RESP Explained in Plain English

Maximizing Grants, Front-Loading Strategies, and the Tax-Efficient Exit

When navigating the Canadian wealth roadmap, most conversations naturally focus on the RRSP, the TFSA, or the newer FHSA. Canadians spend a great deal of time planning for retirement, lowering taxes, or saving for a first home — either for themselves or eventually for their children.

Yet one registered account is frequently misunderstood, underutilized, or poorly managed: the Registered Education Savings Plan (RESP).

That is unfortunate because the RESP combines three powerful benefits: government grants, tax-sheltered growth, and exceptional flexibility. Yet many families fail to take full advantage of what it offers.

Many people view the RESP simply as a “savings account for university.” In reality, it is far more powerful than that. Properly used, the RESP is a highly strategic wealth-building vehicle that combines an immediate, guaranteed 20% government grant with decades of tax-sheltered compounding.

For parents and grandparents looking to help fund a child’s future education without compromising their own retirement security, understanding how to optimize the RESP is critical. In this article, we will break down how the RESP works, explore advanced funding strategies, and explain how to withdraw the money in the most tax-efficient manner possible.

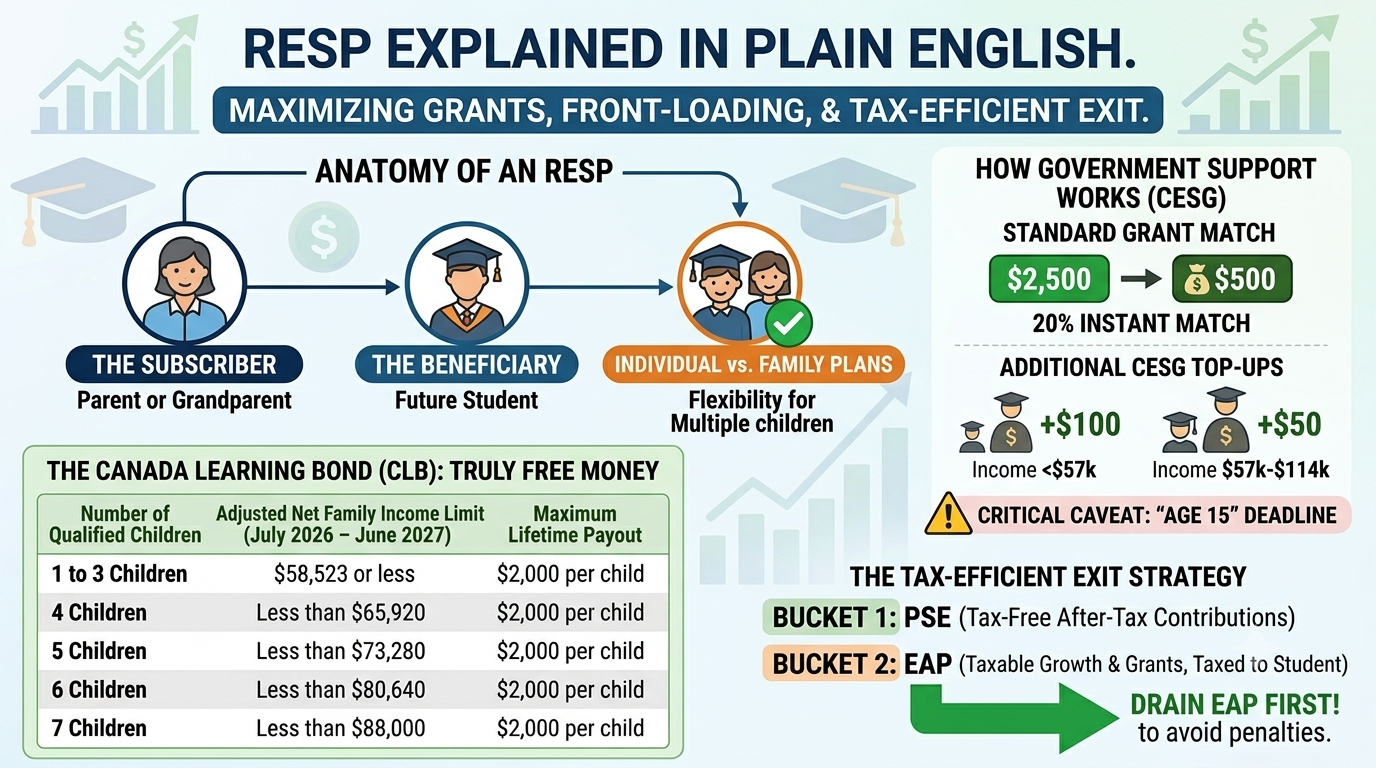

1. The Anatomy of an RESP: Understanding the Key Roles

Before contributing money to an RESP, it is important to understand the terminology. While the Canada Revenue Agency (CRA) uses specific legal labels, the overall structure is fairly simple.

The Subscriber

The subscriber is the person who opens and controls the RESP account and makes the contributions. In most cases, this is a parent or grandparent.

The Beneficiary

The beneficiary is the future student — typically a child or grandchild — who will eventually use the funds to help pay for post-secondary education.

Individual vs. Family Plans

An RESP can be set up as either an Individual Plan (with one beneficiary) or a Family Plan (with multiple beneficiaries).

For families with more than one child or grandchild, a Family Plan often provides greater flexibility. All beneficiaries must be related to the subscriber by blood or adoption, but the structure allows grants and investment growth to be shared among eligible beneficiaries.

This flexibility can be extremely valuable if one child is unable to pursue, or simply chooses not to pursue, post-secondary education, as the funds can often be redirected to a sibling without triggering penalties or the loss of government grants.

2. The Numbers Game: How the Government Support Works

One of the most compelling features of the RESP is the Canada Education Savings Grant (CESG). In simple terms, the federal government contributes additional funds to the account to help accelerate growth.

