The $1.7 Million Myth: Why You Are Closer to Retirement Success Than You Think

Why BMO’s “Magic Number” is a guess, not a requirement — and how to find your real target.

Every February, a new retirement “magic number” makes headlines — and even the most disciplined savers start to question whether they’ll ever have enough. According to the latest retirement survey by the Bank of Montreal (BMO), released in February 2026:

The amount Canadians believe they need for retirement increased by $160,000 year-over-year to $1.7 million, on average. Targets vary significantly across regions.

When you see a figure like “$1.7 million to retire comfortably,” especially if it feels like a mountain you can’t climb, what should you do?

My view: that $1.7 million figure deserves far less attention than it receives.

Behind the intimidating headline is a reality that is far more encouraging. For the average worker, that $1.7 million figure isn’t a financial requirement — it’s a reflection of national anxiety.

1. The “Guessing Game” Effect

When people respond to retirement surveys, they are rarely sitting down with a financial planner, retirement calculator or a spreadsheet. Most are answering intuitively.

Research from the Financial Consumer Agency of Canada (FCAC) reveals a significant “literacy gap”: only about 42% of Canadians can correctly answer three basic questions about interest compounding, inflation, and risk. If nearly 60% of the population struggles to calculate how a 12-month inflation rate affects a $100 grocery bill, it is a mathematical certainty that they are not performing the complex “Present Value” projections required to arrive at a $1.7 million target 25 years into the future.

So where does the $1.7 million figure come from?

For many respondents, it may be what I call a “Safety Guess” — a round, large number that feels protective in an environment dominated by headlines about inflation, housing costs, and market volatility. It feels safer to overestimate than underestimate.

That number is less a product of calculation and more a reflection of uncertainty.

2. The Psychological Trap: Demotivation Through Inadequacy

There is a hidden danger in these massive “magic numbers”: they can lead to financial paralysis.

When ordinary people compare their modest savings to a $1.7 million target, the gap feels so vast that it triggers a “giving up” response. Rather than being motivated to save more, many people start to believe they will never reach the target. This can lead to a self-fulfilling prophecy where individuals stop saving whatever little they can, or take reckless risks to “catch up.”

As BMO’s own survey notes, 14% of Canadians now say they plan to “never retire.” For many, this isn’t a lifestyle choice — it’s a white flag of surrender raised against a number they feel they can’t possibly hit.

3. The Power of the “Household”

One critical question rarely addressed in the headlines: Is the $1.7 million figure meant for one person — or for a couple?

As I discussed in my previous analysis of the 2023 BMO survey results, these figures are often misinterpreted. BMO senior portfolio manager Terri Szego clarified that the $1.7 million represents total retirement savings for a household, not an individual. This immediately slashes the individual burden to $850,000.

Furthermore, couples benefit from shared living costs. Housing, utilities, property taxes, insurance, and many other core expenses do not double simply because two people live together. In practical terms, a two-person household does not require twice the income of a single retiree to maintain a similar standard of living. In financial planning, we often find that two can live for about 1.5 times the cost of one. When retirement needs are viewed through the lens of household economics rather than individual savings targets, the intimidating headline number becomes far more manageable.

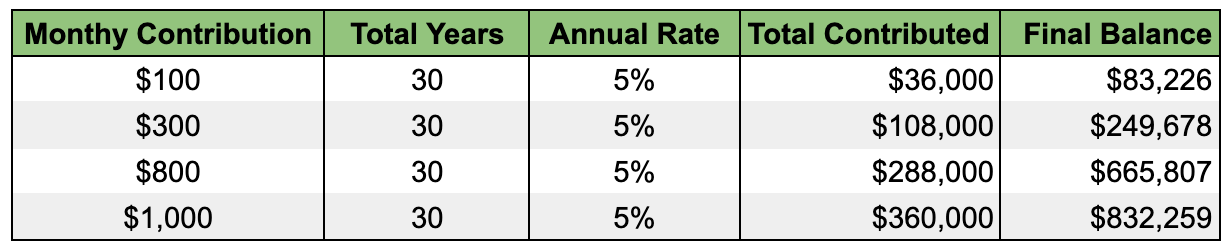

4. How Much Are Canadians Actually Saving?

The BMO survey reports that nearly one-third of respondents save less than $500 per month for retirement:

- 10% save less than $100

- 23% save $100 — $499

- 10% save $500 — $999

- 12% save over $1,000

To understand what that means, consider the long-term growth of consistent monthly savings over 30 years at a 5% annual return:

For example:

- Saving $300 per month for 30 years at 5% grows to approximately $249,678.

