Why Your “Safe” Canadian Dividends Could Be a Retirement Trap

The Canadian Investor’s Guide to Dividends, Yield Traps, and OAS Clawbacks.

In the Canadian investment landscape, dividends are more than just a source of income; they are a cultural staple. With a domestic market dominated by “Blue Chip” giants in banking, telecommunications, and energy, which have been providing stable or even growing dividends, many Canadian investors build their entire financial future around these quarterly dividend payouts. They believe that good dividend-paying companies will provide them with a very good chance of growth during their working life and a predictable income during retirement.

However, like any investment strategy, Canadian dividends are a double-edged sword. While they offer unique tax advantages during your working years, they can lead to portfolio stagnation and unexpected “clawbacks” in retirement. To build a truly resilient portfolio, you need to understand both sides of the coin.

The Fundamentals: What is a Dividend?

Before diving into the pros and cons, it is important to understand what a dividend actually represents. Simply put, a dividend is a portion of a company’s earnings that its Board of Directors decides to “give back” to its shareholders. It is your reward for owning a piece of the business.

Why do some companies pay dividends?

Mature, established companies — like Canada’s Big Five banks, telecom and utilities— often generate more cash than they need to run their daily operations. Since they have already achieved a dominant market position, they distribute this “excess” cash to shareholders as a way to signal financial health and provide a steady return on investment.

Why do some companies NOT pay dividends?

You will notice that many high-growth companies (especially in Tech) pay low or even zero dividends. This isn’t because they are “stingy”; it’s because they have better options for that cash.

- They choose to reinvest every dollar back into the business — funding research, building new infrastructure, or acquiring competitors.

- The goal is to grow the business faster, thereby increasing future earnings and driving the stock price higher. In this case, your “return” comes from the stock price going up (Capital Gains) rather than a dividend payment on a quarterly, bi-annual or annual basis.

Case Study: The Alphabet (Google) Example

To see this in action, look at Google (Alphabet). For nearly 20 years after its 2004 IPO (Initial Public Offering), Google did not pay a single cent in dividends. Instead, it reinvested billions into search, YouTube, Gmail, Maps, Cloud, and much more. It was only in June 2024 that it initiated a modest quarterly dividend of $0.20. Even as of January 2026, the dividend remains a relatively small $0.21 per quarter. However, the lack of a dividend didn’t hurt investors. From 2004 through 2025, the stock’s Compound Annual Growth Rate (CAGR) from price moves alone was approximately 22% per year.

The Bottom Line on Selection

As the Google example illustrates, whether a company pays a dividend is not a primary factor in determining its worthiness — a dividend is simply a capital allocation choice for the company. Your focus should always be on “Total Return” — the combination of dividends and price appreciation — rather than just the dividend yield itself.

Why Canadians Love Dividend-Paying Companies

In many global markets, investors prioritize “Moonshots” and high-growth tech stocks. But in Canada, the dividend-payer is king. This isn’t just a tradition; it’s driven by a unique combination of market history, availability, and investor psychology.

1. The Psychology of Predictable Cash Flow

As noted in our opening, the stability of the “Big Five” banks and major utilities provides a psychological safety net. Receiving a physical deposit provides a tangible return on investment that helps investors stay the course during market volatility. Unlike growth stocks, which rely entirely on fluctuating market prices to show “profit,” a dividend is cash-in-hand. This “bird in the hand” approach makes it much easier to weather a “sideways” market without panic-selling.

2. The Power of Reinvesting (The “Snowball Effect”)

For many Canadians, the goal isn’t just to spend the dividend, but to use it to acquire more of the company. Through Dividend Reinvestment Plans (DRIPs), investors can automatically use their payouts to purchase more shares — often without paying any commission fees.

- Compounding in Action: This enables you to acquire more shares every quarter, which in turn increases the amount of your next dividend.

- Accelerated Growth: Over decades, this creates a “snowball effect” where your share count grows exponentially, significantly increasing your future income stream even if you never contribute another dollar of your own “new” money.