Note: Some income thresholds, grant limits, and withdrawal benchmarks discussed below are indexed periodically by the federal government. The figures shown reflect the rules in effect as of June 2026 and may change in future years.

CESG Eligibility: Who Qualifies?

Before looking at the numbers, it is important to know who can actually receive the grant money. To be eligible for the CESG, the child must meet the following criteria:

- Age Limit: Be 17 years old or younger. The grant is officially available up until the end of the calendar year in which the child turns 17.

- Residency: Be a resident of Canada at the time the contribution to the plan is made.

- Documentation: Have a valid Social Insurance Number (SIN).

- Plan Registration: Be formally named as a beneficiary in an active RESP.

Note: A personal contribution must actually be deposited into the RESP to trigger and receive the matching CESG.

The CESG: Matching Contributions

Once eligibility is established, the basic structure works as follows:

- Lifetime Contribution Limit: You can contribute up to $50,000 per beneficiary over the lifetime of an RESP. Contributions are flexible, as there is no strict annual contribution requirement.

- Standard Grant Match: When you contribute $2,500 in a year, the government adds $500 to the RESP through the CESG. This is a 20% matching grant, effectively providing an immediate 20% boost on your contribution before any investment growth occurs.

- Maximum Lifetime Grant: The total CESG available per child is capped at $7,200. To receive the full $7,200 of basic CESG, a family would typically contribute $2,500 annually for 14 years, followed by a final contribution to capture the remaining grant entitlement.

The Additional CESG: Extra Help for Lower- and Middle-Income Families

Families with lower or modest adjusted family net income may qualify for an enhanced CESG on the first $500 contributed each calendar year:

- Income of $58,523 or less: You receive an extra 20% match on that first $500, giving you an additional $100 per year. (Making your maximum annual CESG $600).

- Income between $58,523 and $117,045: You receive an extra 10% match on that first $500, giving you an additional $50 per year. (Making your maximum annual CESG $550).

Note: The lifetime total cap for all CESG grants remains $7,200 per beneficiary. However, these additional grants allow eligible families to reach the maximum grant entitlement with less personal contribution.

A Critical Caveat: The “Age 15” Deadline

To prevent people from opening an account at the very last minute just to grab a quick grant, the government stipulates that a child who is 16 or 17 can only get the CESG if they met one of these conditions before the end of the calendar year they turned 15:

- A total of at least $2,000 was contributed to (and not withdrawn from) their RESP, OR

- A minimum annual contribution of $100 was made in any four previous years.

