The GIS Optimization Strategy: When It Makes Sense to Empty Your RRSP Before Age 65

Don’t let your savings trigger a pay cut: A case study on avoiding the 50% GIS clawback and the age 71 RRIF trap.

In my previous article, GIS: The Secret Weapon for Low-Income Retirement in Canada, I explained how the Guaranteed Income Supplement (GIS) can quietly become the largest source of income for many retirees. I also discussed how the GIS clawback works — and how certain types of income reduce benefits far more aggressively than others.

But understanding the rules is only half the battle. The real question is:

How do retirement income choices — the timing of CPP, the management of RRSP withdrawals, and the reorganization of non-registered assets — determine whether you receive maximum GIS, partial GIS, or nothing at all?

Let’s look at a real-world case study.

Case Study: Retirement Planning for a Low-Income Earner

Profile:

Sara, a 60-year-old resident of Ontario, is a single individual planning to retire at age 65. She currently earns an employment income of $40,000 per year. After accounting for 2026 tax rates, CPP, and EI premiums, her annual take-home pay is approximately $33,300 ($2,775/month).

Current Savings & Assets:

Sara is now an active saver, putting away $4,000 annually, split equally between her RRSP and TFSA. Her current account balances are:

- RRSP: $70,000

- TFSA: $40,000

Retirement Goal:

Sara aims to maintain a monthly after-tax income of $2,500 ($30,000/year) starting at age 65.

The Challenge:

At age 65, Sara will be eligible for Old Age Security (OAS) and the Guaranteed Income Supplement (GIS), provided her taxable income remains low. However, her RRSP presents a unique hurdle.

While her RRSP balance is currently $70,000, Sara plans to continue contributing $2,000 annually over the next five years. Assuming a 5% inflation-adjusted real return, her account is projected to grow to approximately $100,500 by the time she retires. This significant nest egg — ironically — could become a liability.

Traditional Retirement Plan

In a traditional scenario, Sara would begin collecting her government benefits at age 65 and bridge the gap to her $2,500 monthly goal using her private savings.

Government Pension Floor

Sara’s retirement income is anchored by two primary government sources:

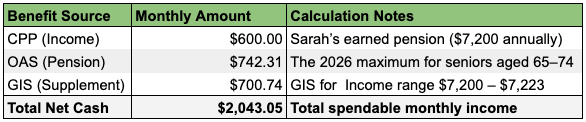

- Old Age Security (OAS): Having resided in Canada for over 40 years after age 18, Sara qualifies for the full OAS pension. As of January 2026, this provides $742.31 per month (~$8,908 per year).

- Canada Pension Plan (CPP): Based on her career earnings, Sara’s estimated CPP benefit at age 65 is $600 per month ($7,200 per year).

The GIS Factor

Crucially, because Sara’s income for GIS purposes (which excludes OAS but includes CPP and RRIF withdrawals) is only $7,200, she is a prime candidate for the Guaranteed Income Supplement.

- At a CPP income level of $7,200, Sara is eligible for approximately $701 per month in GIS (based on January 2026 benefit tables; GIS rates are adjusted quarterly).

- Total Monthly Floor: This brings her total monthly “baseline” to $2,043.31 ($742.31 OAS + $600 CPP + $701 GIS).

Meeting the Required Cash Flow

Sara’s target monthly income is $2,500. With her baseline income of $2,043, she faces a monthly shortfall of $457. She must decide whether to bridge this gap using her TFSA or her RRSP.

The Choice: TFSA Withdrawals

Sara knows that TFSA withdrawals are tax-free and — more importantly — do not count as income for GIS calculations. She decides to withdraw $457 per month ($5,484 per year) from her TFSA to meet her $2,500 goal.

The Six-Year Result (Ages 65–71)

Sara follows this strategy for six years. Because her TFSA withdrawals are “invisible” to the CRA, her GIS remains untouched at $701 per month.

However, a new challenge is growing in the background. While she spends her TFSA, her RRSP continues to sit untouched. From an initial balance of $100,500 at age 65, the account grows at a 5% inflation-adjusted real return. By the time she reaches age 71, her RRSP balance has ballooned to approximately $134,700.

