Understanding Emergency Funds

How much you need, where to keep it, and how to avoid common mistakes

What is an Emergency Fund?

An emergency fund is money you set aside only for unexpected expenses or financial emergencies. This could include a major car or home repair, losing your job, or an illness that prevents you from working. It can also help cover urgent situations, such as needing to travel on short notice because of a family emergency.

When something unexpected happens, you may need money right away. An emergency fund lets you pay for these expenses using your own savings instead of relying on high-interest credit cards or borrowing money.

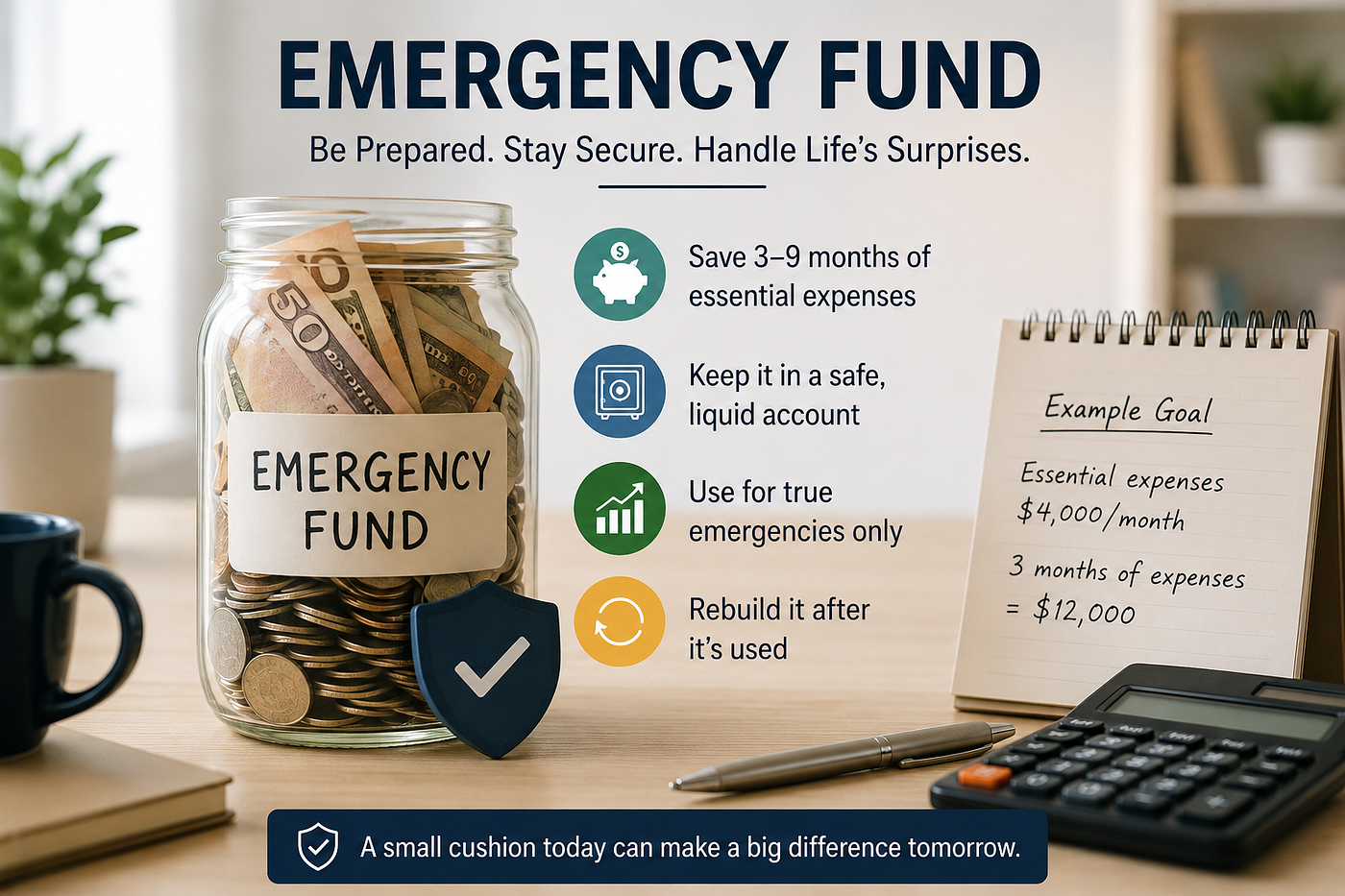

How Much Do You Need?