Essentially, it means you must start saving in an RESP before the end of the year the child turns 15 if you want to claim any grants during their final high school years.

The Catch-Up Room Rule

If contributions were missed in earlier years, the unused grant room carries forward. This allows additional CESG room to be used in future years.

In any given calendar year, you can receive grants for both the current year and one additional prior unused year. This means that contributing $5,000 in a single year can generate up to $1,000 in grants ($500 for the current year and $500 for unused room from a prior year), subject to available eligibility.

This structure allows families who start late to gradually recover missed grant opportunities over time, but it does not allow all missed years to be recovered in a single contribution.

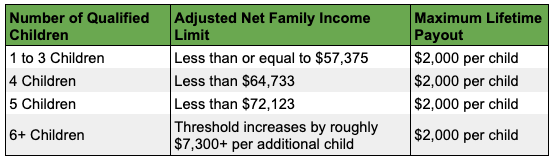

3. The Canada Learning Bond (CLB): Truly Free Money

While the CESG (basic and additional) requires you to deposit your own cash in an RESP, the Canada Learning Bond (CLB) requires $0 in personal contributions. This is one of the most underutilized federal programs designed specifically for low- and modest-income families.

For the period from July 2025 to June 2026, income eligibility for the CLB is as follows:

The government deposits money into the RESP account, provided the family meets the income criteria. For the current benefit period, if your adjusted family net income is $57,375 or less (for families with up to three children), the government deposits money into the RESP simply because the account exists.

- The Initial Kickstart: The government deposits $500 directly into the RESP the very first year the child qualifies, just for opening the account. The government also provides a one-time $25 payment to help offset the cost of opening the account.

- The Annual Top-Ups: They automatically add another $100 per year for every subsequent year you remain financially eligible until the calendar year the child turns 15, up to a lifetime cap of $2,000 per child.

- The Retroactive Catch-Up: If you didn’t open an account when your child was younger but qualified in the past, that money isn’t gone. When an RESP is opened, previously unclaimed CLB entitlements may be paid into the account, allowing eligible families to recover benefits that would otherwise have been missed. In fact, young adults aged 18 to 20 can even open an RESP for themselves to claim their missed childhood CLB money before they turn 21.

- The Shift to Auto-Enrollment: Because so many eligible families miss out on this cash due to paperwork barriers, the federal government is introducing an automatic enrollment system. As of June 2026, the federal government plans to introduce an automatic enrollment process beginning in 2028 and deposit the CLB for eligible children born in 2024 or later if their parents haven’t already done so by the time the child turns four.

4. The Ultimate Low-Income Booster: Layering the Support

It is a common misconception that you have to choose between the Canada Learning Bond (CLB) and the standard matching CESG grant. In reality, they stack, i.e., an eligible family gets both the CLB and the CESG.

If an eligible lower-income family opens an RESP and contributes $2,500 in the first year, they receive:

- $500 CLB kickstart

- $500 basic CESG grant

- $100 “Additional CESG” top-up

In other words, a $2,500 contribution can immediately become $3,600 inside the RESP. Layering these benefits can significantly accelerate early account growth while reducing the family’s required out-of-pocket contributions.

5. Where to Open an RESP and How to Manage It

Knowing the rules of the RESP is only half the battle; you also need to know where to open the account, what assets to hold, and how to safely steer the portfolio across an 18-year timeline.

The “Where”: Choosing Your Platform

You can open an RESP at virtually any Canadian financial institution, but the platform you choose dictates how much control you have over your costs and investments:

- The DIY Option (Online Brokerages): If you manage your own investments using low-cost Exchange-Traded Funds (ETFs) or stocks, a self-directed online brokerage account is usually the most efficient route. It gives you absolute control over your asset allocation and keeps management fees to a minimum.

- The Traditional Route (Banks and Mutual Fund Companies): Most major banks offer individual and family RESPs. While convenient, be mindful of what the money is invested in — high-fee mutual funds can quietly erode a significant portion of your child’s educational nest egg over nearly two decades.