3. A Yield-Heavy Domestic Market

Historically, Canadian companies have paid out significantly more in dividends than large companies in the U.S. or globally. While the U.S. market (S&P 500) currently yields around 1.3% to 1.5%, the Canadian market (TSX 60) often yields closer to 3% to 4%. Because our economy is defined by “Big” players in mature, stable industries with limited competition (oligopolies), they have plenty of excess cash to return to shareholders.

4. The “Era Before ETFs” (and the 30% Rule)

It is also worth remembering that the ease of global investing is a relatively new phenomenon. Before Exchange-Traded Funds (ETFs) became popular and low-cost, Canadian investors did not have easy or affordable avenues to invest in U.S. or global companies.

- The Foreign Property Rule (FPR): For most of the late 20th century, the Canadian government actually restricted how much foreign content you could hold in a registered account (like an RRSP). Before 1990, the limit was a mere 10%. It was gradually raised to 20%, and then to 30% in 2001, before being completely abolished in 2005.

- Forced Domesticity: This meant that for decades, if you wanted the tax advantages of an RRSP, you were legally compelled to keep 70% to 90% of your money in Canada. Since our market is so heavy on banks, energy, and utilities, Canadians were “forced” into a dividend-heavy strategy by law.

- Cultural Legacy: This created a multi-generational “dividend culture.” Many Canadians grew up watching their parents live off bank dividends because that was essentially the only choice they had. This cemented the idea that domestic dividends are the “correct” or “safest” way to build wealth, even though the legal barriers to global growth have been gone for over 20 years.

The Disadvantages: The Risks of “Chasing” Dividends

While the steady stream of income feels secure, focusing exclusively on dividend-paying companies — especially within the borders of Canada — comes with significant structural risks.

1. Concentration and “Country” Risk

The Canadian market is famously narrow. If you strictly filter for high-dividend companies, you will likely end up with a portfolio heavily concentrated in just three sectors: Financials, Energy, and Utilities.

- The Sector Trap: These three sectors make up roughly two-thirds of the S&P/TSX Composite. If Canadian interest rates rise or the domestic housing market cools, your entire portfolio could suffer simultaneously because your “diversification” was only an illusion.

- The Tech Gap: By chasing dividends, you effectively exclude the Information Technology and Healthcare sectors. These sectors represent the engine of global growth but rarely pay high dividends because they are reinvesting in innovation. As of 2026, the S&P 500 has over 30% exposure to high-growth tech, while the Canadian market remains under 10%.

2. Missing Out on the Growth Giants

By prioritizing “yield” over “total return,” investors often miss out on the most successful wealth-creators of the modern era. Companies like Amazon, Berkshire Hathaway, and (until recently) Google built massive shareholder value without paying a dividend. An investor who insisted on a 3%-4% yield would have sat on the sidelines while these “non-payers” delivered total returns that far outpaced the Canadian banks.

Remember: A company that pays a 5% dividend but has a flat stock price is underperforming a company that pays 0% but grows its share price by 10%.

3. Interest Rate Sensitivity

Dividend stocks are often viewed as “bond proxies.” When interest rates are low, investors flock to stocks like Telus or Fortis for yield. However, when interest rates rise (as seen in the mid-2020s), these stocks often drop in value.

- Competition for Capital: If a “risk-free” GIC starts paying 4% or 5%, investors often sell their “risky” 4% dividend stocks to move into the safety of fixed income.

- Debt Costs: Many high-dividend payers (like Utilities and REITs) carry high debt loads to fund their infrastructure. Rising rates increase their interest expenses, which can eat into the very profits used to pay your dividends.

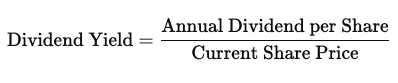

4. The “Yield Trap”: A Case Study of BCE (2008–2025)

Perhaps the most dangerous disadvantage is the Yield Trap. Here is the formula to calculate yield:

Therefore, a yield often looks attractive simply because the company’s stock price is crashing.

5. The BCE Story: How a Once-Safe Dividend Stock Lost 50%

For decades, BCE was viewed as the ultimate “safety-net” stock. Between 2008 and 2022, its share price nearly tripled — from about $23 to over $73 — while paying a reliable and steadily growing dividend that typically yielded between 5% and 8%. It became a cornerstone of millions of Canadian retirement portfolios.

However, the trap began to form as interest rates started rising in 2022.

