Adjusted Cost Base Explained in Plain English

Why Your Broker’s Numbers May Not Match the CRA — And Why It Matters

Many investors assume that the capital gain shown on their brokerage statement is the number they should report on their tax return. Unfortunately, that is not always true. In Canada, the responsibility for calculating capital gains correctly lies with the investor, not the broker. This is where Adjusted Cost Base (ACB) becomes important — and also where many investors make mistakes.

1. The Simple Definition: What is a Capital Gain?

In its simplest form, a capital gain is the difference between what you sell an investment for and what it cost you to buy it. If your sale price is higher than your purchase cost, you have a profit that the CRA wants to tax.

The Concept:

You bought something for $X and sold it for $Y. The difference is your gain (or loss).

The Equation:

Sale Proceeds − (Purchase Cost + Selling Costs) = Capital Gain or Loss

For example:

You bought 100 shares of TD Bank for $10,000 (including commission) and sold them for $11,000 (after deducting commission). In this case:

Capital gain = $11,000 − $10,000 = $1,000

If the sale proceeds are less than your purchase cost, the sale will result in a capital loss. For example, if it costs you $10,000 to buy the shares and you sell them for $9,500, the transaction results in a $500 capital loss ($9,500 − $10,000 = −$500).

This calculation looks simple, but in real life, the “purchase cost” is not always just what you originally paid. Over time, that number can change. That adjusted number is called the Adjusted Cost Base, or ACB.

2. What is Adjusted Cost Base (ACB)?

Adjusted Cost Base (ACB) is the total cost of an investment, including commissions and certain adjustments, spread across all the shares you own. In simple terms, ACB is the average cost per share of your investment after accounting for all purchases and adjustments over time.

A simple way to think about this is: capital gain is calculated when you sell; Adjusted Cost Base is built and adjusted over the entire period that you own the investment — sometimes over decades.

A Simple Example

Suppose you buy shares of Bank of Nova Scotia in multiple transactions:

- Buy 100 shares at $50 per share = $5,000

- Buy another 100 shares at $60 per share = $6,000

Your total cost is $11,000 for 200 shares.

So your ACB per share is:

ACB per share = Total Cost ÷ Total Shares

ACB per share = $11,000 ÷ 200 = $55 per share

Now, if you sell 50 shares, your capital gain is calculated using the ACB of $55 per share — not $50 or $60. This is because Canada requires investors to use the average cost method, rather than FIFO (First-In, First-Out), which is commonly used in countries like the United States.

Why ACB Changes Over Time

Many investors think ACB only changes when they buy more shares, but that is not true. Your ACB can change due to:

- Buying more shares

- New shares issued under the Dividend Reinvestment Plan (DRIP)

- Reinvested distributions (common with ETFs)

- Return of capital

- Superficial loss adjustments

- Foreign exchange for U.S. stocks

- Corporate actions (stock splits, mergers, spin-offs)

- Journaling shares between CAD and USD accounts

This is why the capital gain reported by your broker may not match the number you calculate for tax purposes.

The “Combined Account” Trap

In Canada, when you own the same stock or ETF in multiple purchases, you must average the cost of all shares to calculate your Adjusted Cost Base. More importantly, the Canada Revenue Agency views you as a single entity, regardless of how many brokerage accounts you use.

The Reality:

If you own 100 shares of the same stock at TD Direct Investing and another 100 at Wealthsimple, you have one combined pool of 200 shares with a single ACB.

The Danger:

Each broker tracks ACB only within its own account. Your TD Direct Investing statement does not know about your Wealthsimple purchases. If you rely on their separate “book values,” you may report the wrong capital gain when you sell shares at Wealthsimple.

This is one of the most common reasons why the amounts shown on the T5008 slip issued by your broker may not match the capital gain you should actually report on your tax return. The CRA expects you to calculate your capital gain using your own Adjusted Cost Base records, not simply copy the T5008 numbers.

Important:

The T5008 slip is sent to both you and the CRA, but the CRA expects you to report the correct capital gain using your own Adjusted Cost Base records — not simply copy the T5008 numbers.

