RESP Front-Loading: Does Time in the Market Beat Government Grants?

Comparing Traditional, Front-Loaded, and Hybrid Funding Strategies

In my previous article, “RESP Explained in Plain English”, I discussed how an RESP works and briefly touched upon the front-loading strategy. This strategy can significantly increase the RESP portfolio’s value compared to the traditional approach, in which parents contribute $2,500 annually to maximize the CESG (Canada Education Savings Grant).

In this article, I will compare the two strategies in detail so that you may decide which one works best for you.

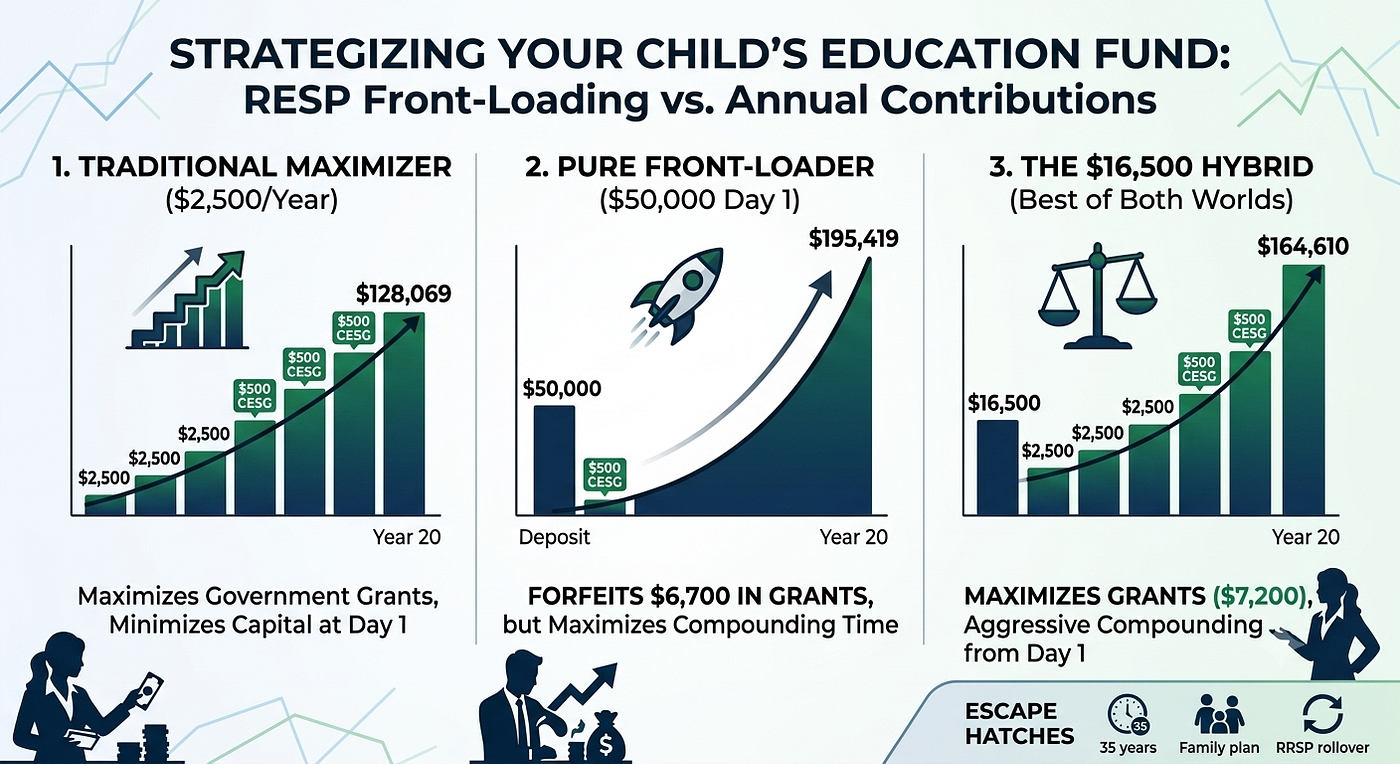

1. The Traditional Grant Maximizer

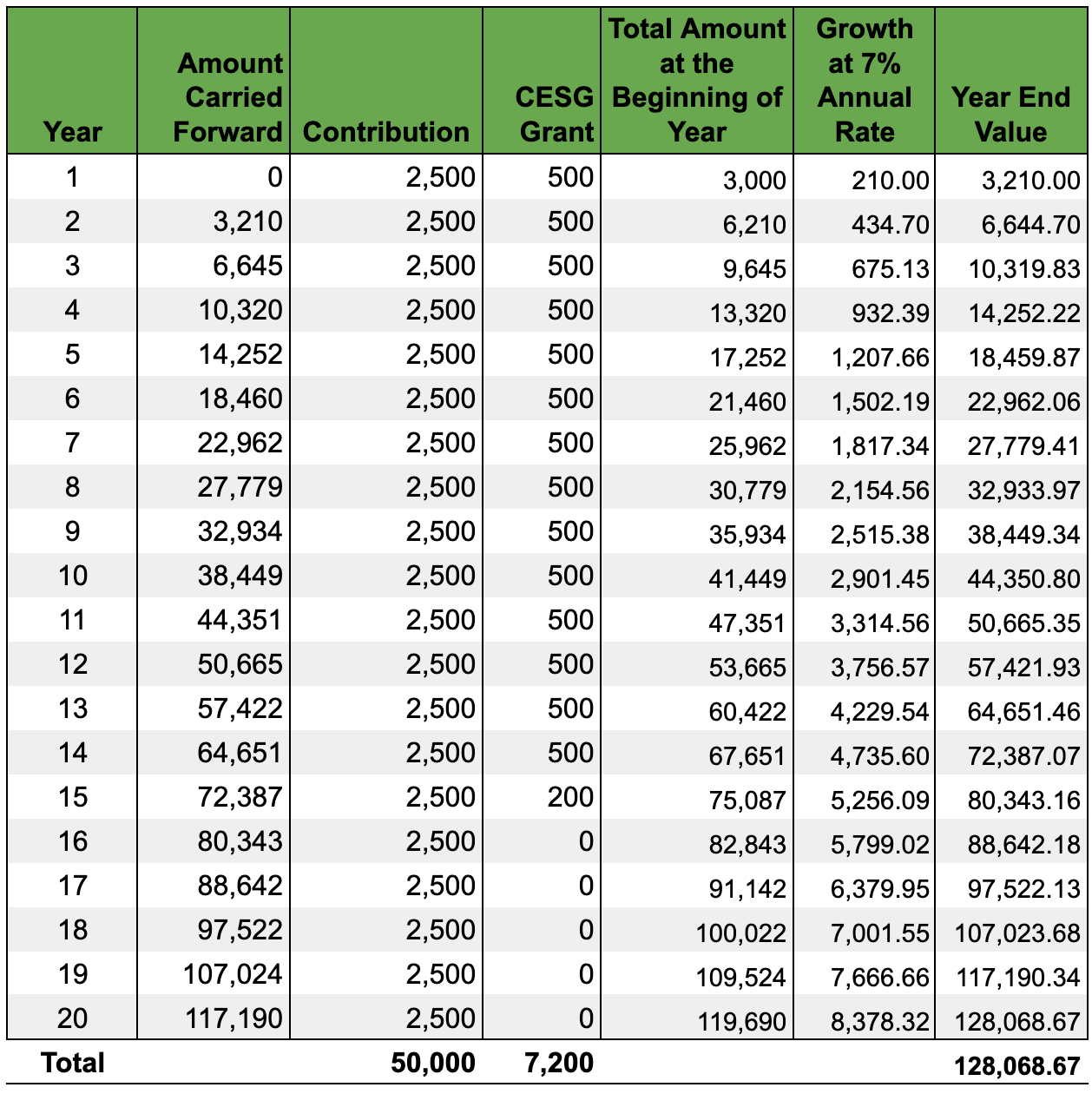

Let us assume that a child is born to Bob and Linda in December 2025. Concerned about future university costs, they open an RESP account for their child on January 1, 2026, with an initial contribution of $2,500.

To maximize both government grants and contribution room, they commit to contributing a total of $50,000 over time. One common approach is to contribute $2,500 annually until the maximum CESG entitlement is reached and then continue contributing until the $50,000 lifetime contribution limit is fully utilized. By doing this, they will also secure the maximum lifetime CESG (Canada Education Savings Grant) of $7,200. (Note that the $7,200 grant cap will be fully reached during the 15th year of contributions, meaning subsequent deposits will not receive a government match).

To keep our analysis clean and simple, we will assume that based on Bob and Linda’s household income, they do not qualify for the Additional CESG or the Canada Learning Bond (CLB).

