The 2025 Canadian Retirement Roadmap: How Much Do You Really Need?

Mastering the math of CPP, OAS, and the 4% Rule to build your own pension

Most of us spend our lives trading time for money, hoping that one day we’ll have enough to stop. For decades, the “deal” was simple: work for one company, get a gold watch, and collect a guaranteed pension. Today, that deal is dead.

In the modern world, retirement has become a DIY project. While well-paying government pensions still exist, they are increasingly rare in the private sector. The good news? With a clear look at your actual needs and the power of compounding on your side, a comfortable retirement is more achievable than the “experts” lead you to believe.

It’s time to plan for your retirement and build your own pension.

How Much Money Do You Need to Retire?

The classic “expert” answer is that you need 70% to 80% of your pre-retirement income. If you earn $100,000 today, they say you’ll need $80,000 in retirement.

For many Canadians, this figure is too high. By the time you retire, your lifestyle usually shifts significantly:

- The Mortgage is Gone: Ideally, your biggest monthly expense has vanished.

- No More Savings Grinds: You are no longer funnelling money into RRSPs, TFSAs or RESPs for the kids.

- Lower Taxes: You aren’t paying into CPP or EI anymore, and your lower income often puts you in a friendlier tax bracket.

The “Floor” Strategy: Needs vs. Wants

To arrive at a realistic estimate of your retirement spending, start by reviewing your actual expenses from the past one to two years. If you use digital payment methods — such as credit cards, debit cards, Interac e-Transfers, or direct withdrawals from your bank account — your bank and credit card statements can provide a reliable picture of your monthly expenses.

Go through these statements and subtract any costs you expect to disappear in retirement, such as contributions to retirement savings (RRSPs and TFSAs), children’s education savings (RESPs), and mortgage payments (ideally, your mortgage will be paid off before you retire). This process will give you a rough estimate of the income you will need during retirement.

Your retirement expenses generally fall into two categories:

Needs (Your “Floor”): Essentials such as groceries, property taxes/rent, utilities, home/car maintenance, cell phone, insurance, transportation (gas) and internet.

Wants (Your Lifestyle): Discretionary spending such as travel, dining out, and sports.

At a minimum, your retirement income should cover your essential needs — the “floor.” Depending on your desired lifestyle, it may also need to support some or all of your wants. Once you’ve identified these amounts, you can estimate how much income you’ll need in retirement.

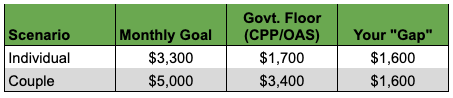

For example, let’s assume you need $3,300 per month in retirement. Next, we’ll look at how much of this amount may be covered by Canadian government benefits.

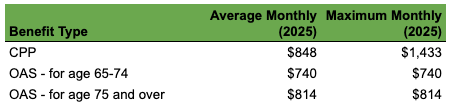

The 2025 Government Benefit Reality

At the traditional retirement age of 65, Canadians may receive two government benefits: the Canada Pension Plan (CPP) and Old Age Security (OAS). CPP payments are based on your work and contribution history, while OAS depends on how many years you have lived in Canada after age 18. To receive the maximum OAS benefit, you must have lived in Canada for at least 40 years after turning 18.

As of 2025, the following are the average and maximum CPP and OAS benefits for a Canadian retiring at age 65.

If you have not lived in Canada for the full 40 years since turning 18, OAS benefits are paid on a pro-rated basis. For example, if you have lived in Canada for only 30 years after age 18, your OAS payment would be calculated as $740 × 30 ÷ 40, or approximately $555 per month. OAS benefits increase by 10% starting at age 75.

Note: These benefits are indexed to inflation — OAS is adjusted quarterly and CPP annually — helping your retirement income keep pace with rising living costs.

Estimating your OAS payments in retirement is relatively straightforward, as OAS is based on the number of years you have lived in Canada after age 18.

To estimate your CPP retirement pension based on your actual contribution history to date, sign in to your My Service Canada Account (MSCA). Once signed in, navigate to the Canada Pension Plan section and select “View my benefit estimates.”

You can also get a broader estimate of your retirement income by using the Canadian Retirement Income Calculator, which combines CPP, OAS, and other sources of retirement income.