Capital gain is calculated when you sell, but Adjusted Cost Base is built and adjusted over the entire period that you own the investment — sometimes over decades. That is why it is important to track the ACB for each investment you own over time, so that when you eventually sell, you report the correct capital gain or loss to the CRA.

Not All Investments are Created Equal

Before we look at the specific events that change your ACB, it is important to know what you are holding.

Note on Asset Types: While the rules of ACB apply to all investments, specific adjustments like Return of Capital (ROC) and Reinvested Distributions are primarily an ETF and mutual fund phenomenon.

If you only hold individual common stocks (like TD, Apple, or Microsoft), these year-end adjustments are rare. However, for ETF investors, tracking these adjustments is a non-negotiable part of good tax record-keeping. This is particularly important today, as more and more DIY investors are building their portfolios using ETFs.

3. Does This Apply to My RRSP or TFSA?

The good news is that you only need to track Adjusted Cost Base for your non-registered (taxable) accounts. You do not need to calculate ACB for:

- TFSA (Tax-Free Savings Account)

- RRSP (Registered Retirement Savings Plan)

- RRIF (Registered Retirement Income Fund)

- FHSA (First Home Savings Account)

- RESP (Registered Education Savings Plan)

In these accounts, you can buy and sell investments without worrying about capital gains or ACB. The tax-sheltered nature of these accounts means the CRA only cares about money going in or coming out — not the individual trades happening inside these accounts.

4. Why Your Broker’s Numbers May Not Match the CRA

By now, you might be wondering: if calculating capital gains depends on ACB, why doesn’t my broker get it right?

Main reasons:

