Understanding RRSP Overcontribution Rules

The $2,000 Cushion and the 1% Monthly Tax

RRSP overcontribution rules are frequently misunderstood. While the framework provides a small safety buffer, excess contributions can quickly become an expensive headache if left uncorrected.

The $2,000 Lifetime Buffer

The CRA allows taxpayers to exceed their cumulative RRSP contribution limit by up to $2,000 without triggering the monthly overcontribution tax.

However, it is vital to remember:

- This buffer does not create additional tax deduction room.

- You cannot claim a tax deduction on the $2,000 excess contribution.

- The cushion acts as a safety net to prevent immediate penalties on minor calculation errors.

When Does the 1% Overcontribution Tax Apply? (A Real Example)

If your total RRSP excess exceeds the $2,000 buffer, the CRA charges a tax equal to 1% per month on the amount above the buffer for each month the excess remains in the account.

Suppose an investor accidentally overcontributes $6,000 on October 1. Here is how the CRA calculates the monthly overcontribution tax:

- Total RRSP excess: $6,000

- Less the lifetime buffer: $2,000

- Taxable excess: $4,000

- Monthly overcontribution tax: $40

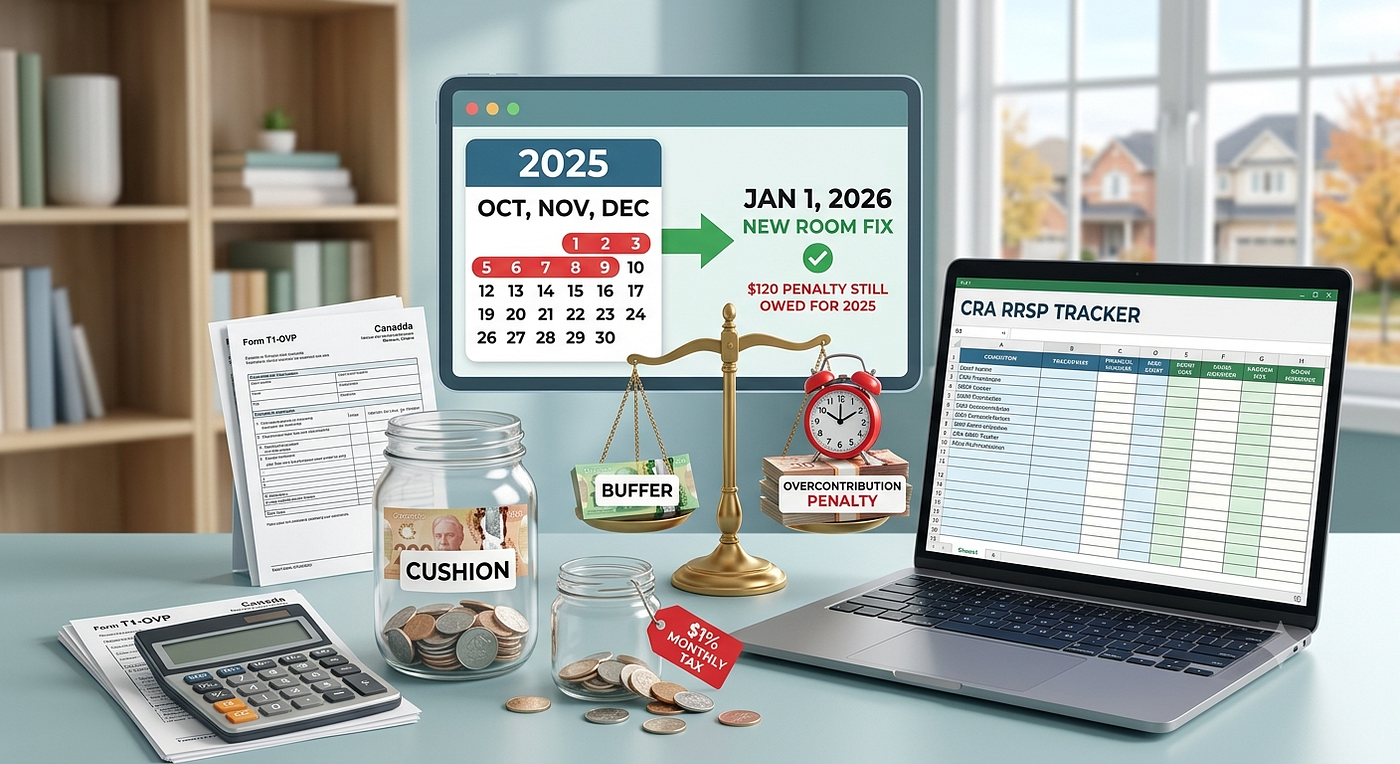

For October, November, and December, the overcontribution tax totals $120 ($40 × 3 months).

What Happens on January 1st? (The New Room Nuance)

A common misconception is that new RRSP contribution room generated on January 1st retroactively erases the previous year’s mistake. It does not.

Continuing our example, suppose the investor receives $10,000 of new RRSP contribution room on January 1st.

- The overcontribution is no longer an excess contribution. Because the investor now has sufficient RRSP contribution room, the previous $6,000 excess is fully absorbed by the new room. As a result, the 1% monthly overcontribution tax stops applying after December.

- The prior-year tax is still payable. The new contribution room does not eliminate taxes that already accrued. The investor still owes the $120 accumulated from October through December and may need to file Form T1-OVP.

- Future contribution room is reduced. Since $6,000 of the new $10,000 room has effectively been consumed by the prior overcontribution, only $4,000 of unused contribution room remains available for future contributions.

When Should You Withdraw the Excess?

If you discover that you have overcontributed to your RRSP, don’t ignore the problem and assume it will eventually resolve itself.

If the excess contribution was made only a few days or weeks ago, consider correcting the issue as soon as possible. Prompt action can prevent additional months of the 1% overcontribution tax from accumulating.

If you do not expect sufficient new RRSP contribution room in the following year to absorb the excess contribution, withdrawing the excess amount may be the best option.

In some situations, CRA allows excess RRSP contributions to be withdrawn without withholding tax by filing Form T3012A before the withdrawal is made. Professional tax advice may be worthwhile if the excess amount is significant.

How the CRA Catches Up

Much like TFSA overcontributions, CRA typically identifies RRSP excess contributions after financial institutions submit annual contribution information.

By the time you receive a CRA letter or notice, several months of overcontribution tax may already have accumulated.

Key Takeaway

The $2,000 RRSP buffer provides some flexibility, but excess contributions above that amount can trigger a 1% monthly overcontribution tax that continues until the situation is corrected or sufficient new contribution room becomes available.

Tracking your RRSP deduction limit on your latest Notice of Assessment — and maintaining your own contribution records throughout the year — is the best way to avoid unexpected overcontribution taxes.

Disclaimer: This article is for educational purposes only and is not financial or tax advice. Please consult a qualified professional before making any decisions.

What are your thoughts on this post? Share your comments with us.

Stay ahead of the curve. Subscribe here to get notified whenever I publish a new guide or tool.

Share your comment or feedback. We'll get back to you as soon as we can.