⚠️ Buyer Beware: Stay Away from “Group” or “Scholarship” RESPs

While researching RESPs, you will likely encounter private companies offering “Group RESPs” or “Scholarship Trust Plans.” Approach these with extreme caution.

Unlike a standard bank or self-directed RESP, Group RESPs require you to sign a rigid contract to buy specific “units” and commit to a strict, mandatory contribution schedule. The pitfalls are substantial:

- Punitive Fee Structures: High upfront “enrollment fees” or sales charges are taken entirely out of your early contributions. If you cancel or modify the plan in the first few years, you may lose thousands of dollars.

- Inflexibility: If your financial situation changes and you miss a scheduled payment, you can face steep penalties or forfeit your account entirely.

- Pooled Risk: Your investment growth is pooled with other children born in the same year. If your child decides not to go to post-secondary school, or doesn’t follow their highly specific payout timelines, you often forfeit your investment earnings to the rest of the pool.

Stick to an individual or family RESP at a mainstream financial institution where you retain 100% control over the schedule, the contributions, and the capital.

The “What”: Managing the Asset Allocation Lifecycle

An RESP has a very specific, hard deadline: the money will be spent starting around age 17 or 18. Because the timeline is relatively short compared to retirement planning, your investment strategy must adapt as the child grows.

Think of managing an RESP like landing an airplane — you want a smooth, stable descent as you approach the runway.

Phase 1: The Early Years (Ages 0 to 12) — Accumulation Mode: When the child is young, time is on your side. You have a decade or more before a single dollar needs to be withdrawn. At this stage, the portfolio can afford to be heavily weighted toward equities (stocks or equity ETFs) to capture long-term growth and outpace inflation.

Phase 2: The Middle Years (Ages 13 to 14) — Balanced Mode: As high school approaches, market volatility becomes a much bigger risk. A sharp market crash right before college could severely impair your principal. During these years, it is wise to start lock-stepping your asset mix into a more balanced posture, introducing fixed-income securities (bonds, GICs, or short-term bond ETFs) to preserve capital.

Phase 3: The Final Stretch (Ages 15 to 18) — Capital Preservation Mode: With university only a few years away, your primary goal switches entirely from “growing the money” to “protecting the money.” By the time the student enters Grade 11 or 12, the funds needed for the upcoming first and second-year tuition should ideally be entirely out of the stock market and tucked safely into cash, High-Interest Savings Accounts (HISA), or short-term Guaranteed Investment Certificates (GICs).

Note: RESP contributions do not have to stop when a child turns 18 or begins post-secondary education. As long as the beneficiary has not exceeded the $50,000 lifetime contribution limit and the RESP remains open, additional contributions can still be made. However, CESG grants are generally no longer available after the end of the calendar year in which the beneficiary turns 17.

6. Advanced Concept: The “Front-Loading” Playbook

For parents or grandparents who have a significant lump sum available early on, a classic financial debate emerges: Should you drip-feed $2,500 a year to maximize the government grant, or drop a massive lump sum into the account on Day 1?

This is known as Front-Loading, and it highlights a fascinating conceptual trade-off between a guaranteed short-term bonus and the long-term time value of money.

Consider the following conceptual strategies:

A. Pure Front-Loading ($50,000 on Day 1)

Instead of waiting 15 years, you deposit the full $50,000 lifetime limit into the RESP immediately after the child is born.

- The Grant Trade-Off: Because basic grants are capped at $500 per calendar year, a single flat deposit means you will only receive $500 in government money for that first year. You permanently forfeit the remaining $6,700 of the lifetime grant limit.

- The Compounding Advantage: In exchange for losing the bulk of the grants, you gain something much more powerful: time. Consider the math at a conceptual level: even a conservative 5% return on a $50,000 investment generates $2,500 in tax-sheltered growth in just the very first year. That growth alone is significantly more than the $500 annual matching grant you miss out on. Over a long investment horizon, the additional years of tax-sheltered compounding may outweigh the value of the forgone grants. Whether that occurs depends on the eventual investment returns earned inside the account.

B. The Year-End Straddle Variation (The $1,000 Grant Alternative)

If you like the idea of maximum front-loading but hate the thought of leaving the initial grant money on the table, there is a highly effective tactical variation: Split the contribution across the calendar year-end.