- Brokers track accounts separately

- They may not adjust for reinvested distributions for ETFs

- Foreign exchange may be handled incorrectly

- Superficial loss rules are not fully tracked

- Return of capital adjustments may be missing

- Transferring accounts between brokers may break ACB tracking

- Corporate actions and ETF mergers may not be fully reflected in book value

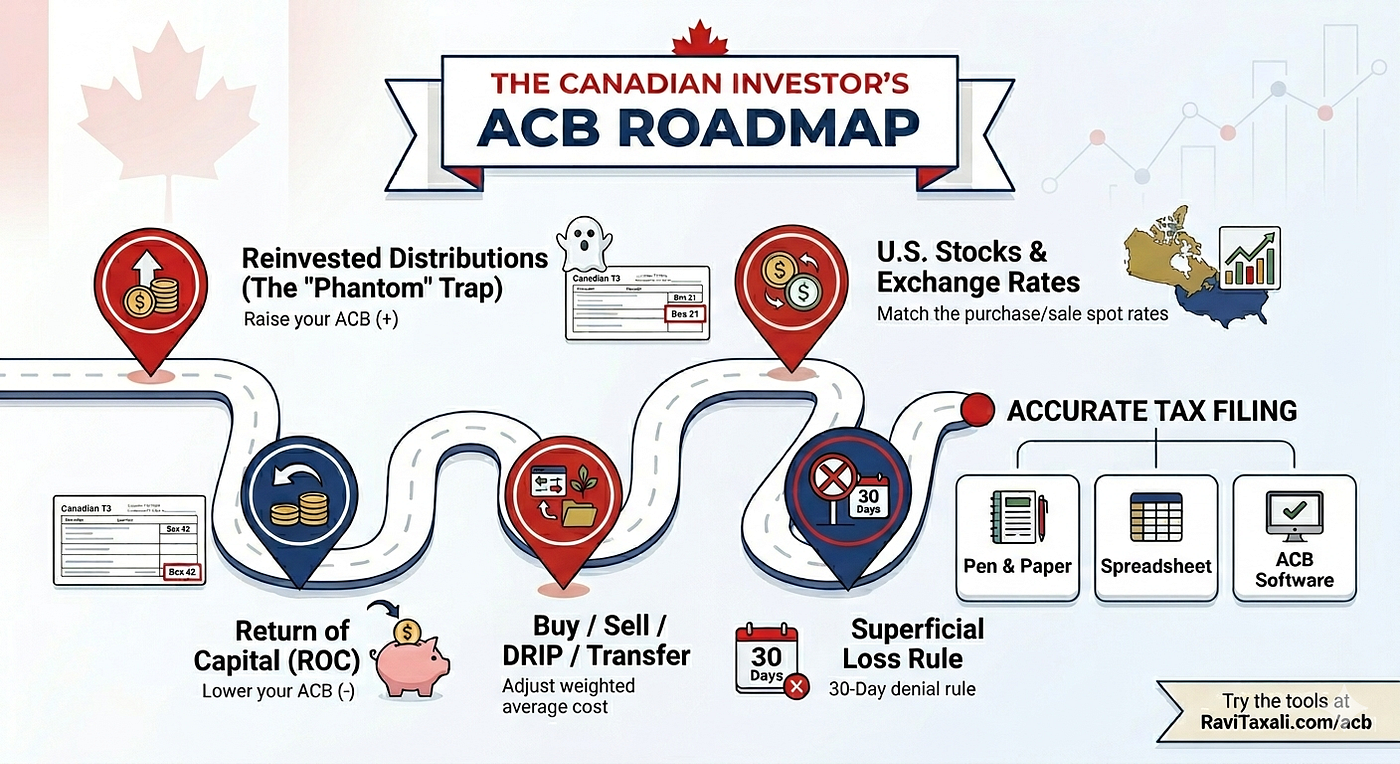

5. Reinvested Distributions: The ETF “Phantom” Trap

If you hold ETFs like XAW, XEQT, XEG or VEE in a non-registered account, you are likely receiving what are known as “Phantom Distributions.” This is perhaps the single most common way DIY investors accidentally pay tax twice on the same dollar.

What is a Phantom Distribution?

Normally, when an ETF makes a profit (by selling an underlying stock for a gain), it can pay that profit out to you as cash. However, to keep the fund’s “tracking” efficient, the manager often chooses to reinvest that profit back into the fund on your behalf.

Instead of sending you a cheque, they reinvest the gain and then perform a “notional” share consolidation so that your total number of shares stays the same. To the naked eye, nothing happened in your account — hence the name “Phantom.”

The Tax Hit (The T3 Slip)

Even though you didn’t receive a penny in cash, the CRA considers this reinvested amount to be taxable income in the year it occurred.

- You will see this amount reported on your T3 slip, typically in Box 21 (Capital Gains).

- You are required to pay tax on this “phantom” money on your current year’s tax return.

Note: The phantom distribution amount is usually reported as a “Reinvested Capital Gain Distribution” in the ETF provider’s annual tax breakdown, not directly on your brokerage statement. This is why many investors miss this adjustment completely.

The ACB Fix (The “Double Tax” Shield)

Because you have already paid tax on this reinvested money, it effectively becomes part of your “purchase cost.” To avoid being taxed on it again when you eventually sell the ETF, you must increase your ACB by the amount of the reinvested distribution.

⚠️ The “Box 21” Trap

A word of caution: Do not blindly use the total in Box 21 of your T3 slip to adjust your ACB. Box 21 reports the total capital gains for the year, which often includes both the cash distributions you already received and the phantom reinvestments. If you add the whole box to your ACB, you will over-inflate your cost base and under-report your future taxes — a mistake the CRA will eventually catch.

The Solution: To get the correct number, you must look at the “Annual Tax Factors” published by the ETF provider (BlackRock (iShares), Vanguard, BMO, etc.) or use a specialized ACB tracking tool that pulls this specific “Non-Cash Distribution” data for you.

By manually increasing your ACB for these phantoms, you are creating a “Tax Shield” that ensures you only pay the CRA exactly what you owe — and not a penny more.

Based on the 2024 Distribution Characteristics from BlackRock Canada, here is a specific example of phantom distributions. This example illustrates exactly how a “reinvested distribution” appears in the data alongside regular cash payments.

