TFSA Overcontributions Rules

A Small Mistake That Can Become Expensive

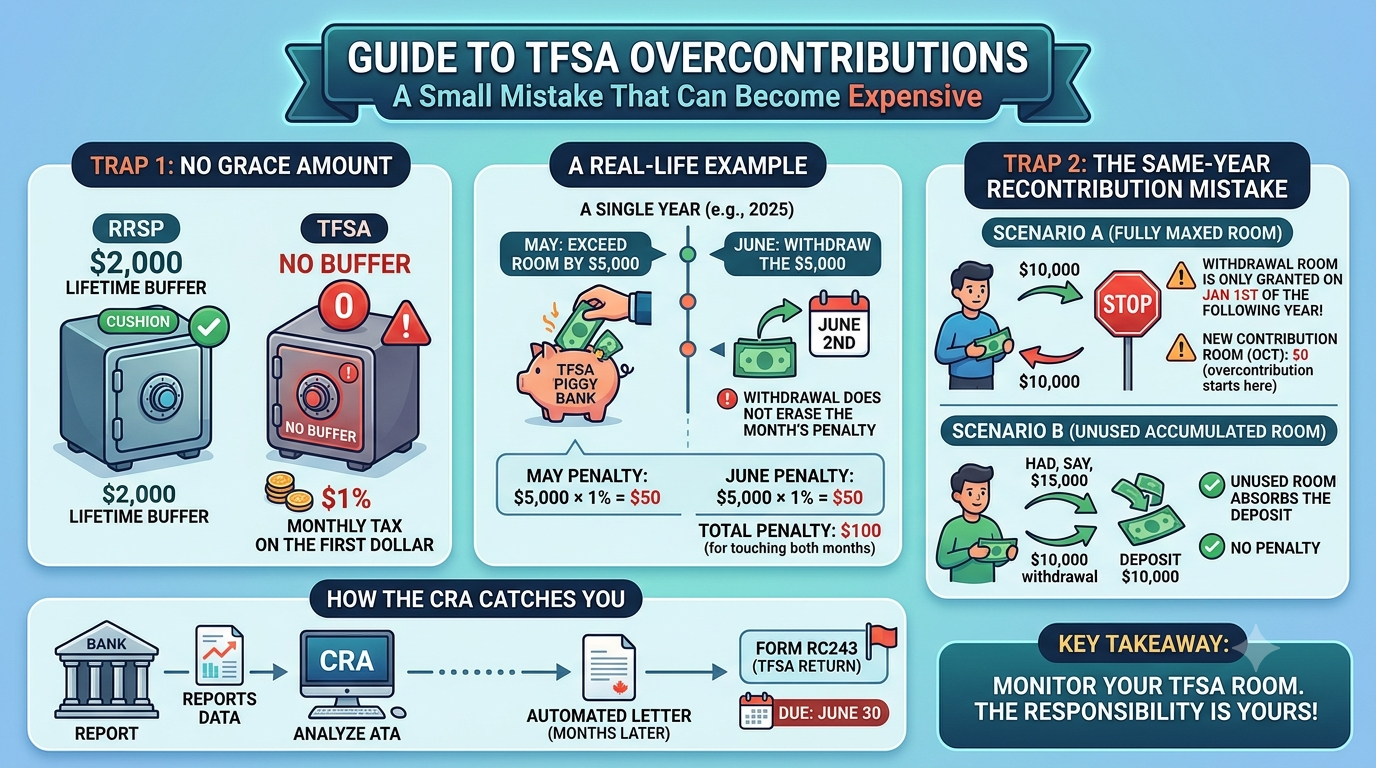

The Tax-Free Savings Account (TFSA) is one of Canada’s most popular investment accounts, but it also has one of the strictest penalty systems. If you contribute more than your available TFSA room, the CRA charges a penalty tax equal to 1% per month on the highest excess amount in that month, for every month the excess remains.

Trap 1: No Grace Amount

Unlike RRSPs — which offer a lifetime $2,000 overcontribution buffer — the TFSA has absolutely zero buffer. The CRA applies the 1% monthly penalty on the very first dollar of an overcontribution. Even a minor math error will trigger an immediate penalty.

A Real-Life Example

Suppose you miscalculate and exceed your TFSA contribution room by $5,000 in May.

- Monthly penalty: $5,000 x 1% = $50 per month

- Even if you realize your mistake and withdraw the excess on June 2nd, you will still owe the penalty for both May and June ($100 total) because the excess touched both calendar months.

- If the excess goes unnoticed for six months, the penalty increases to $300.

Note on the “One-Day” Trap: Just like the RRSP overcontribution rules, the TFSA penalty is not prorated on a daily basis. The CRA charges the full 1% on the highest excess amount reached during that calendar month. If you exceed your limit by $5,000 on May 31st and fix it on June 1st, you have officially touched two separate calendar months and will owe a full $100 penalty ($50 for May, $50 for June) — even though the mistake only lasted 48 hours.

Trap 2: The Same-Year Recontribution Mistake

By far, the most common TFSA mistake occurs when an investor withdraws money and then attempts to put it back later in the same calendar year.

The golden rule of TFSA withdrawals: Withdrawing funds does not instantly free up contribution room. While you do get 100% of your withdrawal room back, the CRA only grants that room back to you on January 1st of the following calendar year.

- Scenario A (The Trap): If you have fully maximized your lifetime TFSA room, withdraw $10,000 in July, and then put that same $10,000 back in October, you have officially overcontributed by $10,000 and will face a $100 per month penalty until December 31st.

- Scenario B (The Exception): If you still had $15,000 of unused, accumulated carry-forward room from previous years sitting in your account, your October deposit of $10,000 is perfectly safe. Because you had enough spare, unused historical room to absorb the new contribution, no penalty applies.

How the CRA Catches the Error

Financial institutions only report TFSA contribution data to the CRA once a year (by the end of February). The CRA then processes this information, meaning taxpayers typically receive an automated “Excess TFSA Amount” letter months down the road, long after penalties have quietly piled up.

If you find yourself in an overcontribution position, you must withdraw the excess immediately and file Form RC243 (Tax-Free Savings Account Return) along with your payment by June 30th of the following year.

Key Takeaway

Never rely blindly on the TFSA room listed on your CRA My Account portal mid-year, as it does not update in real-time when you make deposits or withdrawals. The ultimate responsibility for tracking your transactions month-to-month belongs entirely to you, not the CRA or your bank.

Disclaimer: This article is for educational purposes only and is not financial or tax advice. Please consult a qualified tax or financial professional before making any decisions.

What are your thoughts on this post? Share your comments with us.

Stay ahead of the curve. Subscribe here to get notified whenever I publish a new guide or tool.

Share your comment or feedback. We'll get back to you as soon as we can.