiring today have contributed under the enhanced rules for only a few years, so they receive only a small portion of the additional benefit.

When the enhanced CPP fully matures — after workers contribute at the higher rates for roughly 40 years — the maximum pension will be significantly larger.

A worker consistently earning at or above the YAMPE throughout their career could receive roughly $2,200 per month (in today’s dollars) at age 65. Because CPP benefits are indexed to inflation, the actual dollar amount future retirees receive will likely be higher.

3. CPP for International Students & Temporary Workers

A common myth is that CPP only applies to Canadian citizens or permanent residents. In reality, CPP applies to most people working in Canada, regardless of immigration status.

Mandatory Contributions

If you are an international student or temporary worker earning more than $3,500 per year, CPP contributions are mandatory, just like for Canadian workers.

It’s Not a Lost Tax

Even one valid year of contribution can establish eligibility. If you leave Canada, you can still receive your pension starting at age 60 while living abroad.

Social Security Agreements

Canada has agreements with 50+ countries (including the US, UK, and India) to help you combine contribution periods and qualify for benefits.

4. When Should I Start? (The 10-Year Window)

You can start your CPP anytime between age 60 and 70. It is important to remember that this is a choice, not an automatic event. You do not have to stop working to start your pension, and you don’t have to start your pension just because you’ve retired.

This 10-year window is essentially a “sliding scale” where the government rewards you for waiting or reduces your CPP payment for starting early to account for the extra years of payouts.

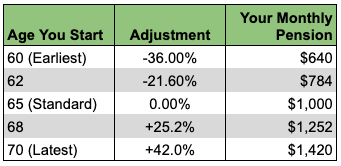

- Standard (Age 65): The “baseline.” You receive 100% of your earned benefit.

- Early (Age 60–64): Your pension is reduced by 0.6% per month (7.2% per year). Starting at 60 results in a permanent 36% reduction compared to age 65. This is often chosen by those with immediate cash flow needs or a shorter life expectancy.

- Late (Age 66–70): Your pension increases 0.7% per month (8.4% per year). Waiting until 70 increases your pension by 42% compared to starting at 65.

The Impact of Timing: A $1,000 Example

To see how this works in real dollars, let’s assume your “earned” CPP benefit (the amount you would get at exactly age 65) is $1,000 per month. Here is how that monthly check changes depending on when you click “start”:

Working While Receiving CPP

- Age 60 to 65: You must continue contributing. These contributions go toward a Post-Retirement Benefit (PRB), which increases your monthly pension the following year.

- Age 65 to 70: Contributions become optional. You can keep contributing to build your PRB or opt out using Form CPT30 to increase your immediate take-home pay.

5. The Strategy: Why Many Experts Now Recommend Age 70

While “taking it early” used to be the norm, many retirement experts now suggest delaying CPP to age 70 if your health and finances allow. Here is why:

- A Guaranteed 8.4% “Return”: It is virtually impossible to find a government-backed, inflation-indexed return of 8.4% per year in the private market.

- Longevity Insurance: A larger CPP payment acts as a safety net if you live into your 90s, ensuring you never outlive your guaranteed income.

- The “RRSP Meltdown” Window: Delaying CPP allows you to withdraw from your RRSP/RRIF at lower tax rates between retirement and age 70.

Note: Read my dedicated guide: RRSP Meltdown Explained: A Plain English Guide for Canadian Retirees.

6. Protecting Your Pension: The Drop-Out Rules

To avoid penalizing you for years with little to no income, CPP includes:

- General Drop-Out: Automatically removes your lowest 17% of earning months (roughly 8 years).

- Child-Rearing Provision (CRP): Excludes months where your income was lower while caring for a child under age 7. You must request this when you apply for CPP.

- Disability Drop-Out: Excludes months you received CPP Disability benefits.

7. CPP for Immigrants Who Move to Canada Mid-Career

If you move to Canada at age 40, you will initially have many “zero-earning” years (from age 18 to 40) in your calculation.

- The Impact: After the 8-year drop-out, several zero-earning years remain, which reduces the average.

- The Strategy: Delaying to 70 is especially effective for mid-career immigrants, as it provides more time to contribute and a 42% bonus to help offset those earlier zero-earning years.

8. More Than Just Retirement: The Disability Benefit

CPP also includes a disability insurance program. If you develop a severe and prolonged disability that prevents you from working any job, you may qualify for the CPP Disability Benefit.

Basic Requirement

You usually must have contributed to CPP for at least 4 of the last 6 years or for at least 25 years, including 3 of the last 6 years

2026 Maximum Disability Benefit

Up to $1,741.20 per month.

At age 65, the disability benefit automatically converts into a regular CPP retirement pension.