The XEG Case Study (2024 Tax Year)

If you held 1,000 units of the iShares S&P/TSX Capped Energy ETF (XEG) throughout 2024, your year-end breakdown would look like this:

Where the numbers appear:

- In Your Brokerage Account: You received $592.40 in actual cash. This is the only part of the distribution you likely noticed.

- On Your T3 Tax Slip: Your broker will issue a T3 slip showing a total Capital Gain in Box 21 of $1,472.12.

- The Trap: You are paying tax on the full $1,472, even though you only put $592 in your pocket. The other $879.72 was reinvested “behind the scenes” by the fund.

In Your ACB Tracker: This is where you must act to prevent “Double Taxation.” Because you already paid tax on that $879.72 phantom amount today, it must be added to your purchase cost.

- Action: You must increase your ACB by $879.72.

Why this matters: The “Double Tax” Penalty

If you don’t manually perform this +$879.72 adjustment, your records will show that your investment cost you less than it actually did (after taxes).

When you eventually sell your XEG units, your capital gain will be artificially inflated by that same $879.72. Effectively, you will pay tax on that money twice — once on your 2024 T3 slip, and a second time in the year you sell.

Investor Tip: Over 20 years of holding a portfolio, ignoring these phantom reinvestments is like leaving a tip for the CRA every time you sell. For a large account, this oversight can easily cost you thousands of dollars in unnecessary taxes.

6. Return of Capital (ROC): Getting Your Own Money Back

While a “phantom” distribution is a gain you didn’t receive in cash, Return of Capital (ROC) is almost the exact opposite. It is cash that you did receive, but it isn’t considered “income” by the CRA.

What is Return of Capital?

Sometimes, a fund (especially REITs or monthly income ETFs) pays out more cash to investors than it actually earned in profit. When this happens, the fund is effectively giving you back a portion of your own original investment.

Because you are simply receiving your own money back, the CRA does not tax this amount as income in the year you receive it. Instead, they require you to lower the “cost” of your investment.

Where to Find the Number (Box 42)

The good news is that you don’t have to go hunting for this data. Your brokerage will report the total ROC for the year directly on your T3 slip in Box 42 (officially labelled as “Amount of adjustment of the cost base”).

The ACB Fix: The “Subtraction” Rule

Since ROC is a refund of your original capital, it reduces your “skin in the game.” To keep your tax records accurate, you must decrease your ACB by the amount shown in Box 42.

Why this matters: By lowering your ACB now, you are deferring your tax. You aren’t paying tax today, but because your “cost” is now lower, you will have a larger capital gain (and a larger tax bill) when you eventually sell the investment.

⚠️ Important: ROC can continue for many years and can eventually reduce your ACB to zero. Once your ACB reaches zero, any further ROC you receive must be reported as an immediate capital gain in that year.

Real-World Example: VRIF (2025 Tax Year)

The Vanguard Retirement Income ETF Portfolio (VRIF) is specifically designed to provide a consistent monthly cash flow. Often, a part of that cash is returned capital.

- As per the 2025 Distribution History document, ROC per Unit: $0.20280

The Math for 1,000 Units of VRIF:

If you held 1,000 units of VRIF throughout 2025, you received approximately $1,000 in total cash, but your T3 slip would show $202.80 in Box 42.

- Your Action: You must subtract $202.80 from your total Adjusted Cost Base.

- The Result: You don’t pay tax on that $202.80 today, but your “cost” in the fund is now lower. You will eventually pay the tax as a capital gain when you sell the units in the future.

Summary: The Plus and Minus of ETF Adjustments

- Phantom distributions → Increase ACB

- Return of Capital → Decrease ACB

7. U.S. Stocks and Exchange Rates: The Currency Mismatch

If you trade stocks listed on U.S. exchanges (like Apple, Microsoft, or U.S.-listed ETFs), your ACB tracking has an extra layer of complexity. You aren’t just tracking the stock price; you are tracking the Value of the Canadian Dollar at two different points in time.