The following table displays the projected growth of this traditional strategy over a 20-year horizon at a 7% annualized growth rate:

At a 7% annualized growth rate, the traditional account is projected to grow to about $128,069 by the end of Year 20. If the RESP grows at an 8% annualized rate, the final account value will reach approximately $144,625 by Year 20.

📌 Important Note on These Projections: These final Year 20 figures assume that the entire account balances are left untouched to compound uninterrupted for the full two decades. In reality, if Bob and Linda’s child begins university at age 18 or 19 and they immediately start making Educational Assistance Payment (EAP) withdrawals to pay for tuition and housing, the final account balances at Year 20 will naturally be lower because there will be less remaining capital left in the account to compound.

2. The Pure Front-Loader (The $50,000 Lump Sum)

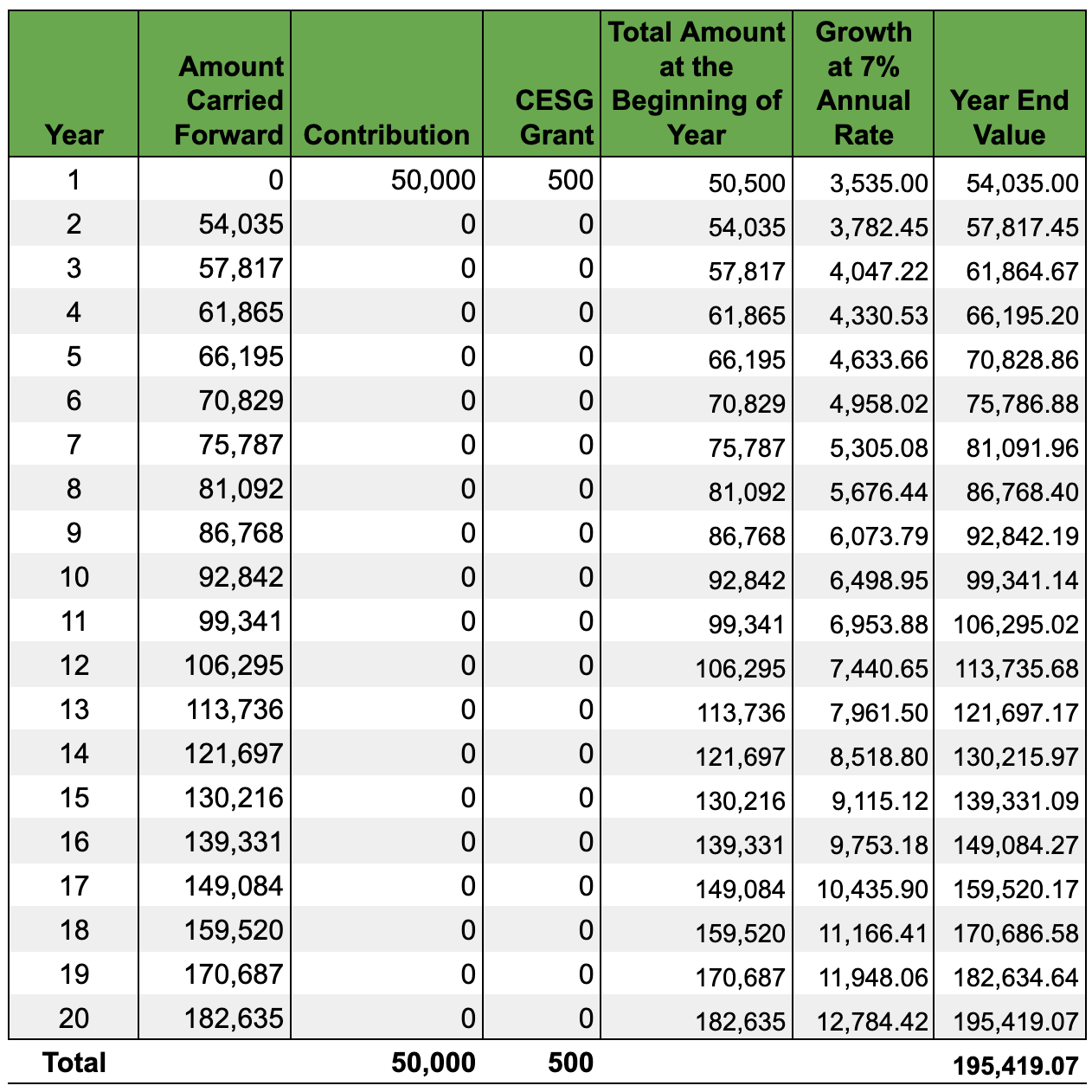

Now, let us look at the alternative scenario. Assume Bob and Linda have extra cash available, or the child’s grandparents wish to gift $50,000 on day one toward the newborn’s future university education.