The Squeeze: As a capital-intensive utility, BCE was especially vulnerable to higher borrowing costs. At the same time, the company was spending billions on network upgrades and U.S. acquisitions, including Ziply Fiber, placing increasing pressure on free cash flow.

The Mirage: By early 2025, BCE’s share price had fallen into the $40s. Because the dividend had not yet been cut, the headline yield appeared enormous — approaching 10%. Many investors chased this yield, assuming the payout remained safe.

The Reality Check: In May 2025, the unthinkable happened. BCE cut its dividend for the first time in 17 years, slashing it by 56%, from roughly $3.99 to $1.75 annually.

The Result: By January 2026, BCE’s share price had fallen to approximately $24, erasing nearly all of the price gains accumulated since 2008. Investors who bought for the “safe 9% yield” in early 2025 suffered losses of more than 40% of their capital — and over half of their income.

The Result: By January 2026, the stock price has plummeted to approximately $24 — wiping out nearly all the price gains made since 2008. Investors who bought for the “safe 9% yield” in early 2025 have now lost over 40% of their principal and more than half of their income.

The Lesson: A high yield is often the market’s way of signalling that a dividend cut may be coming. When a yield looks too good to be true relative to its peers, it usually is.

The Retirement Mirage: Why the “Gross-Up” Matters (And Why It Might Not)

As you approach retirement, the way the government calculates your income changes. While Canadian dividends are famous for their tax efficiency, they can occasionally trigger a “hidden cost” in the form of benefit clawbacks.

The Good News: It Depends on Your Account

Before we look at the mechanics, it is important to remember that for many investors, this is a non-issue:

- In a TFSA: Dividends are truly tax-free. They do not report to the CRA as income and have zero impact on your government benefits.

- In an RRSP / RRIF: Dividends grow tax-deferred. When you withdraw money, it is treated as regular income. There is no “dividend gross-up” here, so while it affects your income, it doesn’t have the “artificial inflation” effect we’re about to discuss.

- The “Danger Zone”: This quirk only affects dividends earned in Non-Registered (Taxable) accounts.

1. The Mechanic: What is the “Gross-Up”?

When you receive an eligible Canadian dividend in a taxable account, the CRA uses a “Gross-Up” system to account for the corporate taxes the company already paid.

- The Reality: You receive $1,000 in cash.

- The Tax Return: You must report $1,380 as income (a 38% “Gross-Up”).

You receive a tax credit to lower your actual tax bill, but that $1,380 figure is what the government uses to decide if you qualify for certain income-tested benefits.

Note on Foreign Dividends: The dividend gross-up does not happen for dividends earned from non-Canadian companies. If you receive a dividend from a U.S. company (like Apple or Coca-Cola), it is reported at its actual 100% value (e.g., $1,000 received = $1,000 reported).

The Trade-Off: While U.S. dividends don’t “inflate” your income for clawbacks, they are taxed at your full marginal rate (like a salary or interest income) and do not qualify for the Canadian Dividend Tax Credit.

2. The GIS Clawback (For Low-to-Middle Income)

The Guaranteed Income Supplement (GIS) is a lifeline for many seniors. However, it is an “income-tested” benefit, meaning it is clawed back by 50 cents for every $1 of other reported income.

Because of the gross-up, your $1,000 dividend looks like $1,380 to the CRA.

- The Reduction: The government may reduce your GIS by $690 ($1,380 x 50%).

- The Result: Even if you pay zero tax on that dividend, you have effectively “lost” 69% of your payout through benefit reductions.

💡 Strategic Tip for GIS Recipients: If you expect to rely on the GIS during retirement, you should avoid holding dividend-paying stocks in a non-registered account. If you already own them, consider selling them before you turn 65 to “lock in” your gains and clean up your reported income. Generally, low to middle-income Canadians should prioritize their TFSA for all dividend-paying investments to ensure every dollar of income remains invisible to the GIS clawback rules.

3. The OAS “Recovery Tax” (For Middle-to-High Income)

Canadian dividends received in a non-registered account for middle-to-high income Canadians can cause significant problems related to the OAS Clawback (officially called the Recovery Tax) due to the dividend gross-up.

