The Hidden Opportunity Cost of CPP: A 24-Year Case Study of Investing vs. Pension Contributions

How private compounding and tax-efficient withdrawals could outperform the CPP pension by 54% — while preserving the original principal in this case study.

For decades, Canadians have been told that the Canada Pension Plan (CPP) is the “bedrock” of a secure retirement system. But what happens when you apply the logic of a disciplined investor to those numbers? When we move beyond the general messaging and examine the implied Internal Rate of Return (IRR), a different perspective can emerge. For many medium- or high-income earners, the CPP can resemble an expensive insurance policy where the “premiums” generally do not return to your estate.

The Methodology: A 24-Year Controlled Experiment

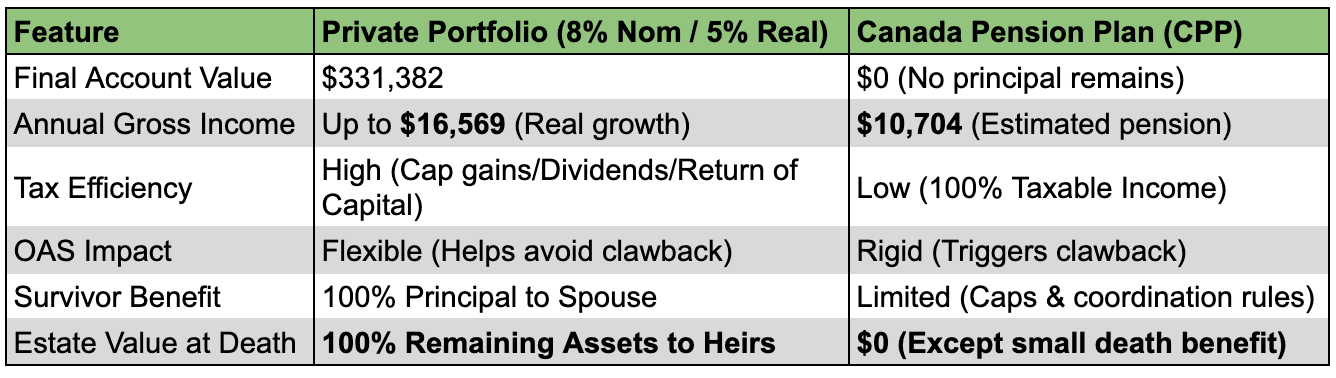

To test the efficiency of the CPP, I tracked my actual contributions (including the employer’s match) from 1997 through 2020. I stopped working in September 2020 at age 60 and made no further contributions to the plan. Based on this contribution history, my estimated CPP benefit at age 65 is approximately $10,704 per year in today’s dollars.

I then simulated a private, non-registered investment portfolio growing at an assumed 8% annual return. By the end of 2025, even without any additional contributions during those final five years, the power of compounding would have grown the portfolio to approximately $331,382.

Important Assumption: The 8% return used in this analysis is not an arbitrary figure; it is grounded in two key data points:

- Institutional Performance: It is in line with the 8.3% 10-year annualized net return recently reported by the CPP Investment Board (CPPIB) as of March 2025.

- Personal Performance: It is consistent with my own 25-year history as a self-directed investor, where my RRSP, TFSA, and non-registered accounts have collectively yielded an annualized return exceeding 8%.

While the CPP provides a guaranteed benefit that shields against market volatility, this case study explores the significant wealth-building potential of achieving institutional-level returns within a private, self-directed framework.

The Results: Private Wealth vs. Social Insurance

The structural differences between a private investment portfolio and the CPP pension become clearer when viewed side by side.

The comparison highlights the structural differences between a private investment portfolio and a government pension benefit.

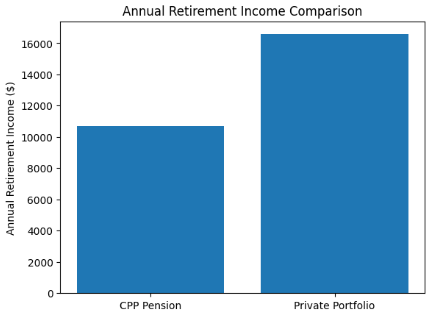

The income difference becomes even clearer when visualized.