The Golden Rule: Use the “Spot Rate”

The CRA requires you to convert every transaction into Canadian dollars (CAD) using the exchange rate in effect on the settlement date of the trade.

- The Purchase: Convert the USD cost to CAD using the exchange rate on the day you bought the shares.

- The Sale: Convert the USD proceeds to CAD using the exchange rate on the day you sold the shares.

The Mismatch Trap

Many investors make the mistake of calculating their gain in USD and then converting that final profit into CAD at the end of the year. This is incorrect. Because the exchange rate fluctuates, you can actually have a “Capital Gain” in Canada even if the stock price didn’t change in the U.S.

Example:

- Buy: You buy 100 shares of a U.S. stock at $100 USD when $1 USD = $1.30 CAD. Your CAD Cost (ACB): $13,000

- Sell: One year later, the stock is still $100 USD, but the dollar has shifted, so $1 USD = $1.40 CAD. Your CAD Proceeds: $14,000

- The Result: Even though the stock price stayed flat at $100, you have a $1,000 Capital Gain due solely to the currency change.

Investor Tip: Avoid “Average Annual Rates”

While the CRA allows an “average annual exchange rate” for some types of foreign income (like dividends), they strictly require the daily spot rate for capital gains. Your brokerage's “Book Value” may use a simplified or outdated rate, so manual tracking is the only way to ensure 100% accuracy.

8. Transfers to Registered Accounts: The “Sale That Isn’t a Sale”

Many investors move shares directly from a non-registered account into an RRSP or TFSA — often for convenience or to avoid selling first. While this looks like a simple “move,” the CRA views it as a Deemed Disposition.

The “Deemed Disposition” Rule

The moment your shares leave a non-registered account for a registered one, the CRA treats it as if you sold them at Fair Market Value (FMV).

- If there is a Gain: You must report the capital gain on your tax return in the year of the transfer, even though you did not receive any cash. You are paying tax on a “profit” even though no cash entered your pocket.

- Impact on ACB: Your weighted average ACB is used to calculate this gain. While the ACB per share for any remaining stock in your non-registered account stays the same, you must record this transfer as a “transfer-out or sale” in your tracker to keep your total share count and book value accurate.

⚠️ The Superficial Loss Trap

When moving shares “In-Kind,” there is a dangerous one-way street:

- Gains are taxed: If your shares are up, the CRA wants their cut.

- Losses are DENIED: If your shares are currently worth less than your ACB, the Superficial Loss Rule kicks in. Because you (the “affiliated person”) still own the stock inside your TFSA or RRSP immediately after the “transfer-out,” the capital loss is rejected.

The “Kicker”: In a regular account, a denied loss is typically added back to your ACB to be used later. But because a TFSA/RRSP has no ACB, that tax loss vanishes forever.

The “30-Day” Strategy for Losing Positions

If your stock is in the red, never hit the “Transfer” button. Instead, use one of these two “Pro Moves” to protect your tax loss:

Option A: The 31-Day Wait

- Sell the shares in your non-registered account to trigger the capital loss.

- Transfer the cash to your TFSA/RRSP.

- Wait at least 31 days before buying the same stock back.

Risk: The stock price might spike while you are waiting on the sidelines.

Option B: The “Similar but Not Identical” Switch

- Sell “Bank A” at a loss in your non-registered account.

- Move the cash to your TFSA/RRSP immediately.

- Buy “Bank B” or a sector ETF (like a Banking ETF) right away.

Benefit: You keep your “market skin in the game,” and your tax loss is safe because Bank B is not “identical” to Bank A.

Summary for the Roadmap: If your investment is at a profit, an in-kind transfer is a convenient way to contribute, provided you are ready for the tax bill. If it’s at a loss, sell for cash first. Don’t give the CRA a “gift” by throwing away a perfectly good tax loss.

9. Common ACB Mistakes DIY Investors Make

Over the years, I have seen the same Adjusted Cost Base mistakes repeated again and again. Most of them come from relying too much on brokerage statements and T5008 slips, and not understanding how ACB is adjusted over time.