On January 1, 2026, the moment the RESP is opened, they deposit the entire $50,000 lump sum into the account.

Because the federal government caps matching grants at $500 per calendar year, this single contribution triggers only a $500 CESG payment. Furthermore, because the account has immediately hit the $50,000 lifetime personal contribution limit, no further deposits can legally be made. As a result, the account will never qualify for future grants.

In other words, by choosing to front-load, the RESP explicitly forfeits $6,700 of potential government grant money ($7,200 maximum lifetime grant minus the initial $500 received).

Using the same 7% annualized rate of return, the following table displays how this upfront capital compounds over the 20-year horizon:

At a 7% annualized growth rate, the front-loaded account is projected to grow to $170,687 by the end of Year 18, and will reach $195,419 by Year 20. If the RESP grows at an 8% annualized rate, the account value will reach approximately $235,378 by Year 20.

Risk Consideration: Front-loading places substantially more money in the market during the early years. While this increases the potential benefit of long-term compounding, it also increases exposure to short-term market volatility. Families considering this strategy should ensure that their investment mix and risk tolerance are appropriate for a long-term investment horizon.

3. The Verdict: Compounding vs. Matching Grants

Now that we have analyzed both paths, let us put them side-by-side. The traditional method maximizes the government’s free money, while the front-loading method maximizes time in the market.

Assuming a 7% annualized growth rate, here is how the two strategies look at the end of Year 20:

Why Early Compounding Outperforms Free Government Grants

Looking at the numbers, the pure front-loader beats the traditional approach by a staggering $67,350.

When Bob and Linda chose to front-load the RESP on day one, they explicitly gave up $6,700 in “free” government grants. However, by forcing that extra $47,500 into the market right at the beginning, they allowed the unstoppable engine of long-term compounding to run at full steam for 20 years.

Ultimately, the market growth generated by having a large lump sum compounding early on completely eclipsed the value of waiting around for gradual government matching payments.

The Takeaway: If a family or grandparents have the financial liquidity to do so, front-loading an RESP turns the account into an absolute growth powerhouse, illustrating how early compounding can outweigh forgone grants over long time horizons.

The Return Rate Sensitivity Rule

It is important to emphasize that the size of this financial victory depends entirely on your portfolio’s annualized rate of return:

- 📈 At an 8% or 9% growth rate: The gap between the two strategies becomes even wider. Higher market returns act like rocket fuel for the front-loaded $50,000 lump sum, allowing early compounding to widen the gap between the front-loading strategy and the gradual grant-maximization approach.

- 📉 At a 6% growth rate (or lower): The gap begins to close. Because a lower market return rate weakens the compounding engine, the guaranteed, immediate 20% return provided by the annual $500 CESG grants holds onto more of its relative value.

The Mathematical Reality: Because the front-loading strategy deliberately walks away from $6,700 in “free” government matching money, it relies entirely on time and market growth to make up the difference. Historically, diversified equity portfolios have generated attractive long-term returns, although future results are never guaranteed. The 7% annualized return used in these examples is intended as a reasonable planning assumption rather than a prediction of future performance. Over a 20-year horizon, as long as your portfolio achieves a reasonable long-term equity return, compounding will almost always cross the breakeven point and come out well ahead.