An emergency fund is usually calculated based on your essential monthly living expenses. This includes necessities like rent or mortgage payments, groceries, utilities, insurance, transportation, internet, and phone bills.

A good rule of thumb is to save enough to cover 3 to 9 months of these essential expenses. The right amount depends on your household and your job situation:

- 3 months if your household has two stable incomes.

- 6 months if your household relies on one income.

- 6 to 9 months if your income is irregular, such as freelance, contract, commission-based, or seasonal work.

For example, if your household’s essential monthly expenses are $4,000 and your goal is to keep 3 months of expenses on hand, you may aim to save approximately $12,000.

Where to Keep the Money?

Because you may need this money at any time, keep it in a safe, easy-to-access account. This is called a liquid account, which simply means you can withdraw your money quickly without delays or penalties.

Your emergency fund should also be protected from stock market ups and downs. Avoid investing it in individual stocks, stock ETFs, or mutual funds. If the market drops just when an emergency happens, you could be forced to sell your investments at a loss. An emergency fund is meant to provide peace of mind — not add financial stress.

Great options include:

- High-Interest Savings Accounts (HISAs)

- Money Market Mutual Funds or ETFs

- Cashable GICs (Guaranteed Investment Certificates)

Tax Tip: If you have available Tax-Free Savings Account (TFSA) contribution room, consider holding your emergency fund there. That way, you won’t pay any tax on the interest or growth your fund earns.

Prioritize Emergency Fund or Pay off Credit Card Debt?

If you have credit card debt, you’re probably paying interest of 20% to 30% a year. That’s much higher than the interest you can earn on an emergency fund.

In most cases, it’s better to keep a small emergency fund of about $1,000 to $2,000 while you focus on paying off your credit card debt. This gives you a small financial cushion so you don’t have to rely on your credit card if an unexpected expense comes up.

Once your credit card debt is paid off, you can focus on building a full emergency fund that covers 3 to 9 months of essential living expenses.

Reduce Your Emergency Fund as Your Savings Grow

When you’re just starting, it’s important to keep a larger emergency fund because you may not have other financial resources to fall back on. As your savings and investments grow, you may not need to keep as much money in cash.

In some cases, if you have a large investment portfolio in a non-registered account or a TFSA, you may be able to sell investments to cover an emergency if needed. Because of this, you may be comfortable reducing your emergency fund to about one month of essential expenses, instead of holding 3 to 6 months.

This allows more of your money to stay invested for long-term growth. However, you should still keep enough cash on hand so you can handle unexpected expenses without being forced to sell investments at the wrong time.

That said, reducing your emergency fund is not right for everyone. If your income is unstable, if you are nearing retirement, or if you would feel stressed relying on investments during an emergency, it is better to keep a larger cash cushion.

What Not to Use Your Emergency Fund For

Your emergency fund is only for true, unexpected emergencies. It should not be used for planned or optional spending, such as vacations, shopping, home upgrades, or other expenses you can plan for in advance. If the expense is expected or can be delayed, it is not an emergency.

Rebuilding Your Emergency Fund After Use

If you use your emergency fund, make rebuilding it a priority. You don’t need to restore it all at once. Instead, rebuild it gradually with regular contributions until you reach your target level again, so you are prepared for future emergencies.

Disclaimer: This article is for educational purposes only and is not financial or tax advice. Please consult a qualified tax or financial professional before making any decisions.

What are your thoughts on this post? Share your comments with us.

Stay ahead of the curve. Subscribe here to get notified whenever I publish a new guide or tool.

Share your comment or feedback. We'll get back to you as soon as we can.