Instead of depositing $50,000 all at once, you deposit $25,000 in December of Year 1 and the remaining $25,000 in January of Year 2.

Because the contributions land in two separate calendar years, you successfully trigger the maximum annual grant for both years. This simple timeline tweak means you capture $1,000 in total grant money ($500 for December and $500 for January) while still getting your entire $50,000 principal completely tax-sheltered and invested in the markets within a matter of days.

C. The Hybrid “Sweet Spot” Strategy

If you don’t have $50,000 or even $25,000 to invest in Year 1, and you want the best of both worlds — unleashing heavy compounding while leaving absolutely zero government money on the table — you can utilize a hybrid approach:

- The Setup: You deposit $15,000 in Year 1. This secures your first $500 grant while getting a large lump sum into the market immediately.

- The Drip: You then contribute $2,500 annually for the next 14 years.

- The Result: The initial $15,000 provides an early compounding head start. The subsequent annual contributions continue to generate CESG until the maximum $7,200 grant is reached and the $50,000 lifetime contribution limit is fully utilized.

📘 Deep Dive: Want to see the exact row-by-row math and spreadsheet projections for these strategies? Check out my follow-up article, RESP Front-Loading: Does Time in the Market Beat Government Grants?, where I break down the exact final values, return sensitivities, and the $16,500 hybrid growth schedule.

A Crucial Prerequisite

Front-loading an RESP is an advanced wealth-transfer strategy. It should only be considered if your own retirement accounts (RRSP and TFSA) are already completely maxed out. It rarely makes sense to lock up money for a child if your own tax-free buckets still have available room.

The Grandparent Legacy Strategy

If you are a grandparent with extra capital beyond your own retirement needs, front-loading an RESP or funding an annual drip is an incredibly powerful way to gift wealth across generations tax-sheltered.

However, because the $50,000 lifetime contribution limit and $7,200 grant cap apply per child (not per account), you must navigate two strict rules:

- Mandatory Coordination: You must coordinate closely with the parents. If your combined annual deposits exceed the grant matching limits, you miss out on free money. Worse, if total lifetime contributions exceed $50,000, the excess amount is subject to a 1% per month tax until the over-contribution is corrected.

- Keep It Simple: Instead of opening a separate RESP — which multiplies administrative fees and tracking paperwork — the cleanest route is usually to gift the funds directly to the parents to deposit into the primary account.

Can Aunts and Uncles Jump In?

Yes. Aunts and uncles can completely open or contribute to an RESP for their nieces and nephews. However, they need to be aware of a strict CRA definition regarding plan types:

- They Cannot Open a Family Plan: Under the Income Tax Act, nieces and nephews are not considered “blood relatives” for RESP purposes (the definition strictly flows vertically from parents/grandparents or horizontally between siblings). Therefore, an aunt or uncle cannot open a single Family Plan to cover multiple nieces and nephews from the same family.

- The Route to Take: If an aunt or uncle wants to open an account themselves, they must open a separate Individual RESP for each specific niece or nephew.

Just like with grandparents, the exact same warning applies: all separate accounts share the child’s single lifetime limit of $50,000 and $7,200 in grants. Close coordination with the parents is mandatory to ensure no one accidentally triggers the CRA’s 1% over-contribution penalty.

7. The RESP Exit Strategy: How to Take the Money Out

Putting money into an RESP is only half the battle; the real strategy is pulling it out without falling into an unnecessary tax trap.

When it comes time to withdraw funds for post-secondary education, the money inside the RESP is divided into two entirely separate buckets, each treated differently by the CRA:

- Bucket 1: PSE (Post-Secondary Education): This bucket consists of the original after-tax contributions made by the subscriber. Because you already paid tax on this money before putting it into the RESP, PSE withdrawals are 100% tax-free. Furthermore, this money can be directed back to the subscriber or given to the student with zero tax consequences.

- Bucket 2: EAP (Educational Assistance Payment): This bucket is made up of all the government grants (like the CESG and CLB) and the accumulated investment growth/earnings inside the account. When you withdraw EAP money, it is legally taxable. However — and this is the beauty of the plan — it is taxed in the hands of the student, not the parent.