The RRIF Withdrawal Trap

Sara’s strategy of using her TFSA worked perfectly for six years. However, Canadian tax law requires all RRSPs to be converted into a Registered Retirement Income Fund (RRIF) by December 31 of the year the owner turns 71. This transition triggers three immediate negative consequences:

1. The Mandatory Withdrawal

At age 71, the mandatory RRIF withdrawal rate is 5.28%, calculated based on the January 1 balance of the RRIF each year. Based on Sara’s ballooned account balance of $134,700, her first year’s mandatory withdrawal is:

- $134,700 × 5.28% = $7,112 per year (~$593 per month).

2. The GIS “Double Tax”

Because RRIF withdrawals are considered taxable income, they trigger a “double hit” effect: you pay income tax, and your GIS is reduced through the clawback — often losing 50 to 75 cents of GIS for every dollar withdrawn.

- Sara’s total “GIS-reportable” income: $7,200 (CPP) + $7,112 (RRIF) = $14,312.

- The Payout: According to the 2026 GIS tables, a single senior with $14,312 in income sees her monthly GIS drop from $701 down to only $360.

3. The New Tax Bill

For the first time in retirement, Sara’s income exceeds her tax-exempt thresholds. After applying the 2026 federal and Ontario basic personal amounts, she will owe approximately $200 per year in income tax. This further reduces her monthly spending power by about $17.

The Widening Gap

To maintain her $2,500 monthly lifestyle, Sara now faces a serious shortfall. While her gross income has technically increased due to the RRIF, her actual take-home pay has plummeted.

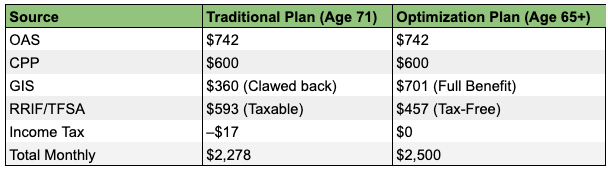

Monthly Cash Flow Calculation (Age 71):

- OAS: $742.31

- CPP: $600.00

- RRIF (Min): $592.67

- GIS (Reduced): $360.00

- Less Income Tax: –$16.67 (Approx. $200/year)

- Total Monthly Take-Home: $2,278.31

Sara is now $221.69 short of her $2,500 goal every month. Sara has two choices, both of which are problematic:

Withdraw from TFSA

If she uses her remaining TFSA funds, she preserves her GIS, but once those funds are gone, she has no “safe” money left.

Withdraw More from RRIF

To bridge this $222 gap using her RRIF, she cannot simply withdraw $222. Because of the 50%–75% GIS clawback and the income tax on those withdrawals, she might have to withdraw closer to $500 from her RRIF just to see an extra $222 in her pocket.

Furthermore, because RRIF withdrawal percentages increase every year based on her age, her taxable income will continue to climb, her GIS will continue to vanish, and her savings will be depleted at an accelerating rate.

Strategy 2: The GIS Optimization Plan

Sara’s “Traditional Plan” failed because it ignored the heavy clawback rules of the GIS. To avoid the RRIF trap at age 71, Sara needs a strategy that prioritizes taxable income reduction during her retirement years.

Step 1: Stop RRSP Contributions (Ages 60–65)

The first mistake in the traditional plan was continuing to contribute $2,000 annually to an RRSP. For a low-income earner like Sara, the tax refund she gets today (roughly 20%) is far outweighed by the 50–75% GIS loss she will face when she takes that money out later.

The Fix: Sara redirects her entire $4,000 annual savings into her TFSA.

- The Result: By age 65, her TFSA is larger, and she hasn’t added more fuel to the “RRSP tax time bomb.”

Step 2: The RRSP Meltdown (Ages 60–64)

Sara decides to “melt down” her $70,000 RRSP over five years (ages 60–64) while she is still working. By withdrawing $14,000 per year on top of her $40,000 salary, her tax bill increases by approximately $3,296 annually.

Is it worth it?

To many, paying an extra $3,296 in taxes seems counterintuitive. However, let’s look at the “Return on Investment”:

- The Cost: Sara pays $16,480 in total extra taxes over 5 years.

- The Reward: By emptying the RRSP, she protects her GIS from being clawed back later. In the “Traditional Plan,” she was losing $341 per month ($4,092 per year) in GIS starting at age 71.

- The Break-Even: In just 4 years of retirement ($16,480 / 4,092), Sara has fully “recovered” the taxes she paid during the meltdown.