For the 2026 tax year, the Old Age Security (OAS) clawback begins at an income threshold of $95,323. If your net income is close to this limit, the 38% gross-up on Canadian dividends can unexpectedly push you over the edge.

The Math of the Clawback

The government takes back 15 cents for every dollar your reported income exceeds that threshold. Because the CRA calculates your income based on the grossed-up amount — not the actual cash you received — the penalty is steeper than it appears.

- The Scenario: You are right at the $95,323 threshold with your RRSP/RRIF withdrawal, OAS pension and CPP. You receive $10,000 in actual cash dividends from Canadian stocks in your taxable account.

- The CRA’s View: Due to the gross-up, the CRA records your income as $13,800.

- The Penalty: You are now $13,800 over the limit.

- The Clawback: You must pay back $2,070 of your OAS ($13,800 x 15%).

The “Hidden Tax” Reality: In this example, that $10,000 dividend didn’t just come with standard income tax; it effectively cost you an extra 20.7% in lost OAS benefits. When you combine the actual tax paid with the benefit loss, your “effective” tax rate on those dividends can be shockingly high — sometimes higher than if you had simply earned the money as a regular income.

4. What Can You Do to Avoid the OAS Clawback Trap?

Five to ten years before you plan to retire, have a look at your estimated income from CPP, OAS, RRSP/RRIF and other sources. If your estimated income is close to the OAS clawback threshold, you may take the following corrective actions:

- Stop the DRIP: If you have been using a Dividend Reinvestment Plan (DRIP), turn it off. By receiving the cash instead of automatically buying more shares, you prevent your future dividend payouts from growing even larger and pushing you further into the clawback zone.

- Shift Toward Growth: Gradually sell your high-dividend paying shares or ETFs and replace them with investments that pay zero or low dividends (relying instead on capital gains).

Important: Do this slowly over several years. Selling all at once can trigger a massive capital gain that may result in a big tax bill in a single year. - Delay Your OAS: You can choose to delay the start of your OAS payments up until age 70. This not only increases your future monthly payment (by 0.6% per month or 36% total), but it also gives you a longer window to “clean up” your non-registered account and convert high-dividend shares into low-dividend growth shares before the clawback rules even apply to you.

Conclusion: The Total Return Mindset

Canadian dividends are a powerful tool, but they are not a “set it and forget it” strategy. As we have seen, the very things that make them attractive during your working years — predictable cash and tax efficiency — can become liabilities in retirement if not managed carefully.

The Power of “Homemade Dividends”

Instead of waiting for a company to send you a dividend, you can create your own “dividends” by selling a portion of your holdings. This gives you total control: you only sell when you need the money, and you leave the rest to grow tax-deferred.

The Tax-Free Advantage of Selling

When you sell shares or an ETF, a large portion of the cash you receive is simply the return of your original investment, which is completely tax-free. You only pay tax on the growth (the capital gain), and even then, you only report 50% of that gain as income.

Example: Imagine you bought shares for $6,000 and they grew to $10,000.

- If you sell: You receive $10,000 in cash.

- The Taxable Part: Your gain is $4,000. Under the 50% inclusion rule, you only report $2,000 to the CRA.

- The Result: You have $10,000 in your pocket, but the government only sees $2,000 of income. Contrast this with receiving $10,000 in Canadian dividends, where the government would see $13,800 of income on paper!

The Verdict

To build a truly resilient financial future, move beyond the “yield at all costs” mentality. A modern Canadian portfolio should be built on Total Return: a healthy mix of dividend-paying stability and high-growth innovation. By understanding the “Double-Edged Sword” of the dividend gross-up and embracing capital gains, you can ensure your retirement income stays in your pocket — not lost to benefit clawbacks.

Note: This article is part of the Canadian Investment & Retirement Roadmap series. Follow the publication and explore related articles on TFSA, FHSA, RRSP, income splitting, and tax-efficient investment strategies.

Disclaimer: This article is for educational purposes only and is not financial or tax advice. Please consult a qualified tax or financial professional before making any decisions.

What are your thoughts on this post? Share your comments with us.

Stay ahead of the curve. Subscribe here to get notified whenever I publish a new guide or tool.

Share your comment or feedback. We'll get back to you as soon as we can.