The Power of Two: Government Benefits for Couples

While retirement planning is often discussed in individual terms, the math shifts dramatically for a household. In 2025, a couple’s “government floor” is one of the most powerful tools in their roadmap.

- Double OAS: Unlike many social programs, Old Age Security is an individual entitlement. If both partners have lived in Canada for 40 years after age 18, the household receives double the OAS. In 2025/2026, this amounts to roughly $17,800 per year in guaranteed, inflation-indexed income for the couple.

- Dual CPP Income: If both partners worked and contributed, both are entitled to their own CPP. For a two-income household, even two “average” CPP payments (approx. $850/month each) combined with OAS can provide over $38,000 per year in total benefits.

Pro-Tip: Don’t forget that if one partner has a significantly higher CPP payment, you can apply for CPP Pension Sharing to balance your tax brackets and keep more of that $3,400 in your pockets.

The “Enhanced” Future: Why the Floor is Rising

It is also important to note that the government benefits we see today are just the starting point. Since 2019, Canada has been phasing in the CPP Enhancement, a multi-year project designed to boost the “Government Floor” for future retirees significantly.

- The Goal: The plan is shifting from replacing 25% of your pre-retirement earnings to replacing 33.33%.

- The 2026 Milestone: As of January 2026, the second phase of this enhancement is fully in place. This includes a new, higher earnings ceiling ($85,000), ensuring that middle-income earners protect more of their salary under the CPP umbrella.

- The Result: For younger workers and those mid-career, the payoff is massive. A worker contributing under these enhanced rules for a full 40-year career could see a maximum benefit that is over 50% higher (in inflation-adjusted terms) than the previous system.

What this means for your roadmap: By the time these enhancements fully mature, a couple could see combined CPP and OAS payments that cover an even larger portion of their lifestyle. This “rising floor” continues to shrink the “Gap,” meaning the total private savings you need to retire comfortably is actually lower than it was for previous generations.

Bridging the Gap

If your goal is $3,300 per month and the government provides $1,700, you are left with a “Gap” of $1,600 per month ($19,200 per year).

Similarly, for a couple, the “Government Floor” is much higher. If your household goal is $5,000 per month and the government provides roughly $3,400 (two sets of OAS and average CPP), you are left with the same $1,600 per month gap.

In both cases, your personal savings only need to generate that $19,200 annual difference to maintain your lifestyle.

However, you actually need to aim slightly higher. Since withdrawals from an RRSP or a taxable account are subject to income tax, you must factor in a “tax drag.” To net $1,600 in your pocket from these accounts, you might actually need to withdraw closer to $1,850, depending on your tax bracket.

The one major exception to this rule is the TFSA (Tax-Free Savings Account). While contributions don’t generate a tax deduction, all TFSA withdrawals are completely tax-free — meaning $1,600 withdrawn is exactly $1,600 in your pocket.

The Gold Standard: The 4% Rule

To determine how much capital you need to bridge this gap, most financial experts point to the 4% Rule. Created in the 1990s, this rule suggests that if you invest in a balanced portfolio (roughly 60% stocks and 40% bonds), you can safely withdraw 4% of your initial balance in Year 1, adjusted for inflation thereafter, with a high probability that your money will last at least 30 years.

To find your “Magic Number” using this rule, simply multiply your annual gap by 25:

$19,200 (Annual Gap) x 25 = $480,000

Is the 4% Rule Outdated for 2025?

While universally popular, the 4% rule isn’t a law of nature. Financial markets fluctuate, and a rigid withdrawal plan can be risky.

- The Conservative View: Some planners suggest a 3.5% rate to account for longer life expectancies and lower bond yields.

- The Aggressive View: Others argue that with a higher stock allocation (like the S&P 500, which has seen an inflation-adjusted return of 7.93% over the last 20 years), a 5% or even 6% rate could be safe.

Calculating Your Target Savings

Your personal withdrawal rate should depend on your risk tolerance and where you are invested (Canadian vs. U.S. vs. Global markets). Here is how much you would need in total savings to generate $20,000 of annual inflation-adjusted income:

- At 4% (Conservative): You need $500,000

- At 5% (Moderate): You need $400,000

- At 6% (Aggressive): You need $333,333

By understanding these ratios, you can move from “guessing” to “targeting” the exact size of the nest egg you need to build.