4. The $16,500 Hybrid Strategy (The Best of Both Worlds)

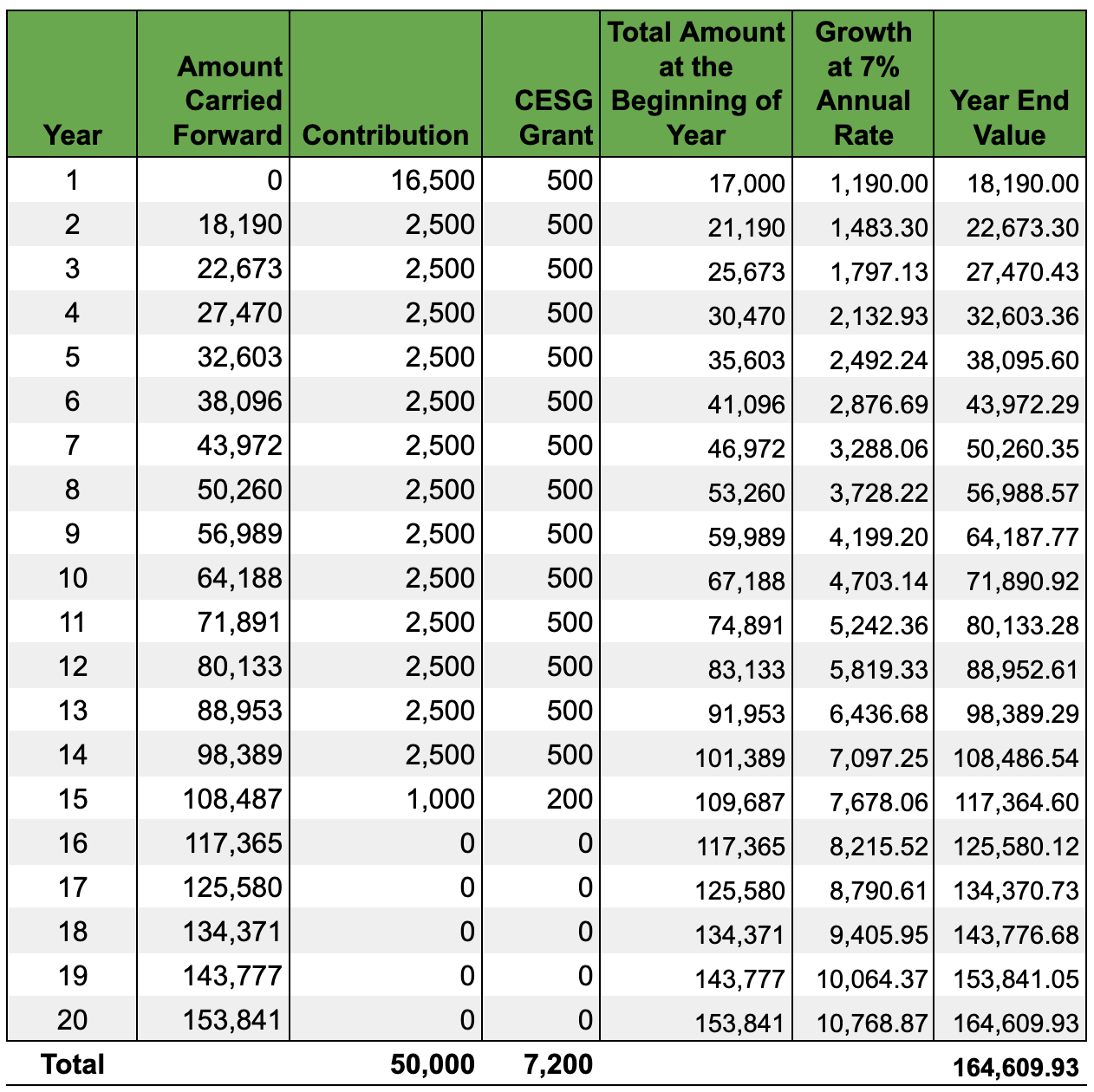

What if you don’t want to walk away from $6,700 of free government money, but you still want an explosive head start? Or what if you love the idea of compounding early, but you simply don’t have $50,000 of extra cash to invest on day one?

Instead of depositing $50,000 or $2,500 on Day 1, you deposit exactly $16,500 in the first year. By structuring your deposits using the $16,500 hybrid blueprint, you achieve a balance between maximizing long-term compounding and preserving your full CESG entitlement.

- Year 1 (Age 0): You deposit $16,500. The government applies the maximum annual matching grant of $500. This leaves you with $33,500 of remaining lifetime contribution room ($50,000 — $16,500).

- Years 2 through 14 (Age 1 to 13): You contribute exactly $2,500 each year for 13 years (totalling $32,500). Every single year, the government drops in a $500 matching grant, securing an extra $6,500 in total grants.

- Year 15 (Age 14): You deposit the final remaining $1,000 of your lifetime room ($16,500 + $32,500 + $1,000 = $50,000). The government matches this final deposit with a $200 grant.

