A Beginner’s Guide to Investing (Part 3): Understanding Different Types of Investments

A plain-English breakdown of GICs, bonds, stocks, and funds

In Part 2, we looked at three things a beginner should consider before jumping in to buy an investment.

Once you decide to invest, the next question is: What should you invest in?

There is no single “best” investment because each one has its own level of risk, potential return, and purpose. Some investments are low-risk and are designed to protect your money and provide steady returns, while others are designed to help your money grow over the long term.

Understanding these differences is the first step toward making informed decisions. Here are some of the most common types of investments:

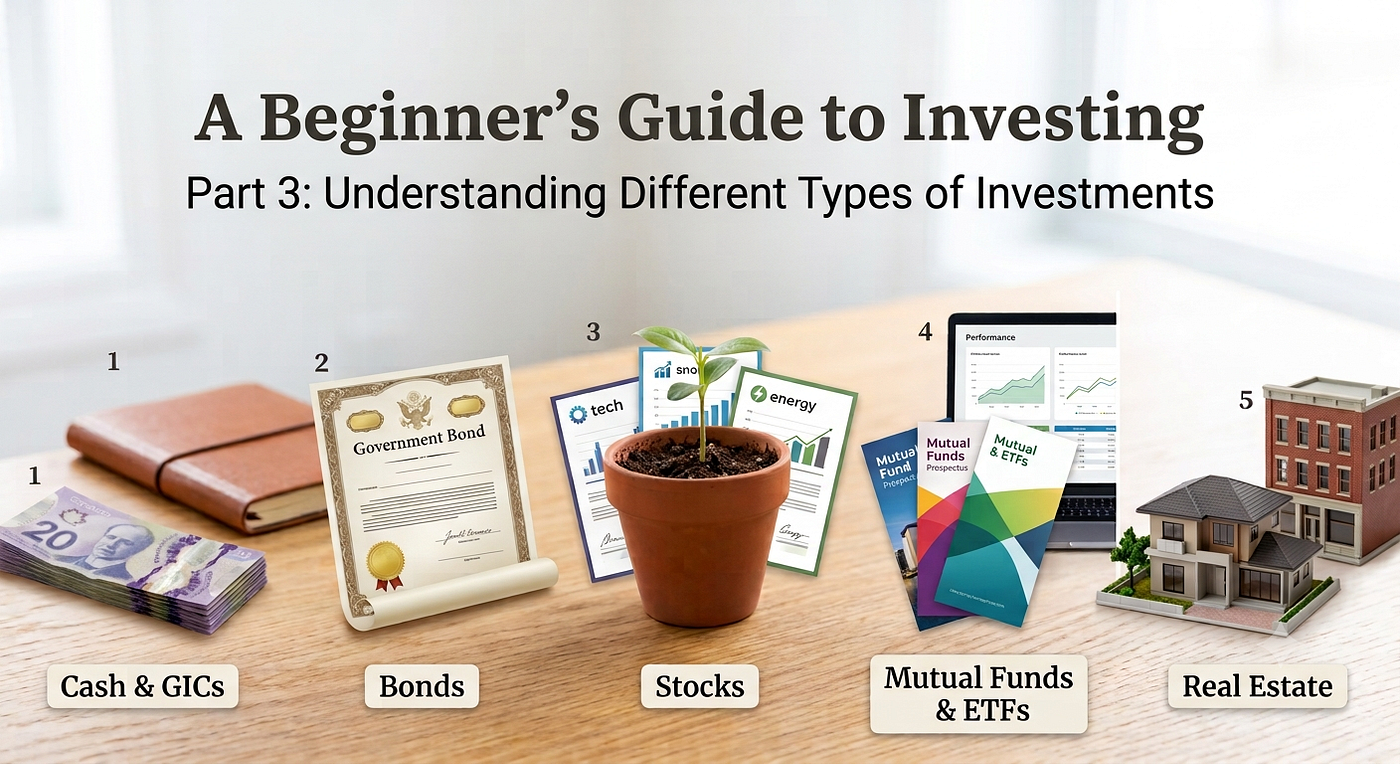

Savings Accounts and Guaranteed Investment Certificates (GICs)

Savings accounts are one of the simplest ways to earn a return on your money. You deposit your money with a financial institution, and they pay you interest over time. Some financial institutions offer high-interest savings accounts, which usually pay a higher rate of interest than regular savings accounts.

The interest rate you receive depends on factors such as overall interest rates in the economy and the policies of the financial institution. Savings accounts are very flexible because you can usually access your money whenever you need it.

Some financial institutions may require you to maintain a minimum balance to earn the advertised interest rate or to avoid monthly fees. Others, particularly online financial institutions, may pay the same interest rate regardless of whether your balance is $1 or $10,000. It is always a good idea to read the account terms before opening a savings account.

A Guaranteed Investment Certificate (GIC) works a little differently. When you buy a GIC, you agree to lend your money to a financial institution for a specific period of time. In return, the institution guarantees a fixed interest rate and returns your original investment when the GIC matures.

Unlike a savings account, your money is usually locked in until the maturity date. Some financial institutions offer cashable GICs, which allow you to withdraw your money earlier, although they typically pay a lower interest rate.