When Should I Start Planning? (The Cost of Delay)

The best time to start was your first paycheck; the second-best time is today. To see why, let’s look at two friends, John and Bob, navigating the Canadian economy in 2025.

The Tale of Two Savers

- John starts at age 25. He invests $300 a month into a diversified portfolio that grows by 7% per year.

- Bob waits until age 45. Realizing he’s behind, he doubles his effort and invests $600 a month into a similar portfolio growing at the same 7% per year.

Both stop saving at age 65. On paper, they have both contributed the exact same amount of “out-of-pocket” cash over their lives ($144,000). However, the results are shocking:

In spite of investing the same total amount at the same rate of growth, John finishes with a whopping $475,000 more than Bob. (Source: Ontario Securities Commission’s Compound Interest Calculator.)

Important note:

When using a compound interest calculator, use an inflation-adjusted (real) rate of return so the future value is expressed in today’s dollars, making comparisons meaningful for real-world retirement planning.

Over the long term, inflation in Canada has averaged about 2% per year. To be conservative, you may choose a slightly higher assumption (for example, 2.5%). Under that assumption, a 9% nominal return translates to roughly a 6.5% real return.

The Lesson: Time is a Lever

Why the massive gap between John and Bob? Because John’s money had an extra 20 years to do the heavy lifting. By the time Bob even started, John’s interest was already earning its own interest.

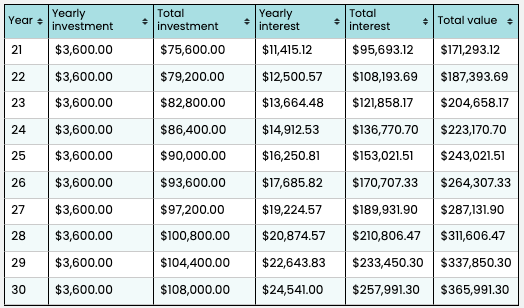

To see this acceleration in action, look at the growth of John’s account in his third decade (Years 21–30). Even though his monthly contribution never changes, his “interest engine” begins to outpace his own deposits:

Note: By Year 21, John’s interest ($11,415) is already triple his annual investment. By Year 30, his money is doing nearly seven times the work he is.

This is the Power of Compounding — the engine that turns modest monthly savings into a significant retirement “pension.” It’s not just about how much you save; it’s about how long you let that money work undisturbed.

The 2025 Reality Check

In 2025, we face a landscape of higher housing costs and persistent inflation. It’s easy to look at a goal and think, “I can’t afford $300 a month.” But as John and Bob’s story proves, waiting is the most expensive mistake you can make. In the world of compounding, size matters, but time matters more. Starting with just $100 a month in a Tax-Free Savings Account (TFSA) today is mathematically superior to waiting five years to start with $200. Don’t wait for the “perfect” time to save; start with what you have.

The numbers tell you whether retirement is financially possible. But they also reveal something deeper: how sustainable your plan truly is. The more clearly you understand your expected expenses and income sources, the more confidently you can structure a retirement that lasts — not just for a few years, but for decades.

Final Thoughts

Retirement is not about chasing a magic number like $1 million or $2 million. It is about replacing your income in a way that is realistic, sustainable, and aligned with your actual life.

Start with clarity:

- Determine your expected annual spending.

- Subtract reliable, inflation-protected income like CPP and OAS.

- Identify the “Gap” your savings must fill.

As we’ve seen, the “Government Floor” is stronger than ever. With the CPP Enhancement now fully in motion, future retirees can expect an even higher percentage of their income to be covered by indexed benefits. Whether you are an individual or a couple, this means your personal nest egg doesn’t have to carry the full weight of your lifestyle.

Retirement planning does not require a lottery-win savings account; it requires a roadmap. When you understand your income, your expenses, and the specific gap between them, retirement stops being a source of anxiety — and becomes a solvable math problem

Disclaimer: This article is for educational purposes only and is not financial or tax advice. Please consult a qualified tax or financial professional before making any decisions.

What are your thoughts on this post? Share your comments with us.

Stay ahead of the curve. Subscribe here to get notified whenever I publish a new guide or tool.

Share your comment or feedback. We'll get back to you as soon as we can.