9. Survivor Benefits: What Happens to Your Pension?

The CPP provides a monthly payment to the legal spouse or common-law partner of a deceased contributor. However, the calculation changes significantly depending on your age and whether you are already receiving your own CPP.

Part A: The Basic Calculation (If you have NO pension of your own)

If you are not yet collecting your own CPP retirement pension, your survivor benefit is calculated using these standard 2026 rates:

- If you are 65 or older: You receive 60% of the deceased’s retirement pension.

- If you are under 65: You receive a flat-rate portion ($238.17 in 2026) plus 37.5% of the deceased’s retirement pension.

Part B: The “Combined Benefit” Reality (The Stacking Rule)

If you are already receiving your own CPP retirement pension, you cannot simply add the survivor benefit on top. The math becomes much more restrictive:

- The 40% Reduction: When combining benefits, the survivor portion is reduced by 40%. Effectively, you only receive about 36% of what your spouse was receiving.

- The Hard Cap: The total of your own pension plus the survivor portion cannot exceed the maximum retirement pension for that year. In 2026, the absolute maximum combined payment is $1,531.56 per month.

Note on Payments: If you are eligible for both benefits, Service Canada will merge them into one single monthly payment. You will not see two separate deposits in your bank account.

Example 1: The “36% Reality” (Staying Under the Cap)

- You: Receive $800/month.

- Your Partner: Receives $800/month.

- The Math: Instead of getting 60% ($480), your survivor portion is reduced by 40%. You receive $288.

- New Total Check: $1,088 ($800 + $288).

Example 2: The “Hard Ceiling” (Hitting the Cap)

- You: Receive $1,200/month.

- Your Partner: Receives $1,200/month.

- The Math: 60% of their pension is $720. Apply the 40% reduction, and you qualify for $432.

- The Result: $1,200 + $432 = $1,632.

- Reality: Since this exceeds the 2026 limit, you are capped. You receive only $1,531.56.

Children’s Benefit

If the deceased had dependent children (under age 18, or age 18–25 in full-time school), they may receive a flat-rate monthly benefit of $307.81 (2026 rate).

What Happens if a Single Contributor Dies?

For those who are single, widowed, or divorced with no dependent children, the rules are very different. It is a common misconception that your CPP contributions sit in a personal “pot” that your heirs can inherit.

1. The Money Does Not “Go Back” to the Family

Unlike an RRSP or a bank account, you cannot name a beneficiary to inherit your CPP. If there is no legal spouse, common-law partner, or dependent child, the monthly pension simply stops. Your contributions remain in the general fund to support other Canadians.

2. The $5,000 Death Benefit (New for 2026)

The estate is eligible for a one-time, taxable lump-sum payment:

- The Standard Amount: $2,500.

- The “No-Survivor” Top-Up: If you die on or after January 1, 2025, and have never collected a single CPP payment (retirement or disability), your estate gets an extra $2,500.

- The Total: Up to $5,000 as a one-time payment.

3. Does the Age Matter?

Timing is everything. If you wait until 70 to “click the button” but die at 69, your estate receives no back-payments or monthly benefits — only the lump-sum death benefit.

⚠️ The “Single Contributor” Warning: Because of these “use-it-or-lose-it” rules, the Age 70 Strategy is a high-stakes gamble for single people. This makes the Break-Even Analysis in Section 12 even more critical for your planning.

10. CPP Pension Sharing: A Simple Way to Lower Your Taxes

If you are married or in a common-law relationship, and both of you are at least 60 years old, you can apply to share your Canada Pension Plan (CPP) retirement pensions. This is a powerful tax-planning tool that many couples overlook. It allows you to shift a portion of the higher-income spouse’s CPP to the lower-income spouse, potentially reducing your overall household tax bill.

How It Works

It’s not a 50/50 split: You can only share the portion of the CPP pension earned during the years you lived together, not the entire pension.

Eligibility: You must be living with your legal spouse or common-law partner, and at least one of you must be receiving (or have applied for) a CPP retirement pension. Both partners must be at least 60 years old.

The Tax Benefit: If one spouse is in a higher tax bracket and the other is in a lower bracket, shifting some CPP income to the lower-income spouse means less tax paid overall and more after-tax income for the household.

Example:

Assume one spouse receives $1,400 per month from CPP and the other receives $400 per month. If the couple has lived together for most of their adult lives, CPP pension sharing will roughly equalize their pensions.

- Total CPP = $1,800 per month

- After sharing ≈ $900 per month each

- Amount shifted from higher-income spouse to lower-income spouse = $500 per month

This income shifting can meaningfully reduce taxes, especially when the higher-income spouse is in a higher marginal tax bracket.