Savings accounts and GICs are generally considered the safest investments available to most Canadians. Eligible deposits held with member financial institutions are insured up to certain limits by the Canada Deposit Insurance Corporation (CDIC), a federal Crown corporation that protects depositors in the rare event of a financial institution’s failure.

Because these investments provide safety and predictable returns, they are often suitable for money you may need in the short term. However, their returns may not always keep up with inflation, which means they may not be a good choice for long-term wealth growth.

Bonds

When you buy a bond, you are lending money to a government or a company. In return, the borrower promises to pay you interest and return your original investment at the end of a specified period.

Unlike savings accounts and GICs, bonds are generally not protected by deposit insurance. The level of risk depends on who issued the bond. Bonds issued by the Government of Canada and provincial governments are generally considered safer than bonds issued by private companies, because governments are generally less likely to fail to make their interest payments or repay the money they have borrowed.

Bonds are generally considered less risky than owning shares of companies, but they carry more risk than savings accounts and GICs. Because they involve more risk than savings accounts and GICs, they generally offer higher potential returns. However, they usually have lower long-term growth potential than stocks.

Stocks (Shares)

When you buy a stock, you are buying a small piece of ownership in a company.

If the company grows and becomes more valuable, your shares may increase in value. Some companies also share part of their profits with shareholders through dividend payments.

The value of stocks can go up and down, sometimes significantly, which means they carry more risk than savings accounts, GICs, or bonds. While stocks have historically provided some of the highest long-term returns, their values can fluctuate significantly in the short term.

Mutual Funds and Exchange-Traded Funds (ETFs)

Instead of buying individual stocks or bonds yourself, you can invest in a collection of many investments through a fund. A fund pools money from many investors to buy a diversified collection of investments, such as stocks, bonds, or both. This automatically gives you diversification — spreading your money across many different investments so you don’t rely on the success of just one company.

There are two main types of funds:

- Mutual Funds: Your money is combined with money from other investors and managed by a professional investment company.

- Exchange-Traded Funds (ETFs): These work in a similar way, but they are bought and sold on a stock exchange just like individual stocks. Many ETFs track a market index, holding hundreds or even thousands of investments at a relatively low cost.

Both mutual funds and ETFs charge a fee for managing the fund. This fee is usually expressed as the Management Expense Ratio (MER). You do not pay this fee separately — it is deducted from the fund’s assets before the returns are reported. In general, mutual funds tend to have higher MERs than ETFs, although the exact fee varies from one fund to another. Before investing, it is a good idea to compare the MERs of similar funds, as higher fees can reduce your long-term returns.

For many beginners, investing in a well-diversified mutual fund or ETF is often a simpler and less risky approach than buying individual stocks. Successfully choosing individual companies requires time, research, and experience.

Furthermore, buying individual stocks can create an emotional challenge. If a beginner puts their money into just one company or a small number of companies and those investments lose significant value, they may become discouraged and lose confidence in investing altogether. Investing through a diversified ETF or mutual fund spreads your money across many companies, reducing the impact of any single investment performing poorly and making it easier to stay focused on your long-term goals.

For these reasons, ETFs and several mutual funds have become popular choices for investors seeking a simple and cost-effective way to build a diversified portfolio.

Real Estate

Real estate is another common type of investment. Some people buy properties to generate rental income, while others invest because they expect property values to increase over time.

Real estate can be a good long-term investment, but it is different from many other investments. It usually requires a large amount of money upfront, involves ongoing costs and responsibilities, and it is difficult to spread your money across many properties.

Another difference is that real estate is generally less flexible than many financial investments. If you need money, you usually cannot sell just a small portion of a property — you typically have to sell the entire property or borrow against it. This can make accessing your money more difficult and may involve additional costs and delays.

For these reasons, beginners may want to first build a diversified portfolio of financial investments before investing in rental properties. Buying a home to live in is a separate decision, as it also provides the benefit of having a place to live.

What About Cryptocurrency?

You have likely heard of digital currencies such as Bitcoin and other cryptocurrencies.

Cryptocurrency is different from many traditional investments. Unlike stocks, bonds, or rental properties, it generally does not generate income such as dividends, interest payments, or rental income. Instead, investors typically hope that the value of the cryptocurrency will increase over time.

Cryptocurrency prices can rise or fall significantly in a short period of time, making them much more volatile and riskier than traditional investments. Because of this high level of uncertainty, cryptocurrency is generally not considered a core investment for most beginners.

For beginners, it is usually more important to first build a solid foundation with diversified investments that match their goals, timeline, and risk tolerance.

Key Takeaway

There is no single investment that is best for everyone. The right choice depends on your goals, how long you plan to invest, and how much risk you are comfortable taking.

For many beginners, a well-diversified ETF or mutual fund can be a simple way to get started, while they continue learning about investing.

What’s Next?

Before choosing any investment, it is important to understand risk and return. The right investment is not necessarily the one with the highest potential return, but the one that matches your goals and your ability to handle ups and downs.

Read Next: Part 4: Understanding Risks and Returns

Disclaimer: This article is for educational purposes only and is not financial or tax advice. Please consult a qualified tax or financial professional before making any decisions.

What are your thoughts on this post? Share your comments with us.

Stay ahead of the curve. Subscribe here to get notified whenever I publish a new guide or tool.

Share your comment or feedback. We'll get back to you as soon as we can.