- At 6% annual growth, the same savings would grow to roughly $301,455.

However, unless returns are adjusted for inflation, the purchasing power of those future dollars will be significantly lower in today’s terms. Long-term projections require understanding concepts such as real (inflation-adjusted) returns, future value, and present value — calculations that many households may not formally model when estimating how much they need for retirement.

When savings assumptions, investment returns, and inflation are uncertain, it becomes easier to default to a large, “safe” number rather than build a structured plan.

But there is a more rational way to approach the problem.

4. Start With Income — Not Assets

Rather than beginning with a lump-sum target, retirement planning should start with a far simpler question:

How much will you actually need to spend each year in retirement?

Most people discover their costs drop by 30% to 50% in retirement. Mortgages are paid off, children are independent, and you stop paying into the very retirement fund you are now using. To get a handle on your own specific target, you need a structured approach rather than a guess. In my 2025 Canadian Retirement Roadmap, I provide a step-by-step guide to determining your actual retirement number based on your unique lifestyle.

Let us see how the math works for a typical retired couple, whose estimated lifestyle need is $60,000 per year (after tax).

Step 1: Subtract Government Benefits

A typical couple can receive roughly $35,000 per year combined from CPP and OAS.

Step 2: The Personal Gap

Their required income from personal savings drops to $25,000 per year.

Step 3: Calculate the Capital

Now we ask: How much capital is needed to generate that $25,000 per year? Using a conservative 4% withdrawal framework, this couple would need approximately:

$25,000 ÷ 0.04 = $625,000

Using a conservative 4% withdrawal rate, this couple needs $625,000 in total household savings.

Note on Taxes:

It is important to remember that, depending on your source of income, some taxes may be involved. If that $25,000 is coming from a Tax-Free Savings Account (TFSA), you keep every penny. However, if it comes from an RRSP or RRIF, it is considered taxable income. In that case, you might actually need to withdraw closer to $28,000–$30,000 to end up with $25,000 in your pocket. Even with this “tax tilt,” your required savings are still nowhere near the $1.7 million headline.

The Reality Check

Even with the “tax tilt” factored in, the math is clear: this couple can maintain a comfortable, $60,000-a-year lifestyle with $625,000 in total household savings.

This is a far cry from the $1.7 million household target mentioned in the headlines, and it is even well below the “clarified” individual share of $850,000.

Retirement planning is an income equation — not a guessing contest.

When you stop chasing a ‘magic number’ and start planning for your actual life, you’ll find that a secure retirement is much more accessible than the banks want you to believe.

5. The Bottom Line

The February 2026 survey from Bank of Montreal offers an interesting snapshot of Canadian retirement anxiety. But it should not be mistaken for a personalized financial roadmap.

Headlines focus on averages, while successful retirement planning focuses on your expenses, your income streams, and your timeline.

Every dollar you save reduces your future income gap, and every year of disciplined planning increases your flexibility and confidence.

The goal is not to chase an arbitrary number, but to build a sustainable income plan that supports the life you actually want to live.

Keep Reading: The 2025 Canadian Retirement Roadmap: How Much Do You Really Need?

Disclaimer: This article is for educational purposes only and is not financial or tax advice. Please consult a qualified tax or financial professional before making any decisions.

What are your thoughts on this post? Share your comments with us.

Stay ahead of the curve. Subscribe here to get notified whenever I publish a new guide or tool.

Share your comment or feedback. We'll get back to you as soon as we can.