Important: Don’t Confuse “Pension Sharing” with “Pension Splitting”

While they sound the same, these are two different tools managed by two different government bodies.

💡 Related Guide: If you have a RRIF or a workplace pension, you should also read my detailed guide: Pension Income Splitting.

11. Common CPP Myths

Myth #1: Everyone receives the maximum CPP

In reality, most Canadians receive much less because they did not earn the maximum pensionable earnings throughout their careers. While the maximum CPP payment for new retirees at age 65 is $1,507.65 per month, the average CPP payment for new retirement beneficiaries (at age 65) is approximately $803.76 per month.

Myth #2: CPP will run out of money

According to the Chief Actuary of Canada, the CPP fund is projected to remain financially sustainable for at least the next 75 years.

Myth #3: Starting CPP early is always best

Starting early permanently reduces your pension. For many retirees, delaying CPP provides a higher guaranteed lifetime income, and it may also help you keep more of income-tested benefits like Guaranteed Income Supplement (GIS) and Old Age Security (OAS).

12. Three Costly CPP Mistakes Canadians Make

1. Starting CPP Without Considering Longevity

If you live into your late 80s or 90s, delaying CPP can significantly increase your total lifetime income.

2. Ignoring Drop-Out Provisions

Many Canadians fail to apply for the Child-Rearing Provision, which can increase their pension.

3. Never Checking Their Contribution Record

Errors occasionally occur in earnings records.

Reviewing your Statement of Contributions ensures your pension is calculated correctly.

13. The CPP Break-Even Insight

Many retirees ask: “At what age does delaying my CPP actually pay off?” If you compare the total dollars received from starting at age 65 versus age 70, the “break-even” point is roughly age 81 to 82.

- If you die before age 81: You would have collected more total cash by starting at 65.

- If you live past age 82: You will receive significantly more total lifetime income by delaying to 70.

The Strategy Note

While the math points to age 82, the real reason to delay isn’t to “win” the break-even game — it is longevity insurance. Most Canadians underestimate their life expectancy. For a healthy 65-year-old couple today, there is a very high probability that at least one spouse will live into their 90s. Delaying CPP ensures that your “oldest self” has the largest possible inflation-protected check arriving every month, long after your other investments might be depleted. For single people, this ‘break-even’ math is even more critical because there is no survivor pension to provide a safety net for a loved one if you die early. For you, CPP is truly ‘use it or lose it.’

14. How to Apply: The My Service Canada Account (MSCA)

Once you have decided on your start date, you must officially apply to begin receiving your pension. CPP benefits do not start automatically. The fastest way to apply is via your My Service Canada Account (MSCA) online.

- Processing: Online applications take 7–14 days; paper applications can take 4 months.

- Timing: Apply up to 12 months in advance (experts suggest 6 months).

The “Age 70” Deadline: Don’t Leave Money on the Table

While you can choose to start your CPP anytime between 60 and 70, there is no financial benefit to waiting past your 70th birthday. The “delay bonus” stops at 42%, and your pension amount will not increase further.

The 12-Month Retroactive Limit

If you are already over age 65 and have not yet started your pension, Service Canada can offer retroactive payments. When you apply, they can pay you a lump sum for up to 11 months of back-payments (plus the month you apply).

However, this is where the age-70 deadline becomes critical:

- Applying at Age 71: If you forgot to apply at 70 and wait until age 71, you can use the 12-month retroactivity rule to recover all the payments you missed since your 70th birthday.

- Applying at Age 72 or Later: If you wait until age 72, you can still only go back 12 months. This means you would permanently lose one full year of pension payments that can never be recovered.

Strategy Tip: Even if you do not need the cash at age 70, it is still wise to apply. You can always invest the monthly payments in a TFSA or a non-registered account, allowing the funds to continue growing.

15. Final Thought

Don’t guess. Log in to your My Service Canada Account (MSCA) and review your Statement of Contributions. It shows your complete earnings record and provides an estimate of the CPP pension you may receive. Understanding your CPP now allows you to coordinate it with your RRSP and RRIF withdrawals for a much more tax-efficient retirement.

Take the Quiz: Think you’ve mastered the CPP rules? Test yourself here: CPP Knowledge Check.

You may also like: The Hidden Opportunity Cost of CPP: A 24-Year Case Study of Investing vs. Pension Contributions

Disclaimer: This article is for educational purposes only and is not financial or tax advice. Please consult a qualified tax or financial professional before making any decisions.

What are your thoughts on this post? Share your comments with us.

Stay ahead of the curve. Subscribe here to get notified whenever I publish a new guide or tool.

Share your comment or feedback. We'll get back to you as soon as we can.