Because most students have very low income and can utilize the basic personal tax credit, they can often withdraw thousands of dollars of EAP completely tax-free.

The Strategic Playbook: Drain the EAP First

When a child enters college or university, you must explicitly tell your financial institution which bucket you are withdrawing from.

A common mistake is withdrawing the tax-free original contributions (PSE) first because it feels “safe.” In many situations, prioritizing EAP withdrawals early can be more advantageous. Generally, you should strategically exhaust the EAP bucket as quickly as possible during the student’s early, lowest-income years.

If you leave the EAP bucket untouched and the student unexpectedly drops out or graduates early to take a high-paying job, that growth will eventually be taxed at your personal marginal rate, plus a hefty 20% penalty. The goal is often to use the taxable EAP funds while the student remains in a low tax bracket, preserving flexibility for the original contributions.

Note: There is a federal cap on EAP withdrawals during the first 13 consecutive weeks of enrollment. The limit is $8,000 for full-time students and $4,000 for part-time students. Once those initial 13 weeks pass, the restriction lifts completely for the remainder of their studies, though total annual EAP withdrawals are subject to the CRA’s indexed benchmark for reasonable education expenses without requiring special documentation, which sits at $29,459, as of 2026.

International Education: RESP Funds Are Not Limited to Canada

A common misconception is that RESP funds can only be used for Canadian schools. In reality, eligible post-secondary education outside Canada also qualifies.

Students can use RESP savings at approved foreign institutions, including universities and colleges in the United States, United Kingdom, Europe, and other countries, as long as the program meets CRA post-secondary education requirements.

For international programs, eligibility generally depends on the structure of the program rather than the location. Degree programs typically qualify when the student is enrolled full-time, while certain shorter programs may also qualify if they meet minimum duration and study-hour requirements.

In other words, the RESP is a global education funding tool — not a Canada-restricted account — as long as the studies meet the definition of post-secondary education under CRA rules.

8. The “What If” Scenarios: Managing the Risk

The number one objection people have to opening an RESP is simple: “What if my child decides not to go to university or college?” Fortunately, the framework is highly forgiving, and you won’t lose your shirt if plans change.

- The 36-Year Window: An RESP can remain open for up to 36 years. If an 18-year-old wants to take a decade-long gap period to travel, start a business, or work before returning to school, the account can sit and grow quietly.

- The Sibling Swap: If you have a Family Plan, you can easily allocate funds to another child pursuing higher education. Investment growth can be shared freely, and CESG grants can be used by the sibling (up to the individual lifetime grant cap of $7,200).

- The RRSP Rollover: If higher education is officially off the table and the account must be closed, your original contributions (PSE) return to you entirely tax-free. The government grants must be returned to Ottawa. However, the accumulated investment growth — technically called an Accumulated Income Payment (AIP) — can be rolled directly into the subscriber’s RRSP to avoid immediate taxation and the 20% penalty. This rollover is allowed up to a lifetime cap of $50,000, provided the subscriber has the necessary RRSP contribution room available.

The Bottom Line

The RESP is not just a passive savings bucket; it is an incredibly flexible, tax-sheltered investment engine. Whether you leverage low-income benefits such as the Canada Learning Bond, contribute $2,500 annually to maximize CESG eligibility, or front-load a lump sum to accelerate tax-sheltered compounding, ignoring the RESP often means leaving valuable government support and tax advantages on the table.

Open a low-cost, self-directed RESP, coordinate across the family, manage the portfolio’s investment lifecycle as the kids grow, and build a clear exit strategy. Your future graduate — and your portfolio — will thank you.

🧠 Put Your Knowledge to the Test! Reading about RESPs is one thing, but navigating real-world tax scenarios is another. I have designed a Review Quiz to stress-test your grasp of contribution limits, grant-layering math, and strategic exit playbooks.

Disclaimer: This article is for educational purposes only and is not financial or tax advice. Please consult a qualified tax or financial professional before making any decisions.

What are your thoughts on this post? Share your comments with us.

Stay ahead of the curve. Subscribe here to get notified whenever I publish a new guide or tool.

Share your comment or feedback. We'll get back to you as soon as we can.