The most common mistakes include:

- Using the broker’s book value instead of tracking your own ACB

- Forgetting to adjust ACB for reinvested (phantom) ETF distributions

- Ignoring Return of Capital (ROC), which reduces ACB over time

- Not combining holdings across multiple brokerage accounts

- Using average exchange rates instead of the actual rate on each transaction for U.S. stocks

- Losing track of ACB after transferring shares between accounts

- Not adjusting ACB after stock splits, mergers, or spin-offs

- Losing historical records after switching brokers

Individually, these mistakes may seem small, but over many years, they can significantly overstate or understate your capital gains. Keeping a simple ACB tracking spreadsheet or using dedicated software can help avoid these problems.

10. How to Track Your ACB: From Pen and Paper to Professional Tools

Now that you understand the “Why,” the question is “How?” Tracking ACB is not a one-time task; it is a lifetime habit. Depending on your comfort level with data, there are three main ways to keep your records straight.

Manual Record Keeping (The Old School Way)

Some investors prefer a physical ledger or a dedicated notebook.

- The Pro: You have a physical “paper trail” that doesn’t depend on a hard drive or a cloud subscription.

- The Con: It is highly prone to human error. Calculating a Weighted Average Cost manually every time you buy, sell, or receive a Phantom Distribution is tedious and risky. One math error in year two can affect your tax filings in year ten.

Spreadsheets (The DIY Developer Way)

Many tech-savvy investors build their own Excel or Google Sheets trackers.

- The Pro: Highly customizable. You can build formulas to automate the weighted average and track multiple accounts in one file.

- The Con: You are responsible for the data entry. You must manually hunt down the “Tax Factors” for every ETF you own and remember to check for Return of Capital (Box 42) every March. If you forget one row, your entire “Book Value” is compromised.

Specialized ACB Tracking Software

This is the modern standard for DIY investors. These tools are designed to handle the specific “edge cases” of Canadian tax law — like the 30-day superficial loss rule and currency conversions — automatically.

- The Advantage: These platforms often have databases that “know” the reinvested distributions for major ETFs (like the XEG or VRIF examples we discussed), saving you hours of manual research.

- My Recommendation: I am a firm believer that software should make our lives easier, not harder. Over the years, I found that specialized ACB tracking tools can save a significant amount of time and help avoid costly mistakes, especially for ETF investors and those trading in multiple accounts.

Take the Guesswork Out of Your Taxes

If you are tired of fighting with spreadsheets or worrying if your “Book Value” is accurate, I invite you to try a set of free ACB tracking tools I’ve developed. They are designed to be intuitive, accurate, and built for the specific needs of Canadian investors.

👉 Try the tools at: RaviTaxali.com/acb

The CRA does not ask you to submit your ACB calculations with your tax return, but you are required to keep supporting records in case they ask for them later. This is why maintaining proper ACB records is not optional — it is part of your tax documentation.