- By age 75, she is strictly “in the profit,” receiving thousands of dollars in government benefits that the “Traditional Plan” would have wiped out.

The Strategic Reinvestment:

After paying the $3,296 tax on the $14,000 RRSP withdrawal, Sara has about $10,704 left. She uses this to maximize her TFSA.

Step 3: The “Clean Slate” Retirement (Age 65+)

By age 65, Sara has successfully emptied (or significantly reduced) her RRSP. Her financial picture now looks very different:

- RRSP Balance: $0 (The “Liability” is gone).

- TFSA Balance: ~$130,000+ (Including her original $40k, $4K annual contribution, the “Meltdown” transfers, and 5 years of growth).

Step 4: Comparison at Age 71

By the time Sara reaches age 71, the difference between the two strategies is staggering.

In the Traditional Plan, Sara’s GIS is reduced significantly to $360 from its potential of $701. Furthermore, to even get close to her goal, she is forced to take a larger taxable withdrawal of $593 from her RRIF, compared to a much smaller $457 tax-free withdrawal from her TFSA in the Optimized Plan.

Despite taking more money out of her private savings in the traditional scenario, her net cash in hand is approximately 10% smaller than the optimized plan. Sara is effectively working harder and spending more of her own money just to receive less from the government.

Because she only needs to take $457 from her TFSA to reach her $2,500 goal (instead of the $593 RRIF minimum), her private savings will last much longer, providing her with a much larger “emergency fund” for later in life.

The Verdict: The “Net-Positive” Math

When you look at the raw numbers, the ‘RRSP Meltdown’ isn’t actually a loss — it’s an arbitrage play.

By emptying your RRSP between 60 and 64, you are essentially ‘buying’ a 50% raise for your future self. Yes, you might pay a 20% or 30% tax rate today to get those funds out. But for every dollar you successfully move into a TFSA or a non-registered account before age 65, you are preventing a 50% to 75% GIS clawback later.

You are trading a small, immediate tax bill for a much larger, guaranteed government subsidy. In the world of Canadian retirement, a 20-30% tax hit is a bargain if it protects you from a 50% benefit cut for the next 20 years.

The GIS Strategy Cheat Sheet: 3 Pillars

If you expect to rely on the Guaranteed Income Supplement, your goal isn’t just to save — it’s to manage your taxable income. Use these guardrails to ensure the system works for you:

- Prioritize the “Invisible” Asset: If your income is modest (under $50,000), stop the RRSP contributions. The small tax refund today is a trap that triggers a massive “GIS tax” later. Use your TFSA; it is invisible to Service Canada and has zero impact on your GIS payments.

- Execute the “Clean Slate” Meltdown: Aim to enter age 65 with little to no RRSP balance. Use your early 60s to aggressively draw down those funds. Paying tax now to protect a 50%+ benefit later is the smartest trade you can make.

- Position for 65+: Once you hit 65, your goal is a low taxable income, not a low actual income. By moving RRSP money into TFSAs early, you create a tax-free fortress that pays you without triggering government penalties.

The Final Takeaway: Strategy Trumps Savings

The hardest part of this strategy isn’t the math — it’s the mindset. For forty years, you’ve been told that an RRSP is a ‘sacred’ account that shouldn’t be touched until the last possible moment.

But for low-to-middle-income Canadians, the traditional rules are a trap. High-net-worth investors focus on tax deferral; you need to focus on benefit qualification.

Don’t let the fear of a tax bill today blind you to the windfall of a maximized GIS tomorrow. Success in a GIS-optimized retirement isn’t about how much you saved — it’s about how strategically you’ve positioned those savings to stay out of the government’s reach. Strategy doesn’t just trump savings; it protects them.

Important Considerations: This strategy is intended for retirees who expect to rely heavily on GIS. Keep in mind that GIS rules and income thresholds can change. In some cases, a partial drawdown is more optimal than a full meltdown. Always review your plan against the current CRA and Service Canada guidelines.

Disclaimer: This article is for educational purposes only and is not financial or tax advice. Please consult a qualified tax or financial professional before making any decisions.

What are your thoughts on this post? Share your comments with us.

Stay ahead of the curve. Subscribe here to get notified whenever I publish a new guide or tool.

Share your comment or feedback. We'll get back to you as soon as we can.