Using the same 7% annualized rate of return, the following table displays how this hybrid strategy compounds over the 20-year horizon:

The Verdict: How the Hybrid Compares

By the end of Year 15, you have contributed your exact $50,000 personal limit and collected the maximum $7,200 in total CESG grants. You did not forfeit a single dime of government matching money. Yet, you successfully forced an extra $14,000 into the market on Day 1 ($16,500 initial deposit minus the standard $2,500), allowing it to compound tax-sheltered for two decades.

At a 7% annualized growth rate, here is how the final Year 20 account values stack up across all three strategies:

- The Traditional Maximizer: $128,069

- The $16,500 Hybrid Strategy: $164,610 (Beats Traditional by $36,541)

- The Pure Front-Loader ($50,000): $195,419 (Beats Hybrid by $30,809)

The Takeaway: While the hybrid strategy does not produce a higher final value than the pure $50,000 front-loader, it offers the ultimate middle ground for self-directed investors. By optimizing your Day 1 deposit without giving up a single dollar of federal grants, you capture an extra $36,541 over the traditional approach. It stands out as an incredibly realistic, accessible, and high-yielding strategy for families balancing optimization with real-world cash flow.

5. The Contingency Plan: What If the Child Doesn’t Go to University?

When parents or grandparents look at a massive projected balance like $164,000 or $195,000, a common anxiety creeps in: “What happens to all this money if the child chooses a different path, or simply doesn’t use the full amount?”

This is a valid concern, but the structure of the Canadian RESP is incredibly flexible. You are not locking your money away in a rigid “use-it-or-lose-it” vault.

If Bob and Linda find themselves with a large unspent RESP balance, they have several highly effective mitigation paths:

The 35-Year Clock (Time is on Your Side)

Most RESPs can remain open for up to 35 years from the date they are established, providing considerable flexibility if educational plans are delayed. If the child decides to travel, take a gap decade, or enter the workforce immediately after high school, there is absolutely no need to rush to close the account. The portfolio can sit in the market, continuing to compound tax-sheltered. The child can tap into it much later in life for a post-grad degree, a professional certification, or an MBA.

The Family Plan Route (Sibling Sharing)

If Bob and Linda have a family RESP plan with more than one child, the rules become even more favourable. If the eldest child opts out of post-secondary education, the assets can easily be redirected to the younger sibling.

- Your personal contributions can be completely shared.

- The CESG grants can also be transferred to the sibling, provided the receiving child does not exceed the lifetime individual grant limit of $7,200.

The Rising Cost of Living & Tuition

Tuition, textbooks, and housing costs will likely rise significantly over the next two decades. Furthermore, RESP funds are not restricted to tuition alone. They can generally be used to support a student’s education-related living expenses, including housing, food, transportation, textbooks, and computer equipment while enrolled in a qualifying program. A large account balance that may seem like “too much” today may simply align with the real-world costs of a four-year degree 18 years from now.

The Ultimate Escape Hatch: The RRSP Rollover

If the 35-year limit is approaching, there are no other siblings, and higher education is completely off the table, the rules allow you to dismantle the account systematically:

- Your Contributions: Every single dollar of the $50,000 personal principal you deposited belongs to you. Because it was originally contributed with after-tax money, you can withdraw it 100% tax-free.

- The Grants: Any unused CESG grant money must be returned to the federal government.

- The Investment Growth (Accumulated Income Payment): The massive pile of market growth inside the account is technically taxable in your hands at your regular marginal tax rate, plus a 20% penalty tax. However, you can completely avoid this penalty.

The Tax Optimization Strategy: Under CRA rules, if the RESP has been open for at least 10 years and the beneficiary is at least 21 years old, you can roll up to $50,000 of the investment growth directly into your Registered Retirement Savings Plan (RRSP) or a Spousal RRSP, provided you have the contribution room available. This completely defers the standard tax and eliminates the 20% penalty.

The Bottom Line

The greatest misconception about RESPs is that they are simply education savings accounts. In reality, they are long-term wealth-building vehicles that combine government incentives, tax-sheltered growth, and considerable flexibility. Whether you choose a traditional contribution schedule, a front-loading strategy, or a hybrid approach, the key is to start early, invest consistently, and use the RESP’s grants and tax-sheltered growth to their fullest advantage.

Disclaimer: This article is for educational purposes only and is not financial or tax advice. Please consult a qualified tax or financial professional before making any decisions.

What are your thoughts on this post? Share your comments with us.

Stay ahead of the curve. Subscribe here to get notified whenever I publish a new guide or tool.

Share your comment or feedback. We'll get back to you as soon as we can.