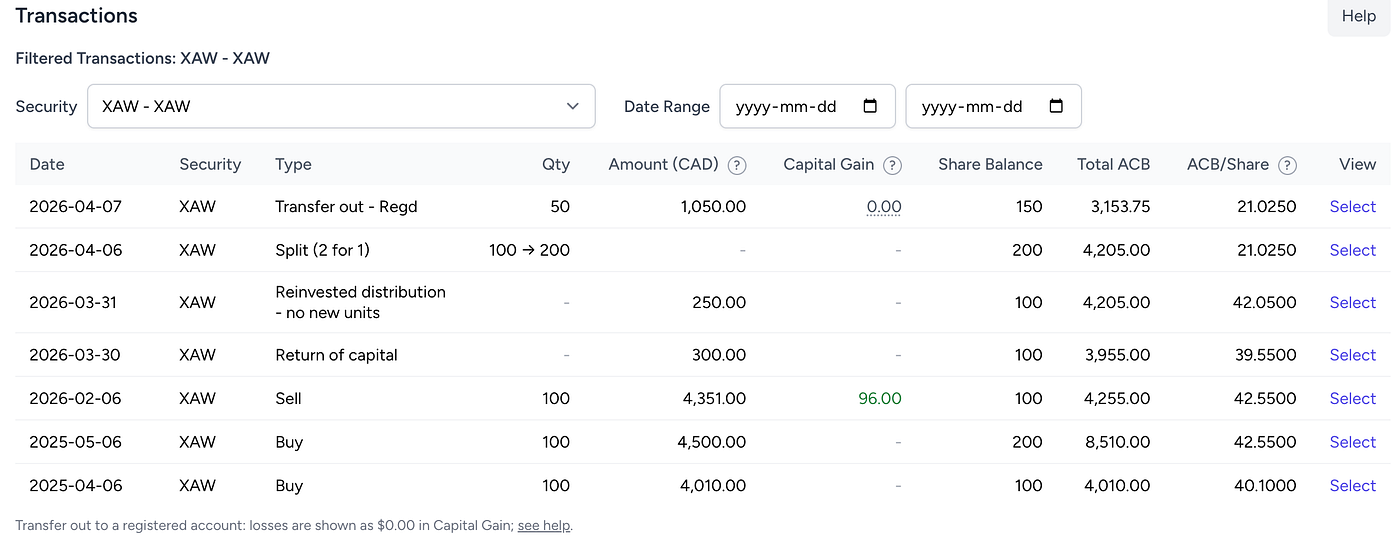

11. The Anatomy of an ACB Ledger: Putting It All Together

To help visualize how these rules interact, let’s look at a sample ledger for a security (XAW) that undergoes several common “tax events” over two years.

By following the ledger from bottom to top, you can see exactly how the Total ACB and ACB/Share fluctuate:

- April 2025 — May 2025 (The Buys): Notice how the ACB/Share is recalculated as a weighted average when the second 100 shares are bought at a higher price ($42.55 vs. $40.10).

- Feb 2026 (The Sell): Selling 100 shares reduces the Total ACB by exactly half, but the ACB/Share remains unchanged at $42.55.

- Mar 30, 2026 (Return of Capital): A $300 ROC payment is received. No shares are sold, but the Total ACB drops from $4,255 to $3,955.

- Mar 31, 2026 (Reinvested Distribution): A $250 “Phantom” distribution occurs. The Total ACB increases back up to $4,205. Note that the share balance stays at 100.

- Apr 06, 2026 (Stock Split): A 2-for-1 split doubles the share count to 200. The Total ACB ($4,205) stays the same, but the ACB/Share is cut in half to $21.025.

- Apr 07, 2026 (Transfer Out — Regd): 50 shares are moved to a TFSA. Even though the “Capital Gain” column shows $0.00 (indicating a loss that was denied by the Superficial Loss Rule), the ledger correctly records the “sale” to keep the remaining 150 shares accurate.

The “Aha!” Moment

Looking at this ledger, ask yourself: Would my brokerage statement have tracked all of those nuances correctly? In many cases, the answer is no — especially for the ROC and Reinvested Distributions that happen “behind the scenes.” This is why having a dedicated ledger is your best defence against overpaying your taxes.

12. Closing Thought: Your “Final Audit”

Whether you use a notebook or ACB software, the most important thing is that you start today. Don’t wait until the year you decide to retire and sell your portfolio to realize your records are a mess.

Treat your ACB tracking as your “Final Audit” protection.

When the CRA eventually asks how you calculated your capital gains, you won’t have to scramble — you’ll simply open your records and show your calculations.

Your broker reports transactions.

The CRA taxes capital gains.

But only you are responsible for tracking the Adjusted Cost Base correctly.

Disclaimer: This article is for educational purposes only and is not financial or tax advice. Please consult a qualified tax or financial professional before making any decisions.

What are your thoughts on this post? Share your comments with us.

Stay ahead of the curve. Subscribe here to get notified whenever I publish a new guide or tool.

Share your comment or feedback. We'll get back to you as soon as we can.