The Internal Rate of Return (IRR) Gap

Various independent studies, including research from the Fraser Institute, estimate that the real internal rate of return (IRR) of CPP contributions for higher-income contributors often falls in the range of roughly 2% to 4%, depending on lifespan and claiming age. This creates a startling “Performance Gap.” While the fund itself grows at 8%, the high-earning contributor only “receives” a fraction of that growth. This case study explores how private investment returns could compare when you capture that full growth for yourself.

The “Infinite” Principal: Higher Lifestyle, Same Capital

In our private model, we assume a 5% real rate of return (8% nominal minus 3% inflation) after age 65 to keep the principal’s purchasing power constant.

- Scenario A (The Match): If you withdraw $10,704 annually (matching the estimated CPP benefit), you are withdrawing less than the real growth; the principal would still grow in real terms to roughly $650,000 by age 95.

- Scenario B (The Higher Standard): Alternatively, you could withdraw the full $16,569. This provides an income roughly 54% higher than the CPP benefit, yet your original $331,382 principal remains perfectly intact.

The Power of Tactical Flexibility

The most significant advantage of the private model is that you are not forced to spend the income every year. If you experience a year with lower expenses or have other sources of cash flow, you can leave the funds in the account to compound even further. Furthermore, these surplus funds can be strategically moved into a Tax-Free Savings Account (TFSA) — up to your available contribution room — to ensure that future growth and withdrawals are entirely tax-free. While the CPP is a “use it or lose it” monthly payment, private capital acts as a dynamic reservoir that you can optimize based on your life’s changing needs.

Addressing the “Tax Drag” and the Growth Tilt

Critics of private investing often point to the “tax drag” in a non-registered account — the annual tax paid on dividends and distributions, which can slow compounding. While it is true that a high-dividend portfolio might see the $331,382 value reduced slightly due to annual taxes, a sophisticated investor has a clear workaround: Growth-Oriented Investing.

By selecting growth stocks or low-dividend ETFs during the accumulation phase, an investor can defer the majority of their tax liability until retirement. With this “accumulation tilt,” the tax drag is minimized, allowing the 8% compounding to work at near-maximum efficiency. The tax is only triggered when you decide to sell and withdraw — on your own terms.

The After-Tax Advantage

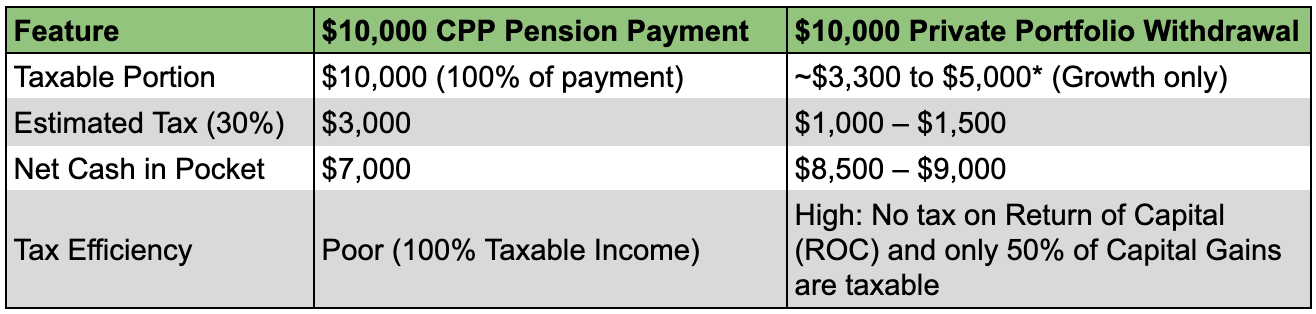

Gross income tells only part of the story. Net income — what you actually keep — is where the private portfolio can provide a meaningful advantage.

1. Immediate Tax Savings on Cash Flow

To understand the difference, consider a $10,000 withdrawal from both sources for a retiree in a 30% marginal tax bracket. Because CPP is 100% taxable as ordinary income, the “haircut” you take on your pension is significantly steeper than a withdrawal from your own capital.

*Assumes a mix of original capital (tax-free) and accumulated growth (taxed at capital gains rates).

2. The OAS Clawback Protection

This tax-efficiency has a powerful secondary effect: protecting your Old Age Security. CPP payments are 100% “on-paper” income. This can push you over the threshold for the OAS Recovery Tax (Clawback). For every dollar over the threshold (approx. $95,323 for 2026), you lose 15 cents of your OAS. Because a private withdrawal shows a much lower “taxable income” on your return despite providing the same cash flow, it allows you to stay below the threshold and protect your full OAS.

3. Preferential Credits

While CPP is taxed at your full marginal rate, Canadian dividends and capital gains receive preferential treatment. You keep more of every dollar you earn.

Survivor Outcomes: Legacy vs. Limited Estate Value

The structural differences between the CPP and a private portfolio are perhaps most stark when considering what you leave behind.

- The CPP Model: If you are single, your decades of contributions essentially vanish upon death (beyond a small $2,500 death benefit). If you have a spouse, the survivor benefit is often capped and subject to complex eligibility rules, and your children typically receive nothing.

- The Private Model: In this case study, the $331,382 principal belongs entirely to you. It can pass to your spouse tax-deferred, and eventually to your children as a significant inheritance. You aren’t just funding a retirement; you are building a multi-generational legacy.

In effect, the private portfolio provides a 100% survivor benefit because the remaining assets belong to your estate. Unlike the CPP, where benefits are limited and subject to caps, the full market value of the investment account remains available to your heirs.

A Note on “Insurance Features”

Critics often point out that CPP contributions also fund disability coverage and survivor pensions. While true, it is important to contextualize these “benefits”:

- Superior Survivor Protection: As shown above, the private model’s survivor protection is mathematically superior, as it preserves the entire capital rather than a restricted monthly payment.

- Existing Workplace Coverage: Many employees already hold comprehensive Long-Term Disability (LTD) coverage through their workplace extended insurance benefits.

- Low-Cost Private Alternatives: For those without workplace coverage, private disability insurance can often be purchased for a small fraction of one’s income (typically 1–3%).

For the disciplined investor, the “insurance” bundled into the CPP is often redundant or overpriced compared to the massive opportunity cost of the lost investment capital.

Conclusion: Wealth Building vs. Pension Security

The CPP is a vital program for the “average” Canadian who may lack the discipline to save or the skill to invest. It provides a guaranteed, inflation-protected safety net that is impossible to outlive.

However, for the sophisticated investor, the CPP is often less of a benefit and more of a mandatory, high-cost insurance-style contribution. As this case study illustrates, by following a disciplined private investment model, we aren’t just seeking higher returns; we are gaining three critical advantages:

- Generational Wealth: Transforming “vanished” contributions into a $331,000+ legacy for heirs.

- Tax Efficiency: Gaining the flexibility to draw income strategically, effectively protecting the OAS from costly clawbacks.

- Optimization of Coverage: Recognizing that “bundled” insurance, like disability, can often be covered more efficiently through workplace benefits or targeted private policies.

Ultimately, we sacrifice hundreds of thousands of dollars in potential wealth for a guaranteed CPP payment that is mathematically less efficient than disciplined, long-term investing. For those with the capacity to manage their own capital, the true cost of the “bedrock” pension is the multi-generational opportunity we leave on the table.

Disclaimer: This article is for educational purposes only and is not financial or tax advice. Please consult a qualified tax or financial professional before making any decisions.

What are your thoughts on this post? Share your comments with us.

Stay ahead of the curve. Subscribe here to get notified whenever I publish a new guide or tool.

Share your comment or feedback. We'll get back to you as soon as we can.